Advertisement

- Australia

- /

- Real Estate

- /

- ASX:CWP

Cedar Woods Properties Limited (ASX:CWP) Stock Is Going Strong But Fundamentals Look Uncertain: What Lies Ahead ?

Cedar Woods Properties' (ASX:CWP) stock is up by a considerable 21% over the past three months. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Specifically, we decided to study Cedar Woods Properties' ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Cedar Woods Properties

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Cedar Woods Properties is:

5.5% = AU$21m ÷ AU$379m (Based on the trailing twelve months to June 2020).

The 'return' is the profit over the last twelve months. So, this means that for every A$1 of its shareholder's investments, the company generates a profit of A$0.06.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Cedar Woods Properties' Earnings Growth And 5.5% ROE

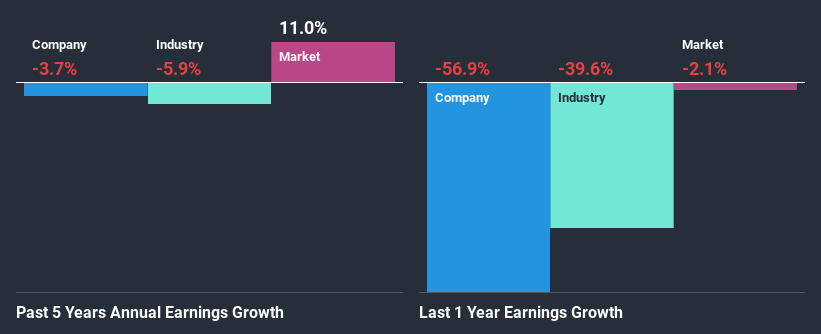

At first glance, Cedar Woods Properties' ROE doesn't look very promising. However, the fact that the company's ROE is higher than the average industry ROE of 3.5%, is definitely interesting. However, Cedar Woods Properties' five year net income decline rate was 3.7%. Remember, the company's ROE is a bit low to begin with, just that it is higher than the industry average. So that could be one of the factors that are causing earnings growth to shrink.

We then compared Cedar Woods Properties' performance with the industry and found that the company has shrunk its earnings at a slower rate than the industry earnings which has seen its earnings shrink by 5.9% in the same period. This does offer shareholders some relief

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is Cedar Woods Properties fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Cedar Woods Properties Making Efficient Use Of Its Profits?

With a high three-year median payout ratio of 52% (implying that 48% of the profits are retained), most of Cedar Woods Properties' profits are being paid to shareholders, which explains the company's shrinking earnings. With only very little left to reinvest into the business, growth in earnings is far from likely.

Moreover, Cedar Woods Properties has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 52% of its profits over the next three years. Regardless, the future ROE for Cedar Woods Properties is predicted to rise to 9.9% despite there being not much change expected in its payout ratio.

Conclusion

In total, we're a bit ambivalent about Cedar Woods Properties' performance. Primarily, we are disappointed to see a lack of growth in earnings even in spite of a moderate ROE. Bear in mind, the company reinvests a small portion of its profits, which explains the lack of growth. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

When trading Cedar Woods Properties or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:CWP

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor