- Australia

- /

- Metals and Mining

- /

- ASX:GRR

Is It Smart To Buy Grange Resources Limited (ASX:GRR) Before It Goes Ex-Dividend?

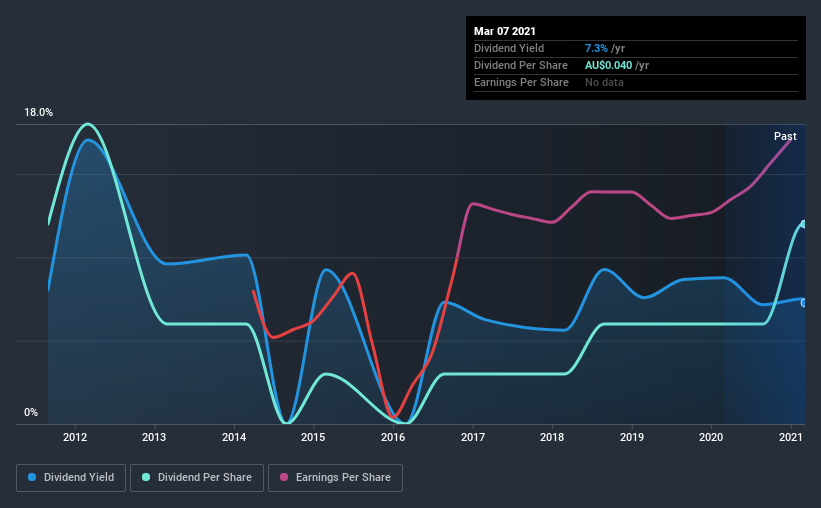

Grange Resources Limited (ASX:GRR) stock is about to trade ex-dividend in 4 days. Investors can purchase shares before the 12th of March in order to be eligible for this dividend, which will be paid on the 30th of March.

Grange Resources's next dividend payment will be AU$0.02 per share, on the back of last year when the company paid a total of AU$0.04 to shareholders. Based on the last year's worth of payments, Grange Resources has a trailing yield of 7.3% on the current stock price of A$0.55. If you buy this business for its dividend, you should have an idea of whether Grange Resources's dividend is reliable and sustainable. So we need to investigate whether Grange Resources can afford its dividend, and if the dividend could grow.

See our latest analysis for Grange Resources

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Grange Resources has a low and conservative payout ratio of just 17% of its income after tax. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out 16% of its free cash flow as dividends last year, which is conservatively low.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Grange Resources paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. It's encouraging to see Grange Resources has grown its earnings rapidly, up 52% a year for the past five years. Grange Resources looks like a real growth company, with earnings per share growing at a cracking pace and the company reinvesting most of its profits in the business.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. It looks like the Grange Resources dividends are largely the same as they were 10 years ago.

Final Takeaway

Should investors buy Grange Resources for the upcoming dividend? It's great that Grange Resources is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. It's disappointing to see the dividend has been cut at least once in the past, but as things stand now, the low payout ratio suggests a conservative approach to dividends, which we like. There's a lot to like about Grange Resources, and we would prioritise taking a closer look at it.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. For example - Grange Resources has 2 warning signs we think you should be aware of.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Grange Resources, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:GRR

Grange Resources

Owns and operates integrated iron ore mining and pellet production business in Australia and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion