Advertisement

- Australia

- /

- Entertainment

- /

- ASX:EVT

With 8.2% Earnings Growth, Did Event Hospitality & Entertainment Limited (ASX:EVT) Outperform The Industry?

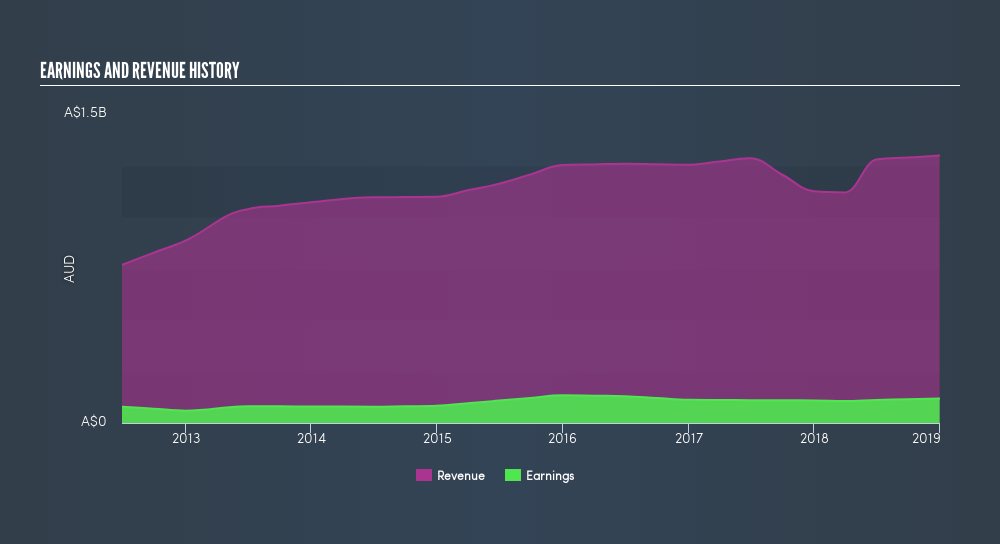

After reading Event Hospitality & Entertainment Limited's (ASX:EVT) most recent earnings announcement (31 December 2018), I found it useful to look back at how the company has performed in the past and compare this against the latest numbers. As a long term investor, I pay close attention to earnings trend, rather than the figures published at one point in time. I also compare against an industry benchmark to check whether Event Hospitality & Entertainment's performance has been impacted by industry movements. In this article I briefly touch on my key findings.

View our latest analysis for Event Hospitality & Entertainment

Commentary On EVT's Past Performance

EVT's trailing twelve-month earnings (from 31 December 2018) of AU$119m has increased by 8.2% compared to the previous year.

Furthermore, this one-year growth rate has exceeded its 5-year annual growth average of 5.6%, indicating the rate at which EVT is growing has accelerated. How has it been able to do this? Let's take a look at whether it is only a result of industry tailwinds, or if Event Hospitality & Entertainment has seen some company-specific growth.

In terms of returns from investment, Event Hospitality & Entertainment has fallen short of achieving a 20% return on equity (ROE), recording 11% instead. However, its return on assets (ROA) of 7.0% exceeds the AU Entertainment industry of 6.7%, indicating Event Hospitality & Entertainment has used its assets more efficiently. Though, its return on capital (ROC), which also accounts for Event Hospitality & Entertainment’s debt level, has declined over the past 3 years from 15% to 11%. This correlates with an increase in debt holding, with debt-to-equity ratio rising from 13% to 38% over the past 5 years.

What does this mean?

Though Event Hospitality & Entertainment's past data is helpful, it is only one aspect of my investment thesis. While Event Hospitality & Entertainment has a good historical track record with positive growth and profitability, there's no certainty that this will extrapolate into the future. I recommend you continue to research Event Hospitality & Entertainment to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for EVT’s future growth? Take a look at our free research report of analyst consensus for EVT’s outlook.

- Financial Health: Are EVT’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 December 2018. This may not be consistent with full year annual report figures.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:EVT

EVT

Engages in the entertainment business in Australia, New Zealand, Singapore, and Germany.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative