Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:FMG

Fortescue (ASX:FMG) Valuation in Focus After Green Metal Breakthrough at Christmas Creek

Simply Wall St

Reviewed by Simply Wall St

Fortescue (ASX:FMG) recently announced the adoption of Metso’s technology as part of its Christmas Creek green metal project, which is currently underway in the Pilbara. This move highlights Fortescue’s ongoing push for low-emission steelmaking and a transition toward renewable energy-powered operations.

See our latest analysis for Fortescue.

Fortescue's push into green steelmaking is arriving alongside a year marked by strong investor returns and continued project activity. The share price is up 8.24% since January, and the total shareholder return over the past year sits at an impressive 21.77%. Recent momentum has been steady, with new technology partnerships and fresh exploration efforts keeping interest elevated in both the short term and the long term.

If you’re interested in uncovering more companies taking bold steps and showing solid momentum, now is the perfect time to broaden your search and discover fast growing stocks with high insider ownership

Given this track record and Fortescue's rapid push into green steel, investors may be weighing whether the stock remains undervalued or if the current price already reflects all the anticipated future growth potential.

Most Popular Narrative: 7.5% Overvalued

With Fortescue’s fair value recently updated to A$18.93, while shares are trading at A$20.36, the valuation narrative is heating up as analysts incorporate revised margin and growth assumptions into their models.

The analysts have a consensus price target of A$17.503 for Fortescue based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$20.11 and the most bearish reporting a price target of just A$15.45.

Want to see what’s driving Fortescue’s tight pricing? The real story includes falling profit margins and an aggressive profit multiple, which is unusual for miners. Which bold numbers are underpinning that price? The core assumptions might surprise you.

Result: Fair Value of $18.93 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a sharp rebound in Chinese steel demand or successful execution of Fortescue’s green initiatives could quickly change the current valuation outlook.

Find out about the key risks to this Fortescue narrative.

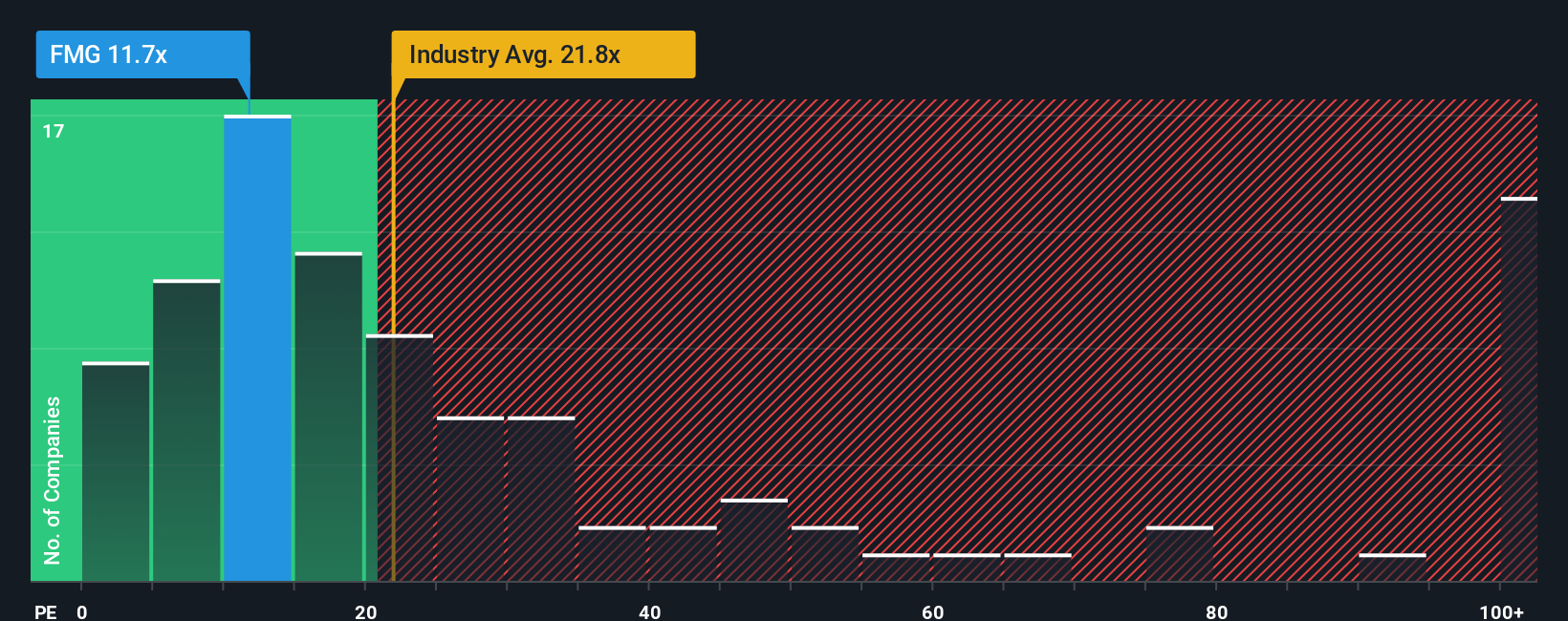

Another View: Market Ratios Signal Opportunity

While analysts see Fortescue as slightly overvalued compared to their price target, traditional price-to-earnings ratios tell a more optimistic story. At 12x earnings, its valuation sits well below the Australian industry average of 20.7x, the peer average of 60.1x, and even under its fair ratio of 17.3x. Such a gap could indicate hidden upside or suggest the market is factoring in risks others miss. Which outlook will ultimately prove right?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fortescue Narrative

If you see things differently or want to form your own views, it only takes a few minutes to shape your own Fortescue story. Why not Do it your way

A great starting point for your Fortescue research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for More Winning Ideas?

Don’t let your next big investment pass you by. Use the Simply Wall Street Screener to spot emerging opportunities you might otherwise miss.

- Boost your portfolio’s stability and income by checking out these 15 dividend stocks with yields > 3% offering reliable yields above 3%.

- Supercharge your growth prospects as you tap into innovation leaders with these 27 AI penny stocks reshaping industries through artificial intelligence breakthroughs.

- Take advantage of the market’s mispricings and get ahead with these 897 undervalued stocks based on cash flows based on real cash flows, not just hype.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FMG

Fortescue

Engages in the exploration, development, production, processing, and sale of iron ore in Australia, China, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor