Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:EVN

Assessing Evolution Mining’s Valuation After Record Half Year Profit And Higher Fully Franked Dividend

What Evolution’s record half year means for shareholders

Evolution Mining (ASX:EVN) has reported record half year numbers, with revenue of A$2,794.35 million and net profit of A$766.57 million, alongside a fully franked interim dividend of A$0.20 per share.

For you as an investor, the combination of higher earnings per share, lower net debt over the past two years and a materially larger dividend sits at the centre of the current investment story.

See our latest analysis for Evolution Mining.

Those record half year results and the higher fully franked dividend have arrived after a strong period for the stock, with a 21.72% 1 month share price return, a 38.55% 3 month share price return and a very large 1 year total shareholder return, even though the latest 1 day move was a 1.54% share price decline to A$16.03.

If strong gold exposure is on your radar after Evolution Mining’s run, it may be a time to scan other producers using our 21 elite gold producer stocks as a starting point for ideas.

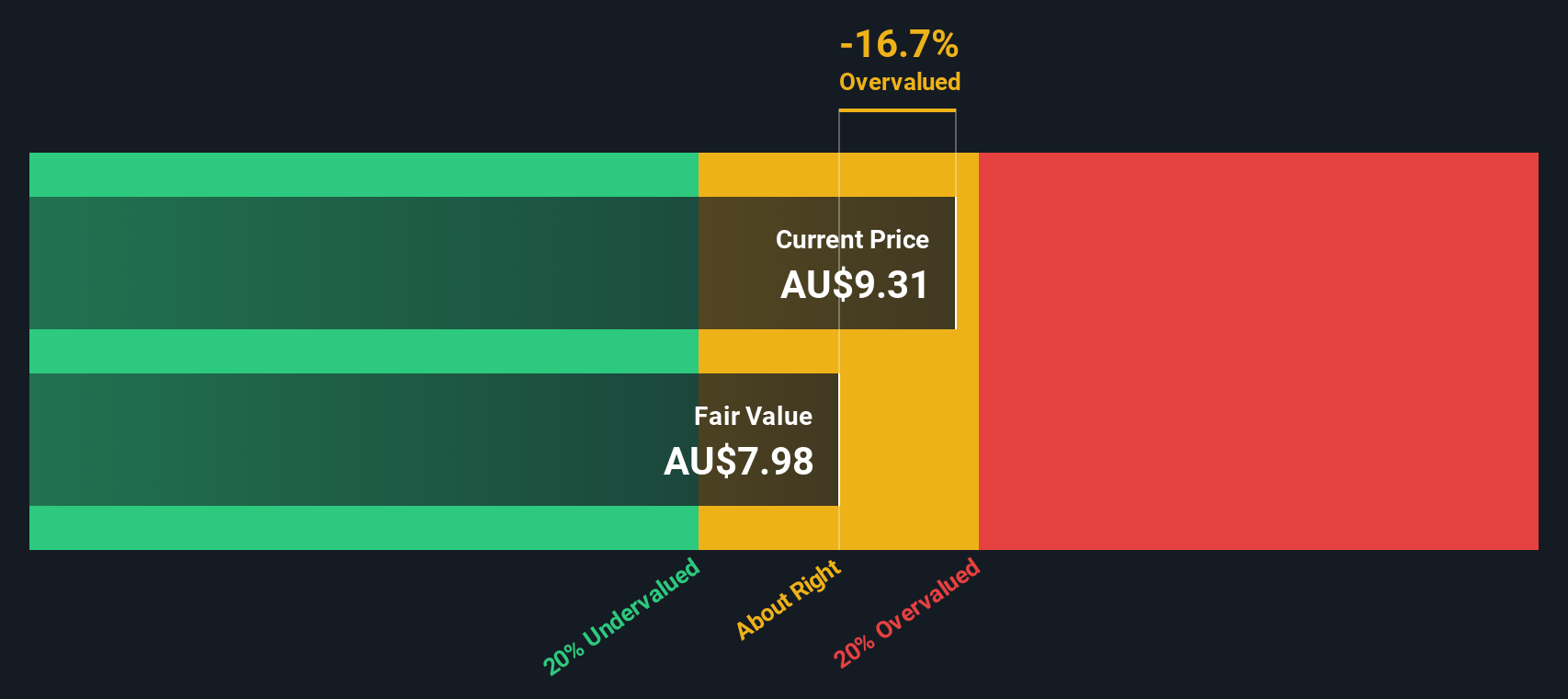

With the share price up sharply and our DCF work suggesting Evolution Mining may be very expensive relative to its intrinsic value, you need to ask yourself whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 26.9% Overvalued

The most widely followed valuation narrative puts Evolution Mining’s fair value at A$12.63 per share, well below the latest close at A$16.03. This sets up a clear tension between modelled worth and current market pricing.

The analysts have a consensus price target of A$7.222 for Evolution Mining based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$8.9, and the most bearish reporting a price target of just A$3.8.

Want to see what is sitting behind that A$12.63 fair value and wide price target spread? The narrative leans heavily on future revenue, earnings and margin assumptions that could surprise you.

Result: Fair Value of A$12.63 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if gold prices stay stronger for longer, or Evolution keeps managing costs tightly, current earnings and cash flow assumptions could prove too conservative.

Find out about the key risks to this Evolution Mining narrative.

Another way to look at the price tag

Our DCF work points to a fair value of A$6.73 per share, far below the current A$16.03 price. This flags Evolution Mining as expensive on this model. If the cash flow assumptions are even roughly right, you have to ask how much valuation risk you are comfortable carrying.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Evolution Mining Narrative

If you are not convinced by this view or you simply prefer to lean on your own research and judgement, you can pull the numbers, stress test the assumptions and build a version of the story that fits your outlook, then Do it your way in less than 3 minutes.

A great starting point for your Evolution Mining research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Evolution Mining is already on your watchlist, do not stop there. Broaden your opportunity set and pressure test your portfolio against other angles the market might be missing.

- Spot potential mispricing early by scanning our 10 high quality undervalued stocks that highlights companies combining strong fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your income stream by reviewing 9 dividend fortresses where companies with higher yields and robust payout histories are grouped for quick comparison.

- Prioritise resilience by checking 5 resilient stocks with low risk scores focusing on businesses with lower risk scores so you can focus more on long term compounding and less on surprises.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evolution Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EVN

Evolution Mining

Engages in the exploration, mine development and operation, and sale of gold and gold-copper concentrates in Australia and Canada.

Outstanding track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.1% undervalued

210 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

53 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.6% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.1% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36039.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Fibromat (M) Berhad ·

Fibromat: More than just a niche player, with clearer earnings visibility from order book and project wins

Fair Value:RM 1.0519.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k36.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.5% undervalued

1348 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0