Advertisement

With EPS Growth And More, QBE Insurance Group (ASX:QBE) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like QBE Insurance Group (ASX:QBE). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide QBE Insurance Group with the means to add long-term value to shareholders.

See our latest analysis for QBE Insurance Group

How Fast Is QBE Insurance Group Growing Its Earnings Per Share?

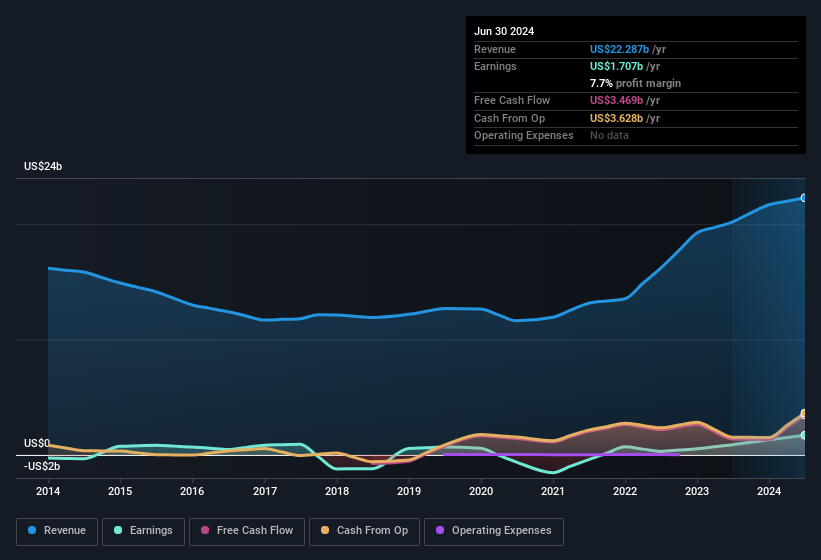

QBE Insurance Group has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. So it would be better to isolate the growth rate over the last year for our analysis. Outstandingly, QBE Insurance Group's EPS shot from US$0.60 to US$1.13, over the last year. It's a rarity to see 90% year-on-year growth like that.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The good news is that QBE Insurance Group is growing revenues, and EBIT margins improved by 6.9 percentage points to 12%, over the last year. Ticking those two boxes is a good sign of growth, in our book.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for QBE Insurance Group?

Are QBE Insurance Group Insiders Aligned With All Shareholders?

Owing to the size of QBE Insurance Group, we wouldn't expect insiders to hold a significant proportion of the company. But we are reassured by the fact they have invested in the company. As a matter of fact, their holding is valued at US$25m. That shows significant buy-in, and may indicate conviction in the business strategy. Despite being just 0.08% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Is QBE Insurance Group Worth Keeping An Eye On?

QBE Insurance Group's earnings have taken off in quite an impressive fashion. That EPS growth certainly is attention grabbing, and the large insider ownership only serves to further stoke our interest. At times fast EPS growth is a sign the business has reached an inflection point, so there's a potential opportunity to be had here. Based on the sum of its parts, we definitely think its worth watching QBE Insurance Group very closely. It is worth noting though that we have found 1 warning sign for QBE Insurance Group that you need to take into consideration.

Although QBE Insurance Group certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of Australian companies that not only boast of strong growth but have strong insider backing.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if QBE Insurance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:QBE

QBE Insurance Group

Engages in underwriting general insurance and reinsurance risks in the Australia Pacific, North America, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor