Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:VYS

Shareholders Will Probably Hold Off On Increasing Vysarn Limited's (ASX:VYS) CEO Compensation For The Time Being

Key Insights

- Vysarn will host its Annual General Meeting on 23rd of November

- CEO James Clement's total compensation includes salary of AU$382.5k

- Total compensation is 82% above industry average

- Over the past three years, Vysarn's EPS fell by 19% and over the past three years, the total shareholder return was 114%

Performance at Vysarn Limited (ASX:VYS) has been reasonably good and CEO James Clement has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 23rd of November. However, some shareholders will still be cautious of paying the CEO excessively.

Check out our latest analysis for Vysarn

How Does Total Compensation For James Clement Compare With Other Companies In The Industry?

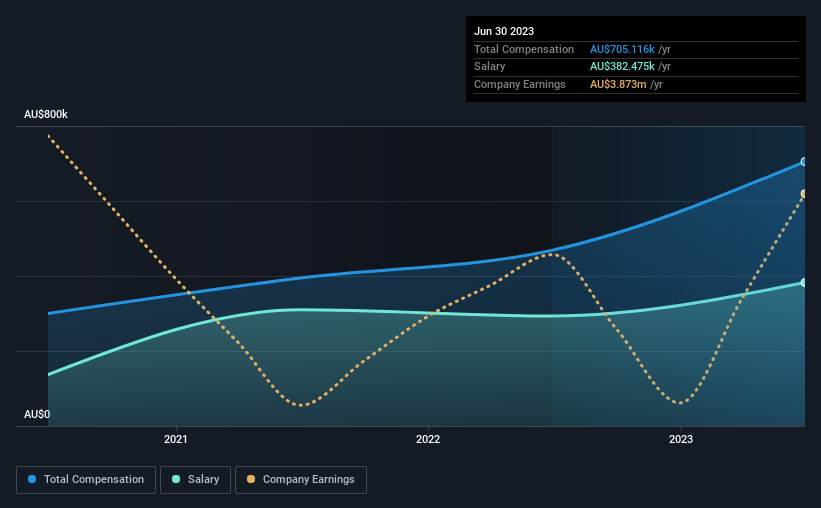

According to our data, Vysarn Limited has a market capitalization of AU$92m, and paid its CEO total annual compensation worth AU$705k over the year to June 2023. Notably, that's an increase of 50% over the year before. We note that the salary of AU$382.5k makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the Australian Metals and Mining industry with market capitalizations under AU$308m, the reported median total CEO compensation was AU$387k. Accordingly, our analysis reveals that Vysarn Limited pays James Clement north of the industry median. Furthermore, James Clement directly owns AU$3.8m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$382k | AU$293k | 54% |

| Other | AU$323k | AU$176k | 46% |

| Total Compensation | AU$705k | AU$469k | 100% |

On an industry level, roughly 61% of total compensation represents salary and 39% is other remuneration. In Vysarn's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Vysarn Limited's Growth Numbers

Over the last three years, Vysarn Limited has shrunk its earnings per share by 19% per year. Its revenue is up 40% over the last year.

Investors would be a bit wary of companies that have lower EPS On the other hand, the strong revenue growth suggests the business is growing. It's hard to reach a conclusion about business performance right now. This may be one to watch. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Vysarn Limited Been A Good Investment?

Most shareholders would probably be pleased with Vysarn Limited for providing a total return of 114% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Some shareholders will be pleased by the relatively good results, however, the results could still be improved. EPS growth is still weak, and until that picks up, shareholders may find it hard to approve a pay rise for the CEO, since they are already paid above the average in their industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Vysarn that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:VYS

Vysarn

Provides water services to various sectors, including resources, urban development, government and utilities in Australia.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor