Advertisement

TASK Group Holdings Limited's (ASX:TSK) 100% Price Boost Is Out Of Tune With Revenues

TASK Group Holdings Limited (ASX:TSK) shareholders have had their patience rewarded with a 100% share price jump in the last month. The annual gain comes to 120% following the latest surge, making investors sit up and take notice.

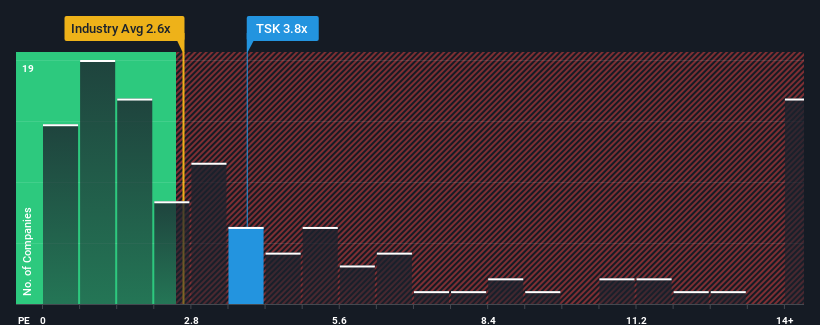

After such a large jump in price, you could be forgiven for thinking TASK Group Holdings is a stock not worth researching with a price-to-sales ratios (or "P/S") of 3.8x, considering almost half the companies in Australia's Software industry have P/S ratios below 2.6x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for TASK Group Holdings

What Does TASK Group Holdings' P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, TASK Group Holdings has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on TASK Group Holdings.Is There Enough Revenue Growth Forecasted For TASK Group Holdings?

TASK Group Holdings' P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 64% last year. Pleasingly, revenue has also lifted 169% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 8.9% as estimated by the dual analysts watching the company. That's shaping up to be materially lower than the 22% growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that TASK Group Holdings' P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

What Does TASK Group Holdings' P/S Mean For Investors?

The large bounce in TASK Group Holdings' shares has lifted the company's P/S handsomely. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've concluded that TASK Group Holdings currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Plus, you should also learn about this 1 warning sign we've spotted with TASK Group Holdings.

If these risks are making you reconsider your opinion on TASK Group Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if TASK Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:TSK

TASK Group Holdings

Engages in the development and sale of software applications primarily for the hospitality sector.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor