Advertisement

We're Interested To See How LiveHire (ASX:LVH) Uses Its Cash Hoard To Grow

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So should LiveHire (ASX:LVH) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

See our latest analysis for LiveHire

When Might LiveHire Run Out Of Money?

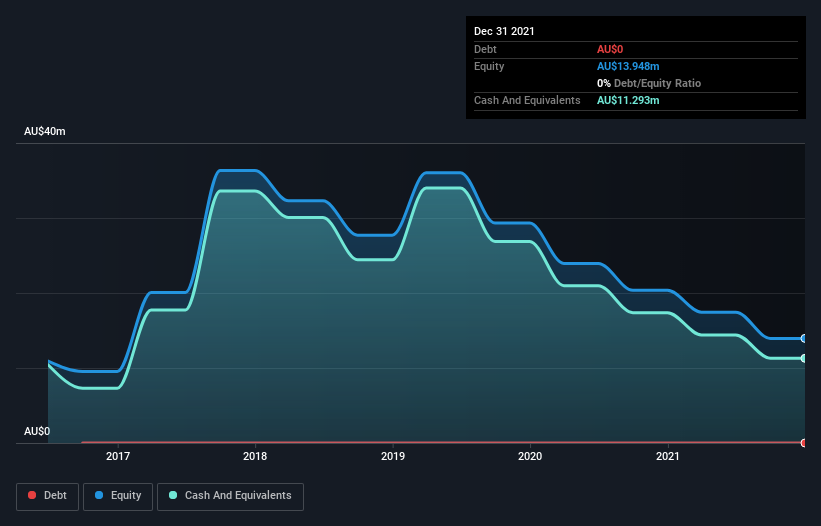

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When LiveHire last reported its balance sheet in December 2021, it had zero debt and cash worth AU$11m. In the last year, its cash burn was AU$6.7m. So it had a cash runway of approximately 20 months from December 2021. Importantly, the one analyst we see covering the stock thinks that LiveHire will reach cashflow breakeven in 2 years. That means it doesn't have a great deal of breathing room, but it shouldn't really need more cash, considering that cash burn should be continually reducing. The image below shows how its cash balance has been changing over the last few years.

How Well Is LiveHire Growing?

We reckon the fact that LiveHire managed to shrink its cash burn by 30% over the last year is rather encouraging. Having said that, the revenue growth of 67% was considerably more inspiring. It seems to be growing nicely. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can LiveHire Raise Cash?

While LiveHire seems to be in a decent position, we reckon it is still worth thinking about how easily it could raise more cash, if that proved desirable. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

LiveHire's cash burn of AU$6.7m is about 8.4% of its AU$80m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

Is LiveHire's Cash Burn A Worry?

As you can probably tell by now, we're not too worried about LiveHire's cash burn. For example, we think its revenue growth suggests that the company is on a good path. Its cash runway wasn't quite as good, but was still rather encouraging! One real positive is that at least one analyst is forecasting that the company will reach breakeven. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Its important for readers to be cognizant of the risks that can affect the company's operations, and we've picked out 4 warning signs for LiveHire that investors should know when investing in the stock.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:LVH

LiveHire

Develops talent acquisition software and engagement platform through software as a service and direct sourcing channels in Australia.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor