- Australia

- /

- Metals and Mining

- /

- ASX:ARR

Introducing Broken Hill Prospecting (ASX:BPL), The Stock That Slid 68% In The Last Year

Broken Hill Prospecting Limited (ASX:BPL) shareholders should be happy to see the share price up 15% in the last week. But that doesn't change the fact that the returns over the last year have been disappointing. During that time the share price has sank like a stone, descending 68%. The share price recovery is not so impressive when you consider the fall. Of course, it could be that the fall was overdone.

Check out our latest analysis for Broken Hill Prospecting

We don't think Broken Hill Prospecting's revenue of AU$160,028 is enough to establish significant demand. We can't help wondering why it's publicly listed so early in its journey. Are venture capitalists not interested? As a result, we think it's unlikely shareholders are paying much attention to current revenue, but rather speculating on growth in the years to come. For example, investors may be hoping that Broken Hill Prospecting finds some valuable resources, before it runs out of money.

As a general rule, if a company doesn't have much revenue, and it loses money, then it is a high risk investment. The is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies do very well over the long term, others become hyped up by promoters before eventually falling back down to earth, and going bankrupt (or being recapitalized). It certainly is a dangerous place to invest, as Broken Hill Prospecting investors might realise.

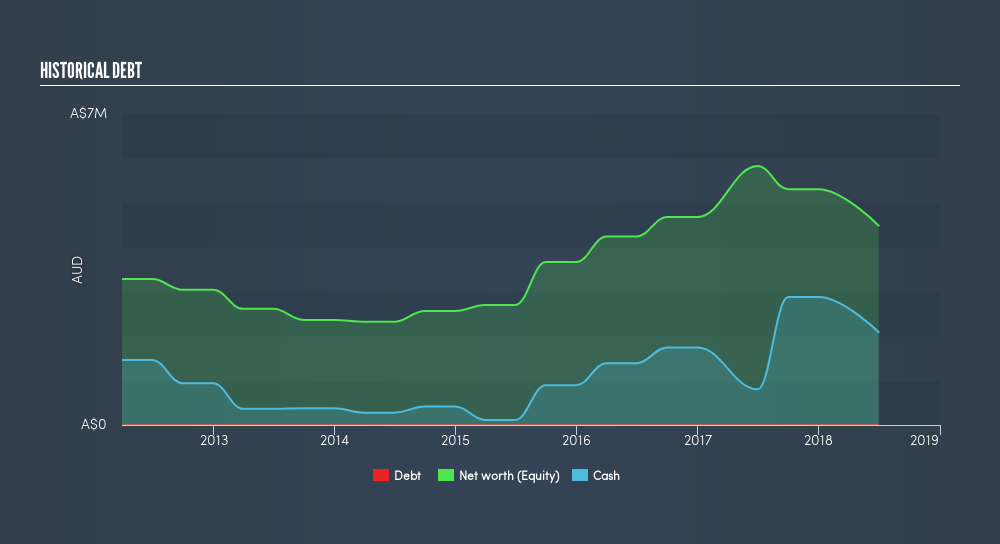

When it last reported its balance sheet in June 2018, Broken Hill Prospecting had net cash of AU$1.8m. While that's nothing to panic about, there is some possibility the company will raise more capital, especially if profits are not imminent. With the share price down 68% in the last year, it seems likely that the need for cash is weighing on investors' minds. You can click on the image below to see (in greater detail) how Broken Hill Prospecting's cash and debt levels have changed over time.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. Given that situation, would you be concerned if it turned out insiders were relentlessly selling stock? It would bother me, that's for sure. You can click here to see if there are insiders selling.

What about the Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Broken Hill Prospecting's total shareholder return (TSR) and its share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings. We note that Broken Hill Prospecting's TSR, at -68% is higher than its share price rise of -68%. When you consider it hasn't been paying a dividend, this data suggests shareholders may have had the opportunity to acquire attractively priced shares in a discounted capital raising.

A Different Perspective

Broken Hill Prospecting shareholders are down 68% for the year, but the market itself is up 8.4%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 9.0% per year over five years. We realise that Buffett has said investors should 'buy when there is blood on the streets', but we caution that investors should first be sure they are buying a high quality businesses. You might want to assess this data-rich visualization of its earnings, revenue and cash flow.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this freelist of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:ARR

American Rare Earths

Explores and develops mineral resources in the United States.

Flawless balance sheet with low risk.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion