Advertisement

Inghams Group Limited's (ASX:ING) Low P/E No Reason For Excitement

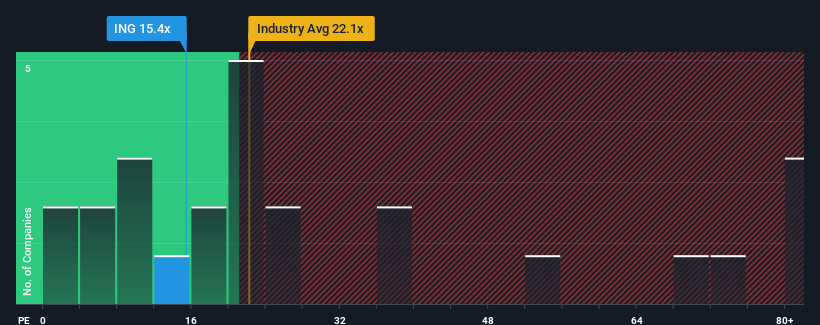

Inghams Group Limited's (ASX:ING) price-to-earnings (or "P/E") ratio of 15.4x might make it look like a buy right now compared to the market in Australia, where around half of the companies have P/E ratios above 18x and even P/E's above 32x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Inghams Group hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Inghams Group

Is There Any Growth For Inghams Group?

There's an inherent assumption that a company should underperform the market for P/E ratios like Inghams Group's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 16%. This has erased any of its gains during the last three years, with practically no change in EPS being achieved in total. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 12% each year as estimated by the ten analysts watching the company. That's shaping up to be materially lower than the 15% each year growth forecast for the broader market.

In light of this, it's understandable that Inghams Group's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Inghams Group maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Inghams Group (of which 1 is significant!) you should know about.

If these risks are making you reconsider your opinion on Inghams Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ING

Inghams Group

Engages in the production and sale of chicken and turkey products under the Ingham’s brand primarily in Australia and New Zealand.

Undervalued with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor