Advertisement

ASX Value Stocks Estimated Below Intrinsic Worth November 2025

Simply Wall St

Reviewed by Simply Wall St

Over the last seven days, the Australian market has experienced a 1.5% decline, yet it has risen by 9.4% over the past year with earnings forecasted to grow annually by 12%. In this context, identifying stocks that are trading below their intrinsic value can present potential opportunities for investors seeking to capitalize on future growth prospects in an evolving market.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Symal Group (ASX:SYL) | A$2.37 | A$4.63 | 48.8% |

| Superloop (ASX:SLC) | A$3.10 | A$5.66 | 45.3% |

| Resimac Group (ASX:RMC) | A$1.085 | A$2.17 | 50% |

| Regal Partners (ASX:RPL) | A$2.85 | A$4.91 | 41.9% |

| Reckon (ASX:RKN) | A$0.595 | A$1.19 | 49.8% |

| NRW Holdings (ASX:NWH) | A$4.82 | A$9.12 | 47.1% |

| James Hardie Industries (ASX:JHX) | A$31.68 | A$60.46 | 47.6% |

| IDP Education (ASX:IEL) | A$5.47 | A$10.53 | 48.1% |

| CleanSpace Holdings (ASX:CSX) | A$0.70 | A$1.38 | 49.3% |

| Airtasker (ASX:ART) | A$0.365 | A$0.72 | 49.1% |

Here's a peek at a few of the choices from the screener.

Infomedia (ASX:IFM)

Overview: Infomedia Ltd is a technology company that develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the global automotive industry, with a market cap of A$637.69 million.

Operations: The company's revenue segment includes A$146.51 million from publishing periodicals related to its technology solutions for the automotive sector.

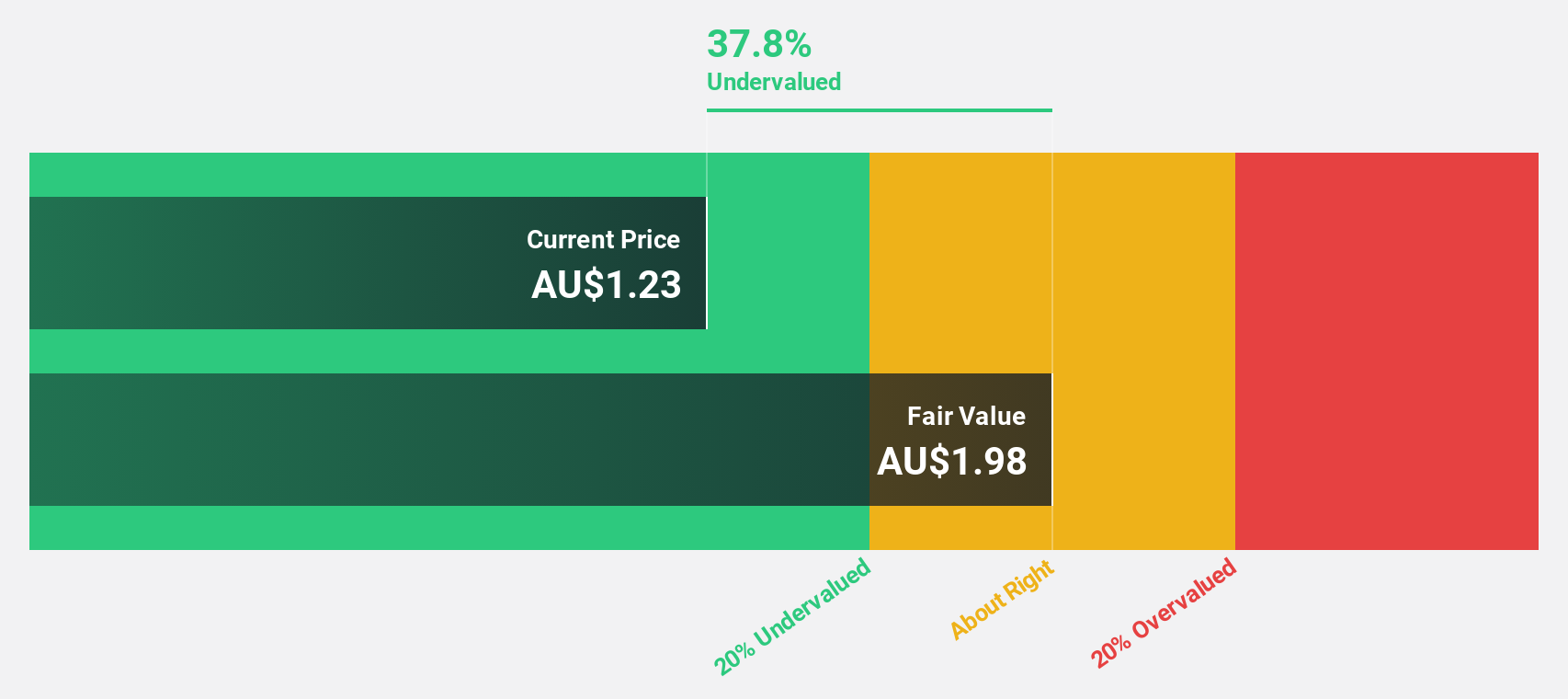

Estimated Discount To Fair Value: 18.9%

Infomedia is trading at A$1.69, below its estimated fair value of A$2.08, offering potential for investors seeking undervalued stocks based on cash flows. Despite a modest dividend yield of 2.49%, not fully covered by earnings, the company has shown robust profit growth with earnings increasing by 31.6% last year and forecasted to grow significantly over the next three years. Recent developments include a buyback completion and an acquisition offer from TPG Growth Capital Asia Limited valued at approximately A$650 million, which could impact its market position if approved by shareholders later this month.

- Insights from our recent growth report point to a promising forecast for Infomedia's business outlook.

- Click to explore a detailed breakdown of our findings in Infomedia's balance sheet health report.

Immutep (ASX:IMM)

Overview: Immutep Limited is a biotechnology company focused on developing novel Lymphocyte Activation Gene-3 related immunotherapies for cancer and autoimmune diseases in Australia, with a market cap of A$412.14 million.

Operations: The company's revenue primarily comes from its immunotherapy segment, generating A$5.03 million.

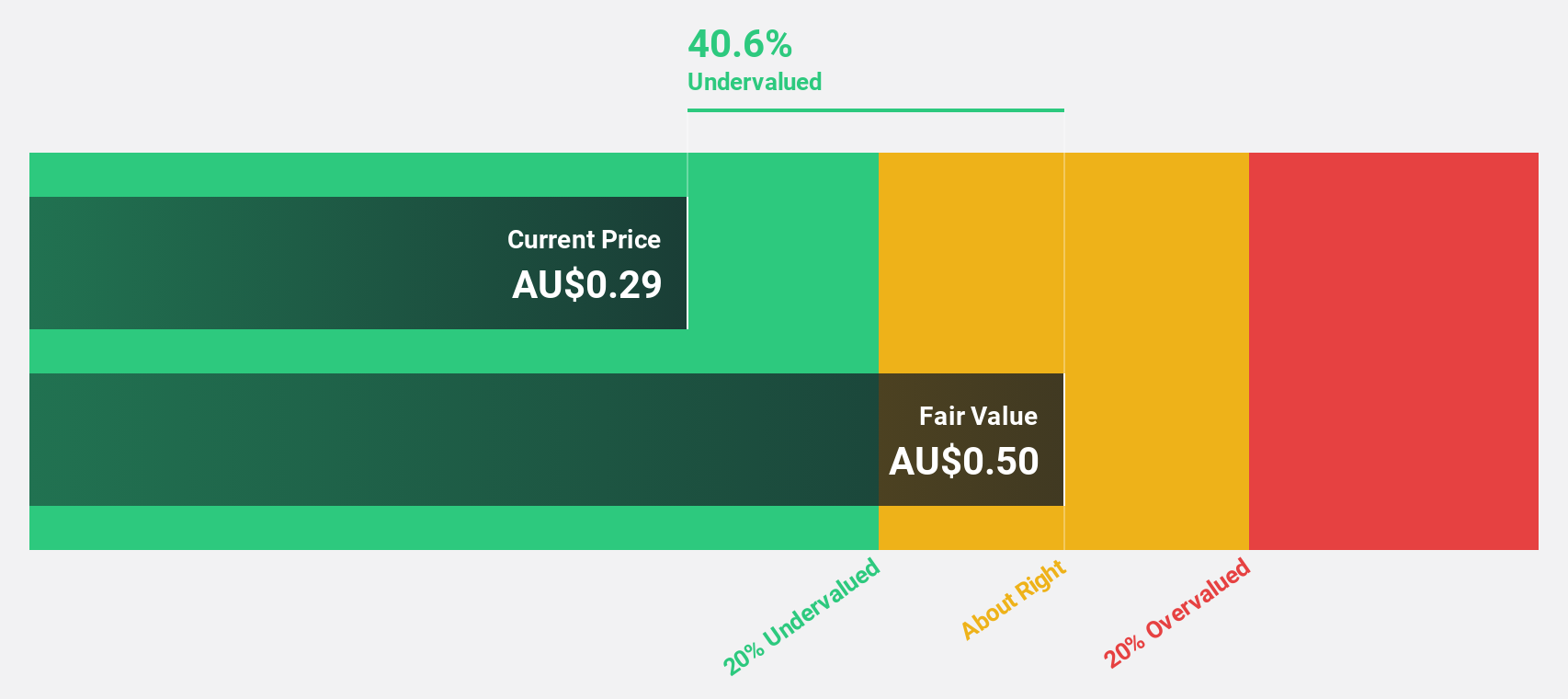

Estimated Discount To Fair Value: 40.8%

Immutep, trading at A$0.28, is significantly undervalued with an estimated fair value of A$0.47, presenting a potential opportunity for investors focused on cash flow-based valuations. Despite current unprofitability and a net loss of A$61.43 million for the year ending June 2025, its revenue growth forecast exceeds 100% annually—well above market averages—driven by promising clinical trial results in oncology treatments like eftilagimod alfa (efti) and strategic FDA feedback enhancing its development prospects.

- Our earnings growth report unveils the potential for significant increases in Immutep's future results.

- Dive into the specifics of Immutep here with our thorough financial health report.

Nickel Industries (ASX:NIC)

Overview: Nickel Industries Limited is involved in nickel ore mining and the production of nickel pig iron, cobalt, and nickel matte, with a market cap of A$3.15 billion.

Operations: The company's revenue segments consist of $120.89 million from nickel ore mining in Indonesia, $109.25 million from HPAL projects in Indonesia and Hong Kong, and $1.50 billion from RKEF projects in Indonesia and Singapore.

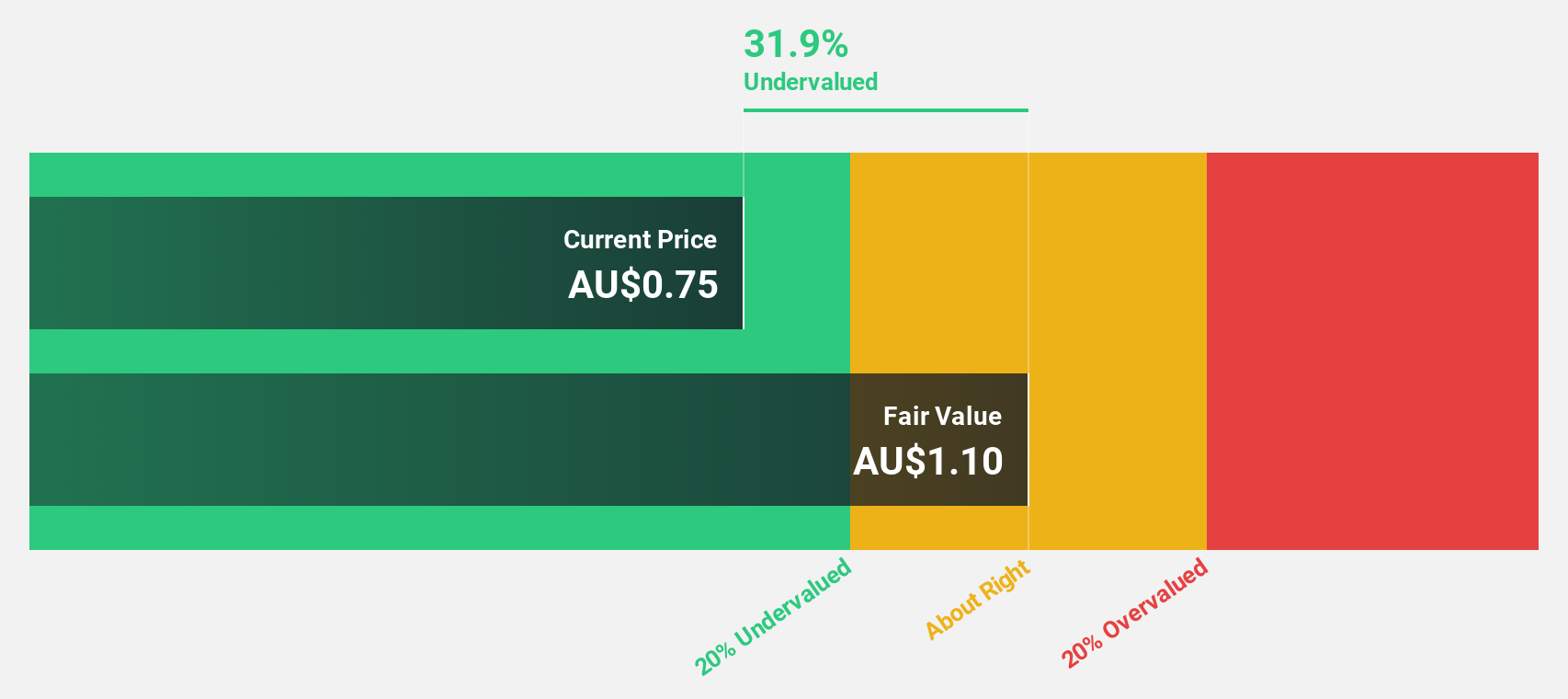

Estimated Discount To Fair Value: 30.8%

Nickel Industries, trading at A$0.73, is undervalued based on discounted cash flow analysis with a fair value estimate of A$1.05, offering a substantial margin for investors considering cash flow metrics. The company is forecast to achieve profitability within three years and expects annual earnings growth of 53.91%, outpacing the broader Australian market's revenue growth rate. Recent debt refinancing initiatives—an USD 800 million issuance extending debt maturity—strengthen its financial position for sustained expansion.

- Upon reviewing our latest growth report, Nickel Industries' projected financial performance appears quite optimistic.

- Take a closer look at Nickel Industries' balance sheet health here in our report.

Key Takeaways

- Discover the full array of 33 Undervalued ASX Stocks Based On Cash Flows right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:IFM

Infomedia

A technology company, develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor