Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:EVN

Evolution Mining (ASX:EVN): Valuation Check After Strategic Lithium JV Expansion in Nevada

Evolution Mining (ASX:EVN) has just deepened its push into battery metals, lifting its stake to roughly 26% in the Nevada North Lithium joint venture and funding the next exploration phase in Nevada.

See our latest analysis for Evolution Mining.

The stronger position in Nevada North Lithium seems to be feeding into sentiment, with Evolution’s 90 day share price return of 28.89% and one year total shareholder return of 159.26% suggesting momentum is still building from a much longer upswing.

If this lithium move has you rethinking where growth might come from next, it could be worth scanning fast growing stocks with high insider ownership for other under the radar compounders.

Yet with the shares trading above consensus price targets after a huge run, investors now face a tougher question: Is Evolution still trading below its long term potential, or is the market already baking in years of growth?

Most Popular Narrative Narrative: 24.8% Overvalued

With Evolution Mining closing at A$12.76 against a narrative fair value near A$10.23, the most followed view sees expectations already running ahead of fundamentals.

The analysts have a consensus price target of A$7.222 for Evolution Mining based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$8.9, and the most bearish reporting a price target of just A$3.8.

Curious how modest revenue growth, rising margins and a punchy future earnings multiple can still point to downside from here? The narrative presents a detailed earnings bridge, layers in dilution, then discounts it all back at a precise required return. Want to see which assumptions carry the most weight in that A$10.23 fair value estimate?

Result: Fair Value of A$10.23 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained gold price strength and disciplined cost control could preserve Evolution’s margins, supporting earnings resilience and challenging the current overvaluation narrative.

Find out about the key risks to this Evolution Mining narrative.

Another Take on Valuation

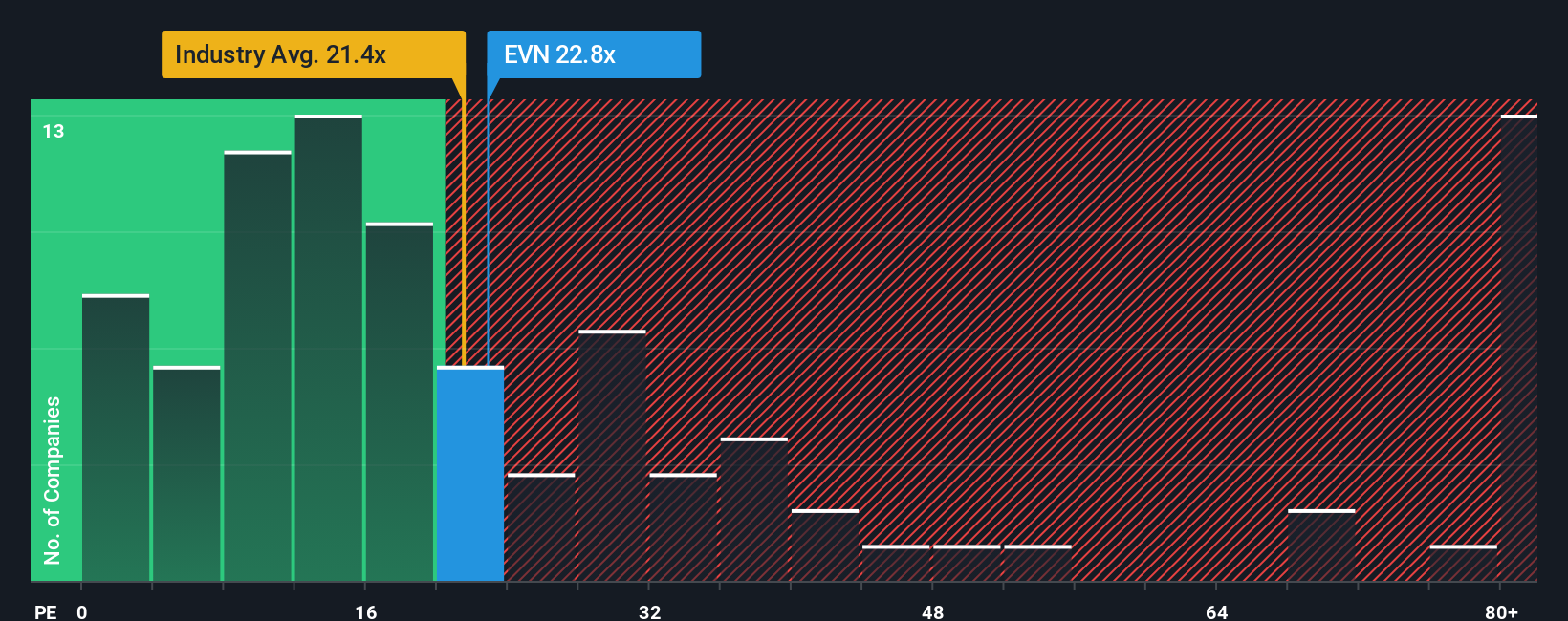

While the narrative fair value points to downside, our price to earnings work paints a milder picture. EVN trades at 28 times earnings versus an Australian metals and mining average of 21.9 times and a fair ratio of 23.6 times, implying a rich but not outrageous premium. Is that extra multiple headroom a warning sign, or simply the cost of owning a proven compounder?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Evolution Mining Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a full narrative in minutes using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Evolution Mining.

Looking for more investment ideas?

Do not stop at just one opportunity. Let Simply Wall St’s screener surface more focused ideas so you do not miss the next big move.

- Capitalize on market mispricing by using these 904 undervalued stocks based on cash flows that may be trading well below their intrinsic value based on future cash flows.

- Ride powerful technological shifts by targeting these 25 AI penny stocks shaping automation, data intelligence and next generation software.

- Strengthen your long term income stream through these 12 dividend stocks with yields > 3% that combine reliable payouts with resilient fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evolution Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EVN

Evolution Mining

Engages in the exploration, mine development and operation, and sale of gold and gold-copper concentrates in Australia and Canada.

Outstanding track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7060.2% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.226.4% undervalued

32 followersusers have followed this narrative

7 commentsusers have commented on this narrative

10 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0542.8% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.9% undervalued

85 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CSL ·

CSL Investment Thesis

Fair Value:AU$14026.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VA

Valtersa on Mouwasat Medical Services ·

Mouwasat Medical Services Will Achieve a 25% Profit Margin in Just 3 Years

Fair Value:ر.س98.634.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9724.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1935.7% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0