Advertisement

Here's Why We Think ReadCloud Limited's (ASX:RCL) CEO Compensation Looks Fair

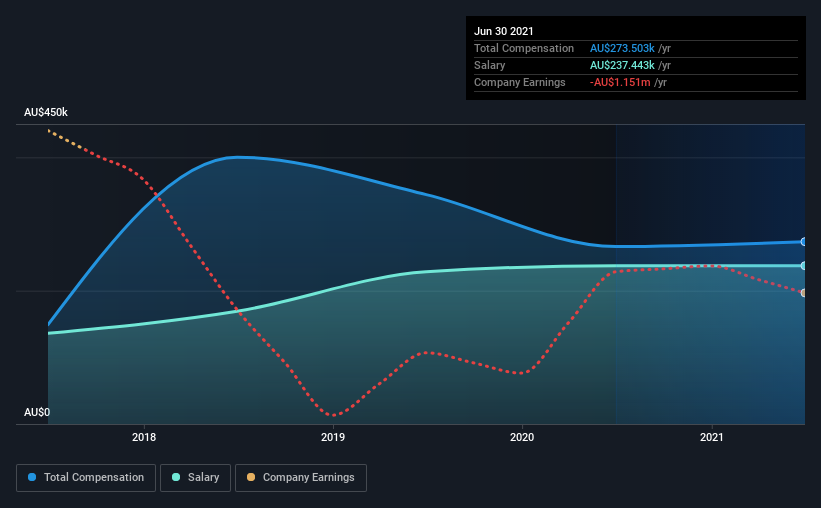

Performance at ReadCloud Limited (ASX:RCL) has been rather uninspiring recently and shareholders may be wondering how CEO Lars Lindstrom plans to fix this. They will get a chance to exercise their voting power to influence the future direction of the company in the next AGM on 23 November 2021. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. We think CEO compensation looks appropriate given the data we have put together.

View our latest analysis for ReadCloud

How Does Total Compensation For Lars Lindstrom Compare With Other Companies In The Industry?

Our data indicates that ReadCloud Limited has a market capitalization of AU$29m, and total annual CEO compensation was reported as AU$274k for the year to June 2021. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at AU$237.4k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations under AU$272m, the reported median total CEO compensation was AU$418k. This suggests that Lars Lindstrom is paid below the industry median. What's more, Lars Lindstrom holds AU$2.0m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | AU$237k | AU$237k | 87% |

| Other | AU$36k | AU$29k | 13% |

| Total Compensation | AU$274k | AU$266k | 100% |

On an industry level, roughly 63% of total compensation represents salary and 37% is other remuneration. It's interesting to note that ReadCloud pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at ReadCloud Limited's Growth Numbers

Over the past three years, ReadCloud Limited has seen its earnings per share (EPS) grow by 34% per year. Its revenue is up 3.2% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has ReadCloud Limited Been A Good Investment?

Given the total shareholder loss of 20% over three years, many shareholders in ReadCloud Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

The fact that shareholders have earned a negative share price return is certainly disconcerting. The share price trend has diverged with the robust growth in EPS however, suggesting there may be other factors that could be driving the price performance. A key question may be why the fundamentals have not yet been reflected into the share price. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for ReadCloud that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:RCL

ReadCloud

Provides eLearning software and industry based training solutions to schools and educational institutions in Australia.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor