Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:MGV

We Think Some Shareholders May Hesitate To Increase Musgrave Minerals Limited's (ASX:MGV) CEO Compensation

CEO Rob Waugh has done a decent job of delivering relatively good performance at Musgrave Minerals Limited (ASX:MGV) recently. As shareholders go into the upcoming AGM on 08 November 2022, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

Our analysis indicates that MGV is potentially overvalued!

Comparing Musgrave Minerals Limited's CEO Compensation With The Industry

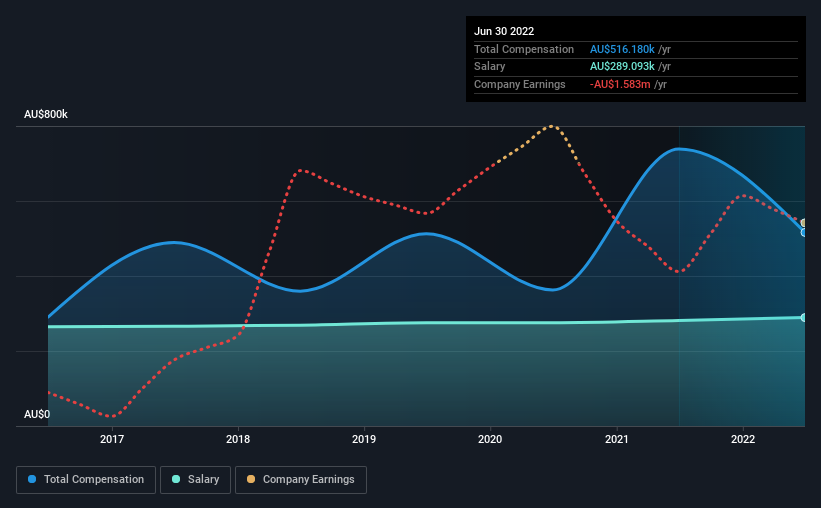

At the time of writing, our data shows that Musgrave Minerals Limited has a market capitalization of AU$122m, and reported total annual CEO compensation of AU$516k for the year to June 2022. Notably, that's a decrease of 30% over the year before. Notably, the salary which is AU$289.1k, represents a considerable chunk of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under AU$313m, the reported median total CEO compensation was AU$368k. Hence, we can conclude that Rob Waugh is remunerated higher than the industry median. Furthermore, Rob Waugh directly owns AU$1.9m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$289k | AU$281k | 56% |

| Other | AU$227k | AU$457k | 44% |

| Total Compensation | AU$516k | AU$739k | 100% |

Speaking on an industry level, nearly 60% of total compensation represents salary, while the remainder of 40% is other remuneration. Musgrave Minerals is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Musgrave Minerals Limited's Growth

Musgrave Minerals Limited has reduced its earnings per share by 31% a year over the last three years. It achieved revenue growth of 17% over the last year.

The reduction in EPS, over three years, is arguably concerning. But on the other hand, revenue growth is strong, suggesting a brighter future. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Musgrave Minerals Limited Been A Good Investment?

We think that the total shareholder return of 217%, over three years, would leave most Musgrave Minerals Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

The overall company performance has been commendable, however there are still areas for improvement. EPS growth is still weak, and until that picks up, shareholders may find it hard to approve a pay rise for the CEO, since they are already paid above the average in their industry.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 3 warning signs for Musgrave Minerals (1 is potentially serious!) that you should be aware of before investing here.

Important note: Musgrave Minerals is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:MGV

Musgrave Minerals

Musgrave Minerals Limited engages in the exploration and development of mineral properties in Australia.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor