Advertisement

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So, the natural question for Berkeley Energia (ASX:BKY) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Berkeley Energia

Does Berkeley Energia Have A Long Cash Runway?

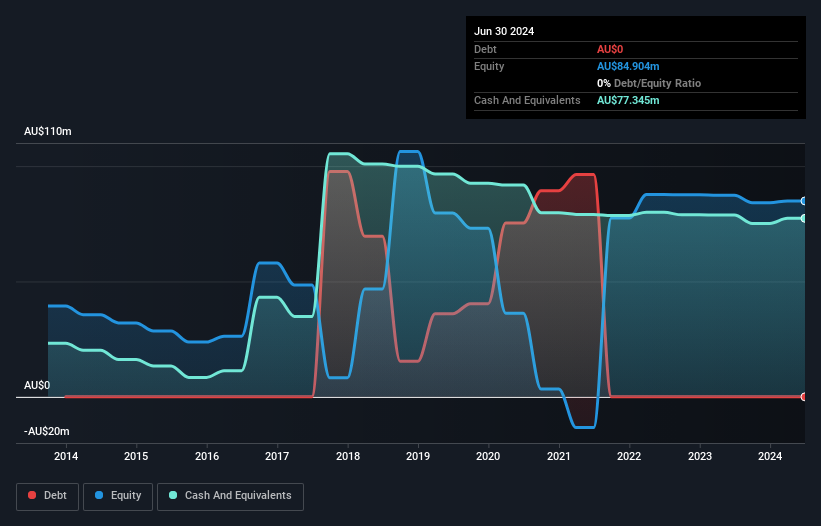

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. In June 2024, Berkeley Energia had AU$77m in cash, and was debt-free. Looking at the last year, the company burnt through AU$1.5m. So it had a very long cash runway of many years from June 2024. Even though this is but one measure of the company's cash burn, the thought of such a long cash runway warms our bellies in a comforting way. You can see how its cash balance has changed over time in the image below.

How Is Berkeley Energia's Cash Burn Changing Over Time?

While Berkeley Energia did record statutory revenue of AU$3.5m over the last year, it didn't have any revenue from operations. To us, that makes it a pre-revenue company, so we'll look to its cash burn trajectory as an assessment of its cash burn situation. The 64% reduction in its cash burn over the last twelve months may be good for protecting the balance sheet but it hardly points to imminent growth. Admittedly, we're a bit cautious of Berkeley Energia due to its lack of significant operating revenues. We prefer most of the stocks on this list of stocks that analysts expect to grow.

Can Berkeley Energia Raise More Cash Easily?

While we're comforted by the recent reduction evident from our analysis of Berkeley Energia's cash burn, it is still worth considering how easily the company could raise more funds, if it wanted to accelerate spending to drive growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of AU$158m, Berkeley Energia's AU$1.5m in cash burn equates to about 0.9% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

Is Berkeley Energia's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Berkeley Energia is burning through its cash. For example, we think its cash runway suggests that the company is on a good path. But it's fair to say that its cash burn reduction was also very reassuring. Taking all the factors in this report into account, we're not at all worried about its cash burn, as the business appears well capitalized to spend as needs be. Taking an in-depth view of risks, we've identified 1 warning sign for Berkeley Energia that you should be aware of before investing.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

Valuation is complex, but we're here to simplify it.

Discover if Berkeley Energia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:BKY

Berkeley Energia

Engages in the exploration and development of mineral properties in Spain.

Flawless balance sheet with minimal risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor