What We Learned About Growthpoint Properties Australia's (ASX:GOZ) CEO Pay

Tim Collyer has been the CEO of Growthpoint Properties Australia (ASX:GOZ) since 2010, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the funds from operations and shareholder returns of the company.

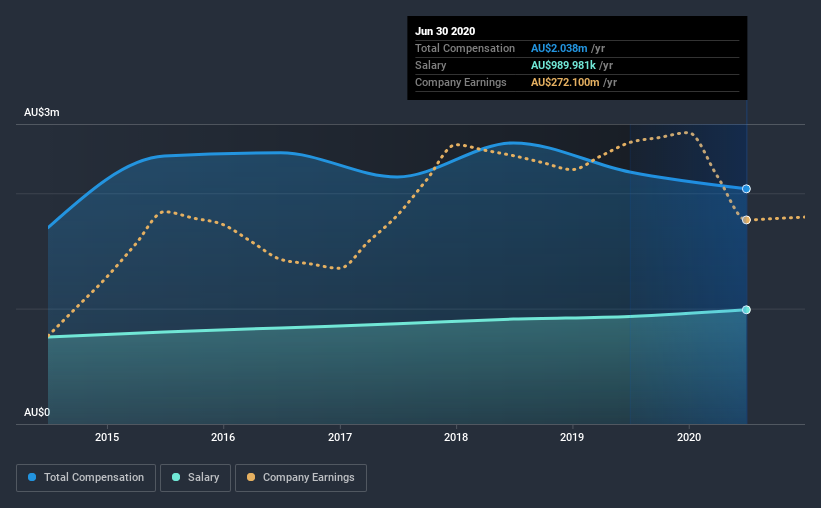

See our latest analysis for Growthpoint Properties Australia

Comparing Growthpoint Properties Australia's CEO Compensation With the industry

At the time of writing, our data shows that Growthpoint Properties Australia has a market capitalization of AU$2.5b, and reported total annual CEO compensation of AU$2.0m for the year to June 2020. That's a slight decrease of 6.7% on the prior year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$990k.

In comparison with other companies in the industry with market capitalizations ranging from AU$1.3b to AU$4.1b, the reported median CEO total compensation was AU$1.5m. Accordingly, our analysis reveals that Growthpoint Properties Australia pays Tim Collyer north of the industry median. Furthermore, Tim Collyer directly owns AU$3.8m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$990k | AU$933k | 49% |

| Other | AU$1.0m | AU$1.3m | 51% |

| Total Compensation | AU$2.0m | AU$2.2m | 100% |

On an industry level, roughly 57% of total compensation represents salary and 43% is other remuneration. Growthpoint Properties Australia pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Growthpoint Properties Australia's Growth Numbers

Growthpoint Properties Australia has seen its funds from operations (FFO) increase by 6.5% per year over the past three years. In the last year, its revenue is up 6.3%.

We would argue that the improvement in revenue is good, but isn't particularly impressive, but it is good to see modest FFO growth. It's clear the performance has been quite decent, but it it falls short of outstanding,based on this information. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Growthpoint Properties Australia Been A Good Investment?

Growthpoint Properties Australia has generated a total shareholder return of 20% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

As we noted earlier, Growthpoint Properties Australia pays its CEO higher than the norm for similar-sized companies belonging to the same industry. But the business isn't growing FFO, and the returns to shareholders haven't been wonderful. So while shareholders might not be overly concerned about CEO compensation, we suspect most would prefer to see improved performance, before thinking a bump in pay is in order.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 5 warning signs for Growthpoint Properties Australia (of which 2 make us uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you’re looking to trade Growthpoint Properties Australia, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:GOZ

Growthpoint Properties Australia

Our vision is to create sustainable value in everything we do, by being the forward-thinking, trusted partner of choice.

Undervalued average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion