Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that LBT Innovations Limited (ASX:LBT) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for LBT Innovations

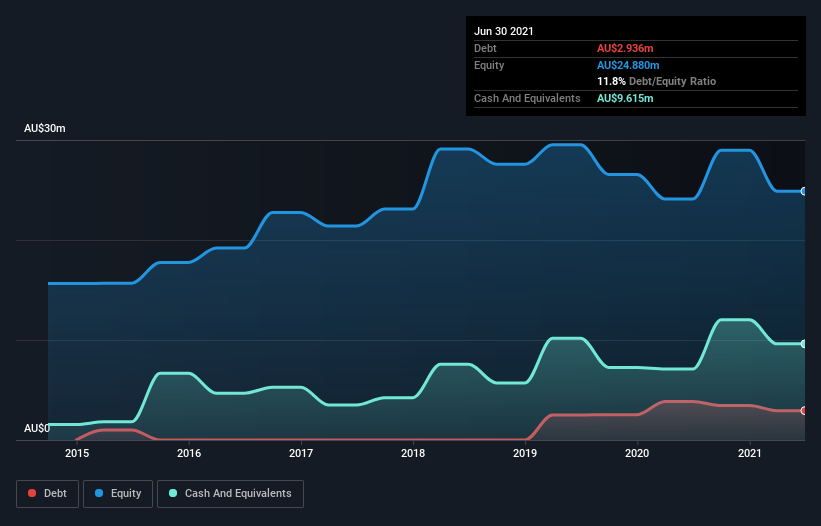

What Is LBT Innovations's Net Debt?

As you can see below, LBT Innovations had AU$2.94m of debt at June 2021, down from AU$3.86m a year prior. However, it does have AU$9.62m in cash offsetting this, leading to net cash of AU$6.68m.

How Strong Is LBT Innovations' Balance Sheet?

We can see from the most recent balance sheet that LBT Innovations had liabilities of AU$2.58m falling due within a year, and liabilities of AU$8.23m due beyond that. On the other hand, it had cash of AU$9.62m and AU$1.95m worth of receivables due within a year. So it actually has AU$758.0k more liquid assets than total liabilities.

Having regard to LBT Innovations' size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the AU$39.0m company is short on cash, but still worth keeping an eye on the balance sheet. Simply put, the fact that LBT Innovations has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since LBT Innovations will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Since LBT Innovations doesn't have significant operating revenue, shareholders must hope it'll ramp sales of its new medical tech as soon as possible.

So How Risky Is LBT Innovations?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that LBT Innovations had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of AU$3.3m and booked a AU$7.3m accounting loss. But at least it has AU$6.68m on the balance sheet to spend on growth, near-term. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for LBT Innovations (2 can't be ignored) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade LBT Innovations, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:CC5

Clever Culture Systems

Engages in the research, development, and commercialization of technology solutions for medical industry in Australia, the United States, Sweden, the United Kingdom, China, Netherlands, and Germany.

Moderate risk with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor