Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:DRR

Deterra Royalties Limited's (ASX:DRR) Share Price Could Signal Some Risk

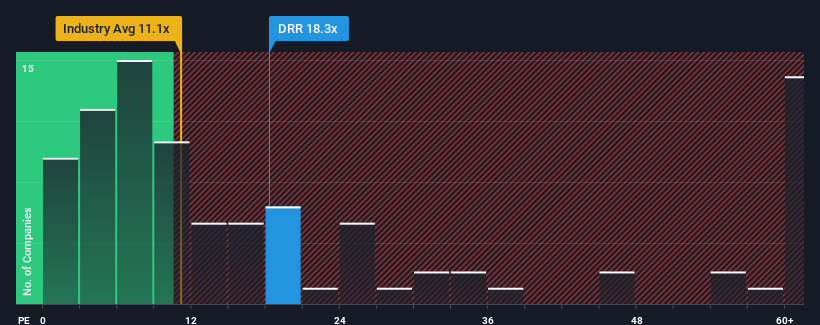

With a median price-to-earnings (or "P/E") ratio of close to 19x in Australia, you could be forgiven for feeling indifferent about Deterra Royalties Limited's (ASX:DRR) P/E ratio of 18.3x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times haven't been advantageous for Deterra Royalties as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. You'd much rather the company wasn't bleeding earnings if you still believe in the business. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

View our latest analysis for Deterra Royalties

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Deterra Royalties would need to produce growth that's similar to the market.

Retrospectively, the last year delivered a frustrating 15% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 158% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the eleven analysts covering the company suggest earnings should grow by 0.5% each year over the next three years. That's shaping up to be materially lower than the 17% each year growth forecast for the broader market.

With this information, we find it interesting that Deterra Royalties is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Deterra Royalties' analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

You need to take note of risks, for example - Deterra Royalties has 2 warning signs (and 1 which can't be ignored) we think you should know about.

You might be able to find a better investment than Deterra Royalties. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:DRR

Deterra Royalties

Operates as a royalty investment company in Australia, the United States, Mexico, Zambia, Peru, Canada, Mali, Kenya, Brazil, Cote D’Ivoire, and South Africa.

Fair value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor