Advertisement

Three Top Undervalued Small Caps With Insider Activity In None Region

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have been navigating a complex landscape marked by geopolitical tensions in the Middle East and robust economic indicators in the U.S., which have influenced investor sentiment and impacted various indices, including small-cap stocks. The S&P MidCap 400 and Russell 2000 indices experienced declines as investors weighed these developments alongside strong job growth and rising oil prices. In this environment, identifying promising small-cap stocks involves looking for those with solid fundamentals that may be temporarily undervalued due to broader market volatility, offering potential opportunities for growth as conditions stabilize.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 24.6x | 5.6x | 11.41% | ★★★★★☆ |

| Daiwa House Logistics Trust | 10.0x | 7.3x | 37.57% | ★★★★★☆ |

| Nexus Industrial REIT | 3.6x | 3.6x | 19.34% | ★★★★☆☆ |

| Citizens & Northern | 12.7x | 2.8x | 44.35% | ★★★★☆☆ |

| Sagicor Financial | 1.3x | 0.3x | -43.71% | ★★★★☆☆ |

| Franklin Financial Services | 9.8x | 1.9x | 38.58% | ★★★★☆☆ |

| Calfrac Well Services | 2.5x | 0.2x | 18.37% | ★★★★☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -774.50% | ★★★☆☆☆ |

| National Vision Holdings | NA | 0.4x | -33.48% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

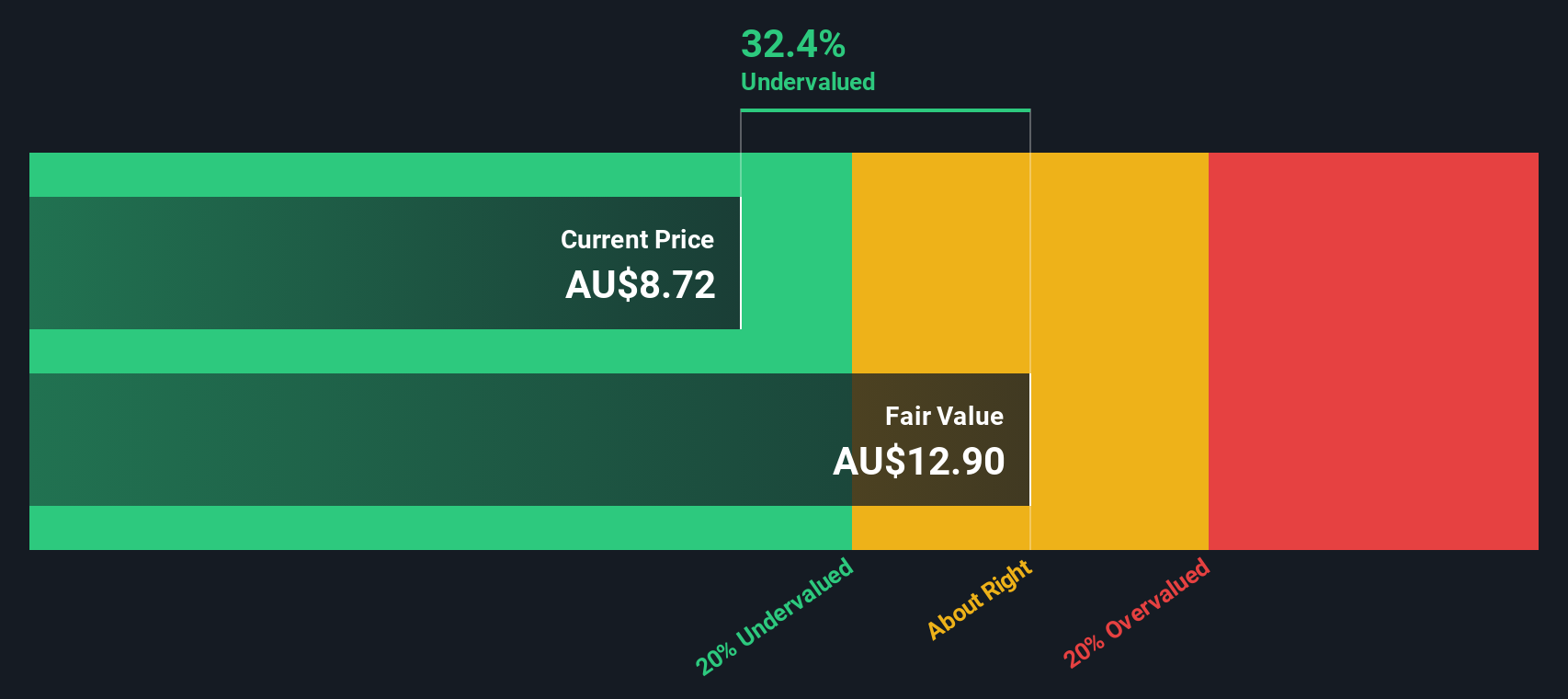

Magellan Financial Group (ASX:MFG)

Simply Wall St Value Rating: ★★★★★☆

Overview: Magellan Financial Group is an Australian-based investment management company that specializes in global equities and infrastructure strategies, with a market capitalization of A$3.95 billion.

Operations: Magellan Financial Group generates revenue primarily through its Investment Management Services, contributing significantly to its overall income. The company's cost of goods sold (COGS) impacts its gross profit, with a recent gross profit margin of 80.78%. Operating expenses include general and administrative costs, depreciation and amortization, and sales and marketing expenses. Notably, the net income margin has shown variation over time, reaching 63.07% in one period.

PE: 7.8x

Magellan Financial Group, a small company, has shown insider confidence with share purchases from July 2023 to June 2024, repurchasing 685,571 shares for A$5.19 million. Despite its high-quality earnings and recent dividend increase to A$0.357 per share for the six months ending June 2024, the firm faces challenges with forecasted earnings declines of 9.2% annually over three years and reliance on external borrowing as funding. However, their net income rose to A$238.76 million from A$182.66 million last year, indicating potential resilience amidst market pressures.

- Navigate through the intricacies of Magellan Financial Group with our comprehensive valuation report here.

Learn about Magellan Financial Group's historical performance.

Gujarat Ambuja Exports (NSEI:GAEL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Gujarat Ambuja Exports operates in agro-processing, spinning, renewable power, and maize processing sectors with a market capitalization of ₹67.10 billion.

Operations: The company's primary revenue stream is from its Maize Processing Division, contributing significantly to its total revenue. The gross profit margin has shown fluctuations, peaking at 30.85% in March 2022 before declining to 27.68% by June 2024. Operating expenses have consistently been a notable component of the cost structure, with general and administrative expenses being a consistent part of it over time.

PE: 18.3x

Gujarat Ambuja Exports, a smaller company in its sector, has shown insider confidence with Sandeep Agrawal purchasing 3,050 shares for ₹389,235 between July and August 2024. The company's earnings are expected to grow by 15.93% annually. Despite relying solely on external borrowing for funding, which carries higher risk, the firm declared a final dividend of ₹0.35 per share for fiscal year 2023-24 at its AGM on August 31st.

- Take a closer look at Gujarat Ambuja Exports' potential here in our valuation report.

Understand Gujarat Ambuja Exports' track record by examining our Past report.

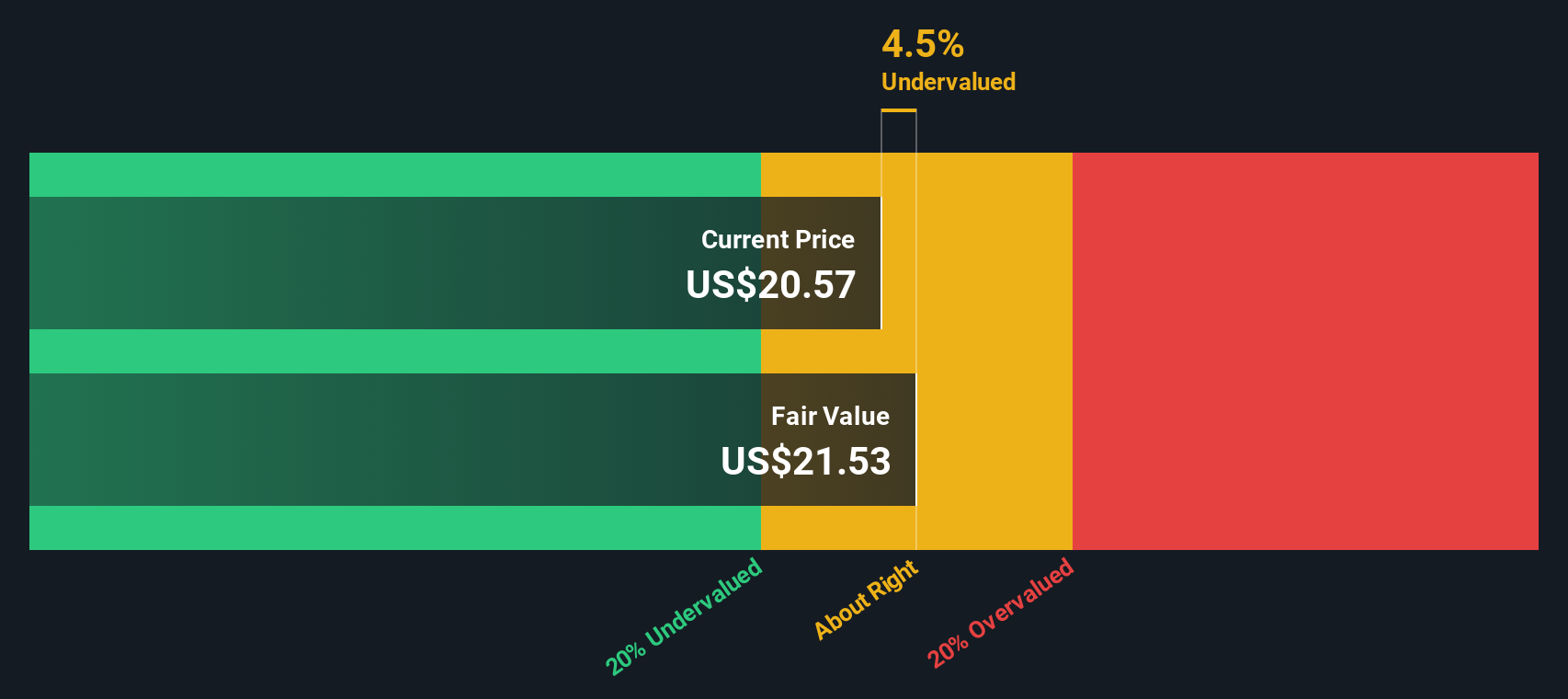

Victoria's Secret (NYSE:VSCO)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Victoria's Secret is a leading specialty retailer primarily focused on women's intimate apparel, beauty products, and lingerie, with operations centered around its retail segment valued at $6.13 billion.

Operations: Victoria's Secret generates revenue primarily from its retail specialty segment, with recent figures around $6.13 billion. The company's cost of goods sold (COGS) significantly impacts its gross profit margin, which was 44.67% as of the latest period. Operating expenses, including general and administrative costs and sales & marketing expenses, are substantial components affecting profitability.

PE: 14.3x

Victoria's Secret, a smaller company in the market, has shown signs of financial improvement with second-quarter net income reaching US$31.8 million, reversing a previous loss. The company raised its full-year sales guidance for 2024 despite expecting a slight decline compared to last year. Recent leadership changes include appointing Hillary Super as CEO, bringing extensive retail experience from her tenure at Savage X Fenty and Anthropologie Group. However, the company's reliance on external borrowing poses higher financial risks without insider confidence through share purchases or repurchases observed recently.

Where To Now?

- Explore the 188 names from our Undervalued Small Caps With Insider Buying screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:GAEL

Gujarat Ambuja Exports

Primarily engages in the agro processing activities in India and internationally.

Excellent balance sheet unattractive dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

87 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

925 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative