- Australia

- /

- Metals and Mining

- /

- ASX:ERM

Emmerson Resources And 2 Other ASX Penny Stocks To Watch

Reviewed by Simply Wall St

The Australian market has shown resilience, with the ASX200 gaining 0.83% and all sectors making progress, notably the IT sector. For investors interested in exploring smaller or newer companies, penny stocks remain an intriguing option despite their vintage-sounding name. These stocks can offer hidden value and growth potential when backed by strong financial foundations, providing opportunities for those seeking to invest in promising companies at lower price points.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Financial Health Rating |

| Embark Early Education (ASX:EVO) | A$0.755 | A$141.28M | ★★★★☆☆ |

| LaserBond (ASX:LBL) | A$0.595 | A$69.75M | ★★★★★★ |

| Helloworld Travel (ASX:HLO) | A$1.815 | A$287.37M | ★★★★★★ |

| Austin Engineering (ASX:ANG) | A$0.55 | A$322.48M | ★★★★★☆ |

| Navigator Global Investments (ASX:NGI) | A$1.645 | A$798.83M | ★★★★★☆ |

| Perenti (ASX:PRN) | A$1.17 | A$1.07B | ★★★★★★ |

| Atlas Pearls (ASX:ATP) | A$0.14 | A$61M | ★★★★★★ |

| EZZ Life Science Holdings (ASX:EZZ) | A$3.03 | A$141.71M | ★★★★★★ |

| Joyce (ASX:JYC) | A$4.51 | A$129.2M | ★★★★★★ |

| MaxiPARTS (ASX:MXI) | A$1.885 | A$104.27M | ★★★★★★ |

Click here to see the full list of 1,034 stocks from our ASX Penny Stocks screener.

Here's a peek at a few of the choices from the screener.

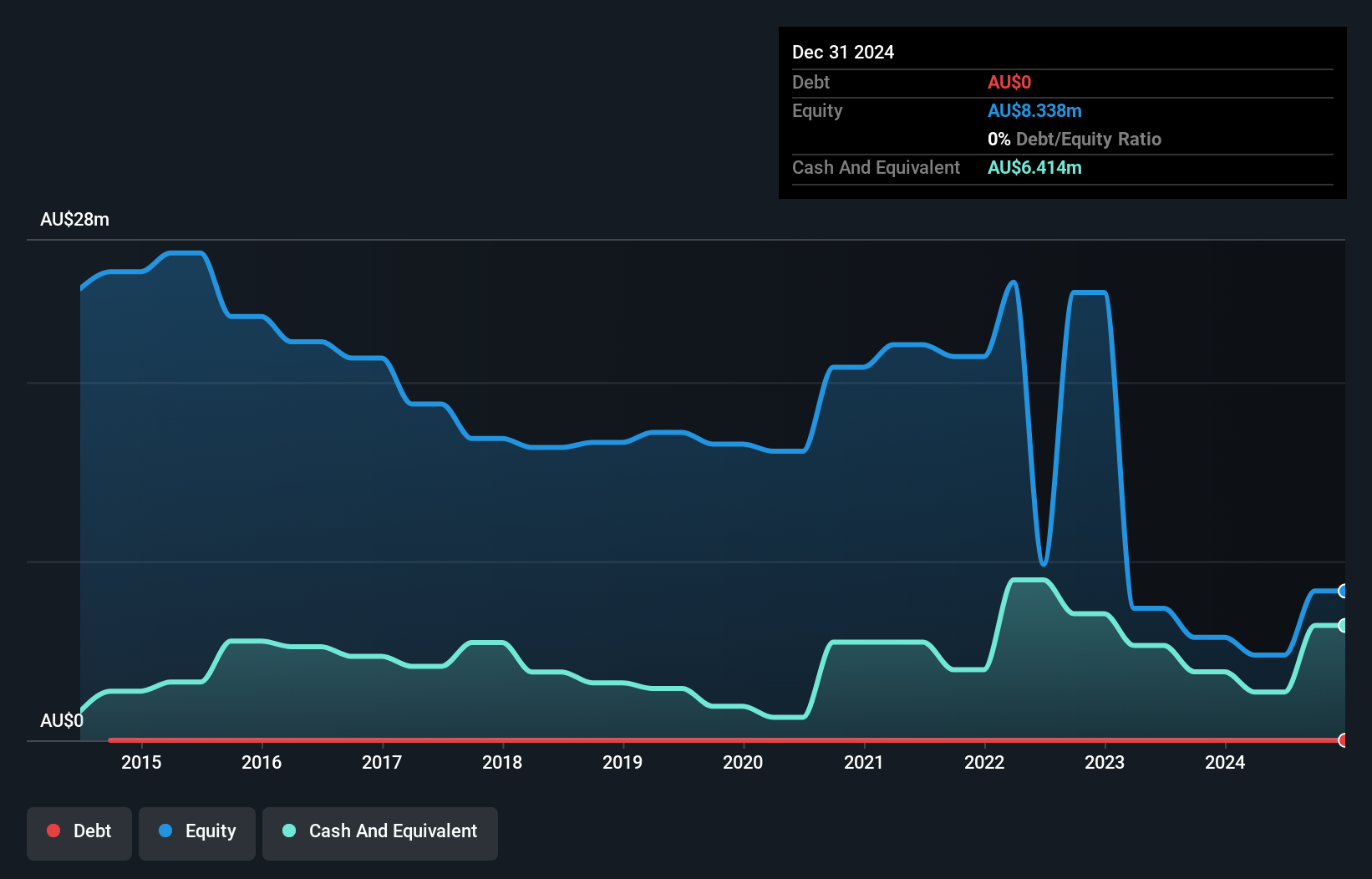

Emmerson Resources (ASX:ERM)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Emmerson Resources Limited is involved in the exploration and evaluation of mineral properties, with a market capitalization of A$25.06 million.

Operations: The company's revenue segment is derived entirely from Mineral Exploration, amounting to A$0.14 million.

Market Cap: A$25.06M

Emmerson Resources, with a market capitalization of A$25.06 million, is pre-revenue, generating only A$0.14 million from mineral exploration. The company remains unprofitable, reporting a net loss of A$2.94 million for the year ended June 30, 2024. Despite this, Emmerson has no debt and maintains sufficient cash runway for more than a year based on current free cash flow levels. Its board and management team are experienced with average tenures of 13.4 and 3 years respectively. Shareholder dilution has been minimal over the past year, while short-term assets exceed liabilities comfortably.

- Jump into the full analysis health report here for a deeper understanding of Emmerson Resources.

- Assess Emmerson Resources' previous results with our detailed historical performance reports.

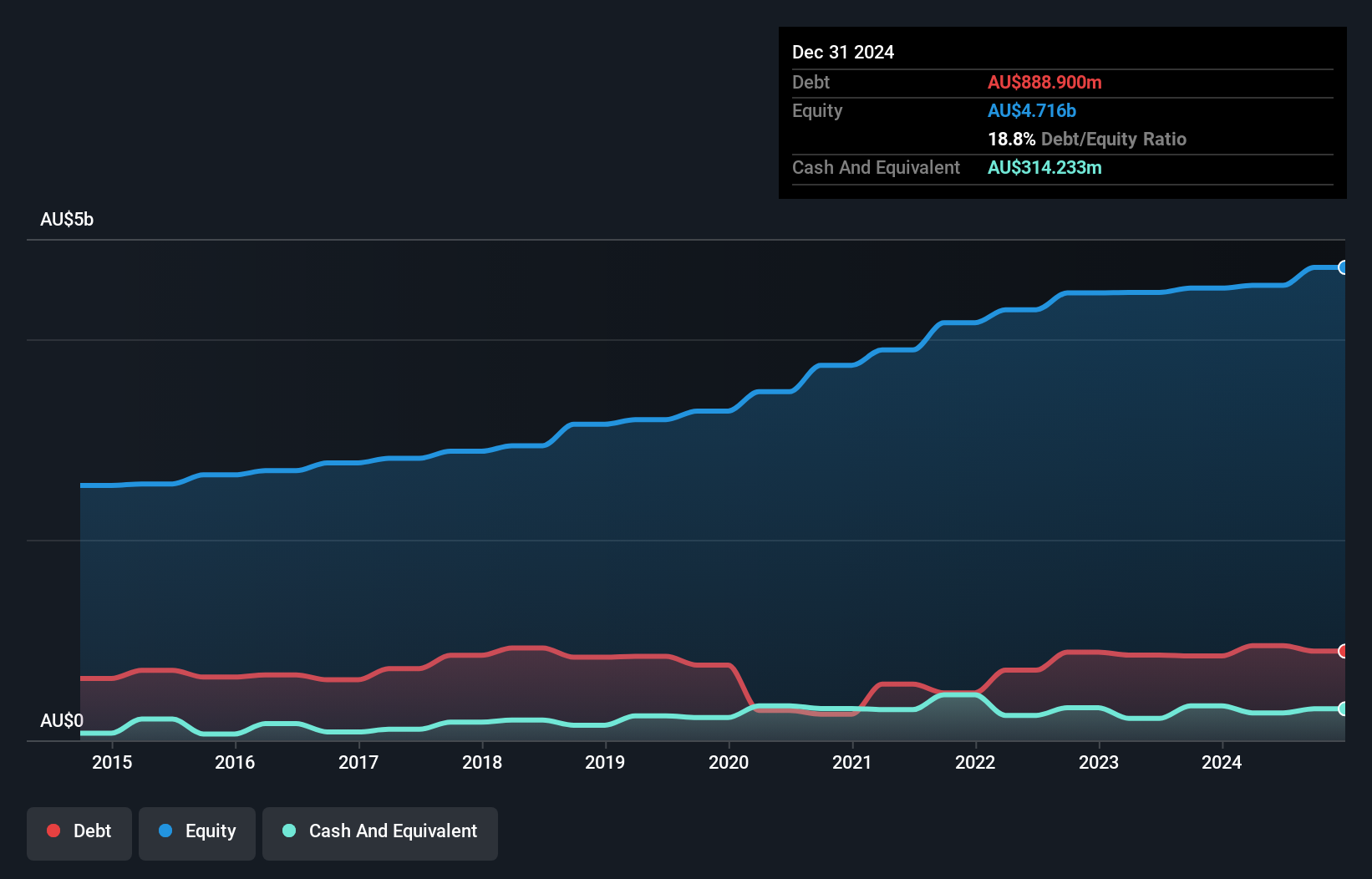

Harvey Norman Holdings (ASX:HVN)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Harvey Norman Holdings Limited operates in the integrated retail, franchise, property, and digital system sectors with a market cap of A$5.67 billion.

Operations: The company's revenue segments include Retail in New Zealand (A$952.69 million), Slovenia & Croatia (A$215.44 million), Singapore & Malaysia (A$707.72 million), Non-Franchised Retail (A$242.39 million), and Ireland & Northern Ireland (A$693.42 million).

Market Cap: A$5.67B

Harvey Norman Holdings, with a market cap of A$5.67 billion, shows mixed financial performance. The company's Return on Equity is low at 7.9%, and it has experienced negative earnings growth over the past year. Despite this, its debt management appears strong with interest payments well-covered by EBIT (11.1x) and a satisfactory net debt to equity ratio of 14.8%. Short-term assets exceed short-term liabilities significantly, though they fall short against long-term liabilities. Recent earnings reports indicate a decline in net income to A$352.45 million from A$539.52 million last year, reflecting challenges in maintaining profit margins and revenue growth stability.

- Get an in-depth perspective on Harvey Norman Holdings' performance by reading our balance sheet health report here.

- Review our growth performance report to gain insights into Harvey Norman Holdings' future.

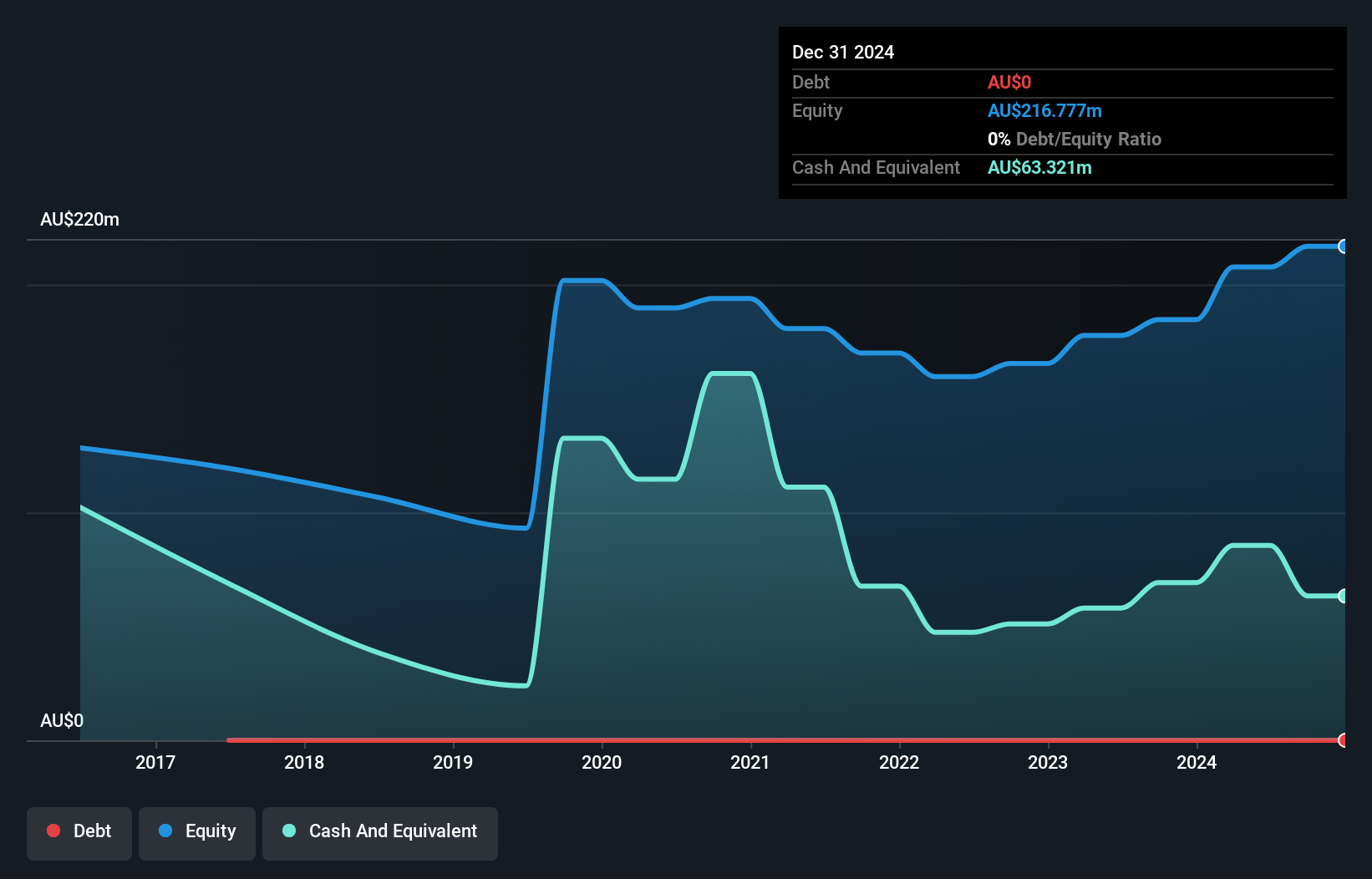

Tyro Payments (ASX:TYR)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Tyro Payments Limited provides payment solutions to merchants in Australia and has a market cap of A$408.42 million.

Operations: The company's revenue is primarily derived from its Payments segment, which generated A$471.51 million, complemented by the Banking segment with A$14.73 million.

Market Cap: A$408.42M

Tyro Payments, with a market cap of A$408.42 million, has shown robust earnings growth of 327.5% over the past year, significantly outpacing the industry average. The company remains debt-free, with short-term assets exceeding both short and long-term liabilities, indicating solid financial health. Despite a large one-off loss impacting recent results, Tyro's net profit margin improved to 5.2%. Its Price-To-Earnings ratio is below the Australian market average, suggesting potential value for investors. Recent developments include board changes and strong annual earnings growth from A$439.78 million to A$497.72 million in revenue and net income rising to A$25.71 million from A$6.01 million last year.

- Click to explore a detailed breakdown of our findings in Tyro Payments' financial health report.

- Understand Tyro Payments' earnings outlook by examining our growth report.

Where To Now?

- Embark on your investment journey to our 1,034 ASX Penny Stocks selection here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Emmerson Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ERM

Emmerson Resources

Engages in the exploration and evaluation of mineral properties.

Excellent balance sheet slight.