Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:DEG

We Discuss Why De Grey Mining Limited's (ASX:DEG) CEO May Deserve A Higher Pay Packet

Shareholders will be pleased by the robust performance of De Grey Mining Limited (ASX:DEG) recently and this will be kept in mind in the upcoming AGM on 24 November 2022. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. Here is our take on why we think CEO compensation is fair and may even warrant a raise.

Our analysis indicates that DEG is potentially overvalued!

How Does Total Compensation For Glenn R. Jardine Compare With Other Companies In The Industry?

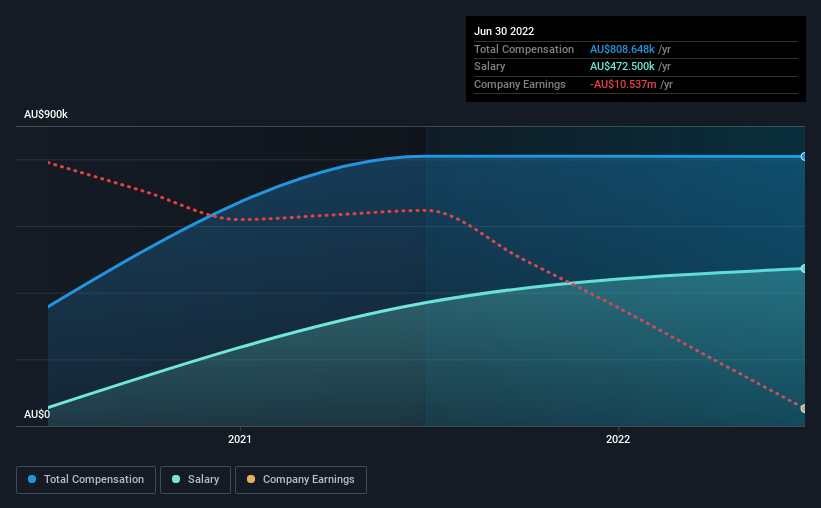

According to our data, De Grey Mining Limited has a market capitalization of AU$1.9b, and paid its CEO total annual compensation worth AU$809k over the year to June 2022. This means that the compensation hasn't changed much from last year. In particular, the salary of AU$472.5k, makes up a fairly large portion of the total compensation being paid to the CEO.

On comparing similar companies from the same industry with market caps ranging from AU$1.5b to AU$4.7b, we found that the median CEO total compensation was AU$1.7m. This suggests that Glenn R. Jardine is paid below the industry median. What's more, Glenn R. Jardine holds AU$173k worth of shares in the company in their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$473k | AU$370k | 58% |

| Other | AU$336k | AU$439k | 42% |

| Total Compensation | AU$809k | AU$809k | 100% |

Speaking on an industry level, nearly 60% of total compensation represents salary, while the remainder of 40% is other remuneration. There isn't a significant difference between De Grey Mining and the broader market, in terms of salary allocation in the overall compensation package. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

De Grey Mining Limited's Growth

De Grey Mining Limited has reduced its earnings per share by 19% a year over the last three years. It achieved revenue growth of 47% over the last year.

The decrease in EPS could be a concern for some investors. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. It's hard to reach a conclusion about business performance right now. This may be one to watch. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has De Grey Mining Limited Been A Good Investment?

Most shareholders would probably be pleased with De Grey Mining Limited for providing a total return of 2,410% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 5 warning signs for De Grey Mining (3 are potentially serious!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:DEG

De Grey Mining

Engages in the exploration of mineral properties in Australia.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor