- Australia

- /

- Metals and Mining

- /

- ASX:SFR

3 ASX Stocks Possibly Trading Up To 49.9% Below Intrinsic Value Estimates

Reviewed by Simply Wall St

Over the last 7 days, the Australian market has dropped 4.7%, but it is up 4.0% over the past year, with earnings expected to grow by 13% per annum over the next few years. In this context, identifying undervalued stocks that are trading below their intrinsic value can offer significant investment opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| LaserBond (ASX:LBL) | A$0.69 | A$1.38 | 49.8% |

| Regal Partners (ASX:RPL) | A$3.26 | A$6.40 | 49.1% |

| Shine Justice (ASX:SHJ) | A$0.70 | A$1.33 | 47.4% |

| Nanosonics (ASX:NAN) | A$2.97 | A$5.86 | 49.3% |

| Infomedia (ASX:IFM) | A$1.64 | A$3.07 | 46.6% |

| HMC Capital (ASX:HMC) | A$7.53 | A$13.84 | 45.6% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Life360 (ASX:360) | A$15.16 | A$28.19 | 46.2% |

| Sandfire Resources (ASX:SFR) | A$8.38 | A$16.73 | 49.9% |

| Airtasker (ASX:ART) | A$0.27 | A$0.52 | 48.6% |

We're going to check out a few of the best picks from our screener tool.

GenusPlus Group (ASX:GNP)

Overview: GenusPlus Group Limited (ASX:GNP) specializes in the installation, construction, and maintenance of power and communication systems in Australia, with a market cap of A$390.99 million.

Operations: Revenue Segments (in millions of A$): Industrial: 93.69, Communication: 67.14, Infrastructure: 318.32

Estimated Discount To Fair Value: 12.9%

GenusPlus Group is trading at A$2.20, which is 12.9% below its estimated fair value of A$2.53. The company’s earnings are forecast to grow significantly at 27.9% per year, outpacing the Australian market's growth rate of 12.9%. Revenue is also expected to rise by 17.1% annually, faster than the market average of 5.1%. Recent earnings growth was strong at 49.5%, indicating solid financial health and potential undervaluation based on cash flows.

- Upon reviewing our latest growth report, GenusPlus Group's projected financial performance appears quite optimistic.

- Get an in-depth perspective on GenusPlus Group's balance sheet by reading our health report here.

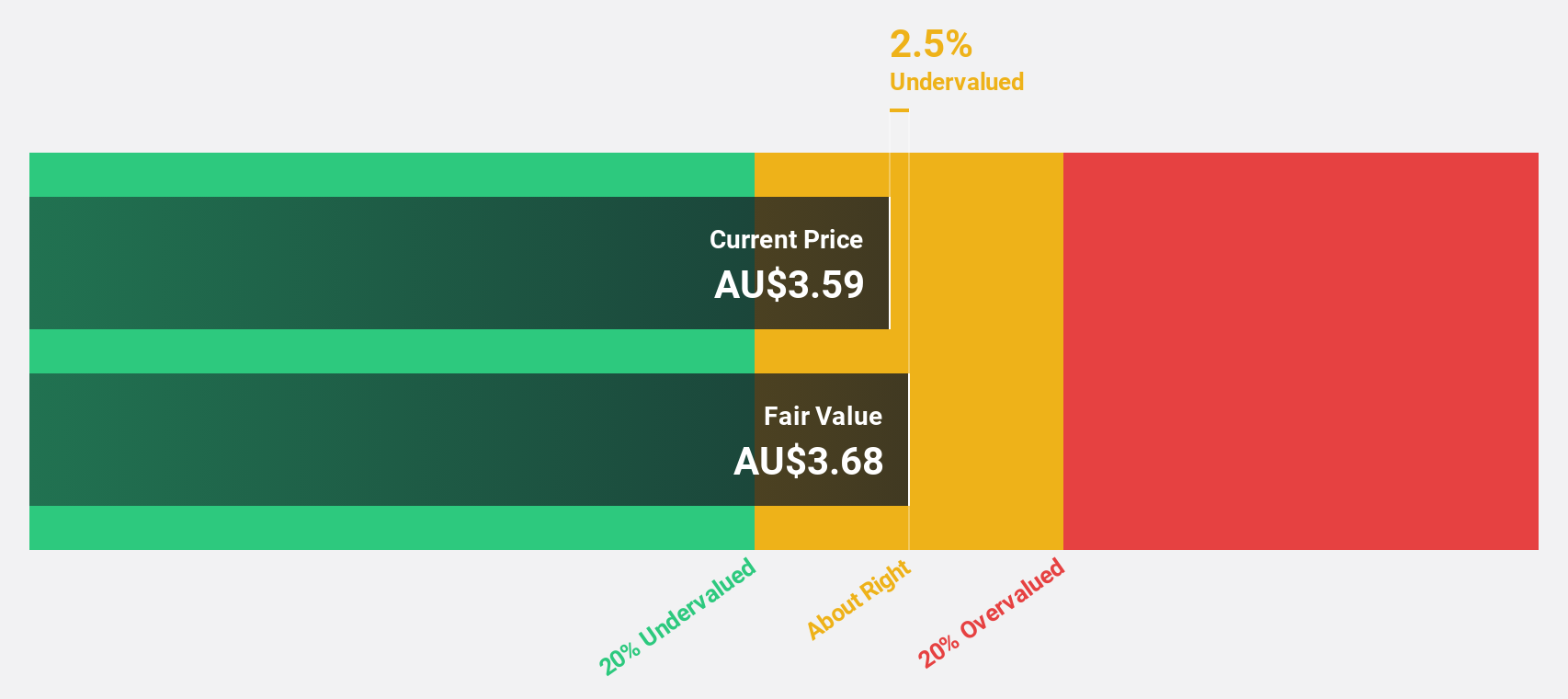

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources Limited, a mining company with a market cap of A$3.83 billion, focuses on the exploration, evaluation, and development of mineral tenements and projects.

Operations: The company's revenue segments include MATSA Copper Operations at $581.75 million and DeGrussa Copper Operations at $94.49 million.

Estimated Discount To Fair Value: 49.9%

Sandfire Resources is trading at A$8.38, significantly below its estimated fair value of A$16.73, indicating potential undervaluation based on cash flows. The company’s revenue is forecast to grow 12% annually, outpacing the Australian market's 5.1%. Earnings are expected to increase by 52.33% per year over the next three years, reflecting robust growth prospects despite a low forecasted return on equity of 12.4%.

- Insights from our recent growth report point to a promising forecast for Sandfire Resources' business outlook.

- Click to explore a detailed breakdown of our findings in Sandfire Resources' balance sheet health report.

Webjet (ASX:WEB)

Overview: Webjet Limited offers online travel booking services across Australia, New Zealand, the United Arab Emirates, the United Kingdom, and internationally with a market cap of A$3.34 billion.

Operations: The company generates revenue from three primary segments: Corporate (A$0.80 million), Business to Business Travel (B2B) (A$327.90 million), and Business to Consumer Travel (B2C) (A$142.80 million).

Estimated Discount To Fair Value: 26.2%

Webjet Limited, trading at A$8.55, is significantly undervalued compared to its estimated fair value of A$11.57 based on discounted cash flow analysis. The company reported robust earnings growth, with net income rising from A$14.5 million to A$72.7 million year-over-year. Revenue is forecasted to grow at 10.6% annually, outpacing the Australian market's 5.1%. The recent demerger plans and leadership changes could unlock further value and attract potential suitors for its assets.

- The analysis detailed in our Webjet growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Webjet.

Where To Now?

- Unlock more gems! Our Undervalued ASX Stocks Based On Cash Flows screener has unearthed 35 more companies for you to explore.Click here to unveil our expertly curated list of 38 Undervalued ASX Stocks Based On Cash Flows.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:SFR

Sandfire Resources

A mining company, engages in the exploration, evaluation, and development of mineral tenements and projects.

Good value with reasonable growth potential.