- Australia

- /

- Capital Markets

- /

- ASX:MFG

Undervalued Small Caps In Australia With Insider Buying To Consider

Reviewed by Simply Wall St

Over the last 7 days, the Australian market has remained flat, yet it has shown a robust performance over the past 12 months with a rise of 22%, and earnings are anticipated to grow by 12% per annum in the coming years. In this environment, identifying small-cap stocks that may be undervalued and have insider buying can present intriguing opportunities for investors looking to capitalize on potential growth.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| GWA Group | 16.4x | 1.5x | 41.77% | ★★★★★★ |

| SHAPE Australia | 13.7x | 0.3x | 36.34% | ★★★★★☆ |

| Aurelia Metals | NA | 1.1x | 46.86% | ★★★★★☆ |

| Tabcorp Holdings | NA | 0.4x | 20.63% | ★★★★★☆ |

| Collins Foods | 17.9x | 0.7x | 7.75% | ★★★★☆☆ |

| Centuria Capital Group | 21.7x | 4.9x | 44.62% | ★★★★☆☆ |

| Dicker Data | 20.1x | 0.7x | -65.97% | ★★★☆☆☆ |

| Coventry Group | 238.0x | 0.4x | -17.72% | ★★★☆☆☆ |

| Corporate Travel Management | 20.1x | 2.4x | 4.72% | ★★★☆☆☆ |

| Abacus Storage King | 12.1x | 7.6x | -29.19% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

Mader Group (ASX:MAD)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Mader Group is a company that specializes in staffing and outsourcing services, with a market capitalization of A$1.38 billion.

Operations: Mader Group generates revenue primarily from staffing and outsourcing services, with their latest reported revenue at A$774.47 million. The company's cost of goods sold (COGS) amounts to A$612.49 million, resulting in a gross profit of A$161.99 million and a gross profit margin of 20.92%. Operating expenses are recorded at A$89.97 million, contributing to a net income of A$50.42 million and a net income margin of 6.51%.

PE: 24.1x

Mader Group, a growing player in Australia, is attracting attention for its potential value. With earnings projected to grow 13% annually and revenue expected to hit A$870 million in fiscal 2025, the company shows promise despite relying solely on external borrowing. Insider confidence is evident with share purchases this year. Recently added to the S&P Global BMI Index in September 2024, Mader's financial health includes a net income rise from A$38.51 million to A$50.42 million over the past year.

- Click here and access our complete valuation analysis report to understand the dynamics of Mader Group.

Examine Mader Group's past performance report to understand how it has performed in the past.

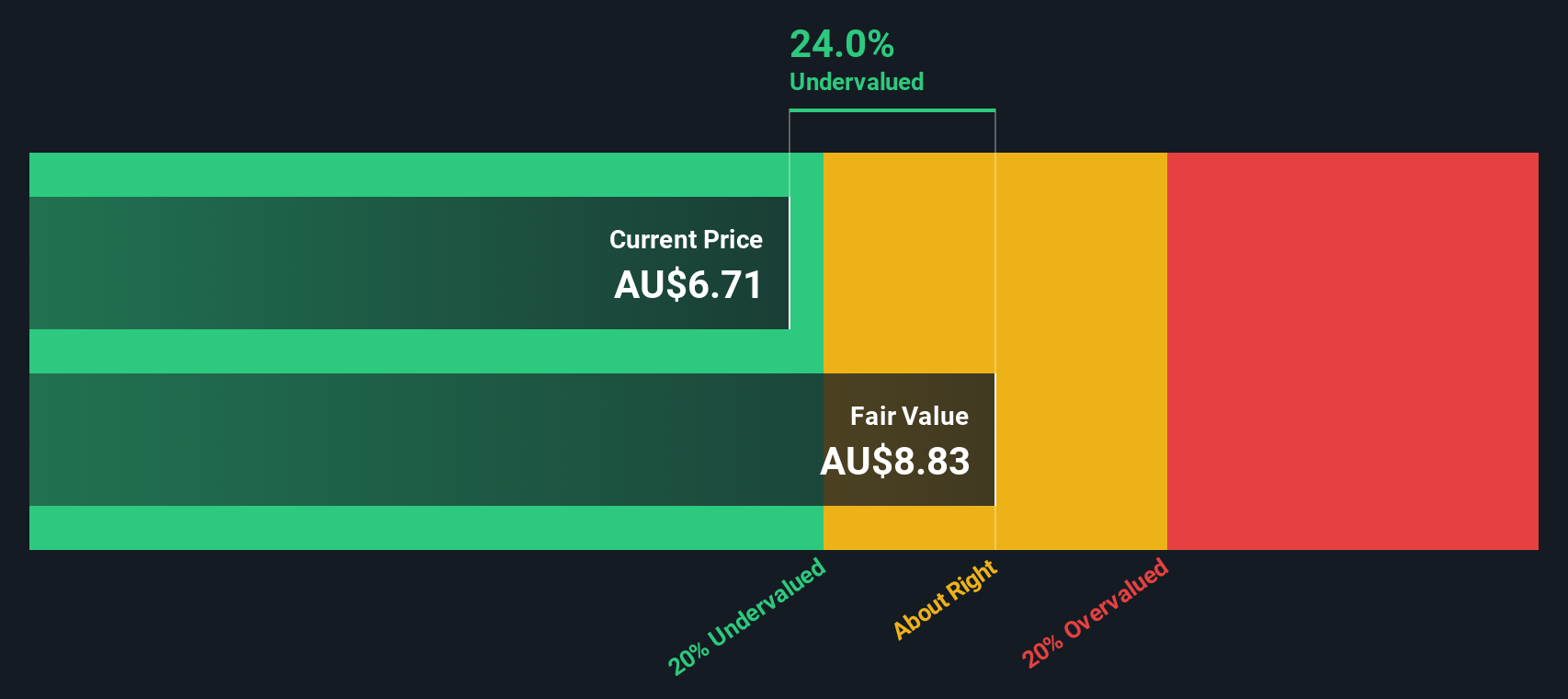

Magellan Financial Group (ASX:MFG)

Simply Wall St Value Rating: ★★★★★☆

Overview: Magellan Financial Group is an Australian-based investment management firm that specializes in global equities and infrastructure strategies, with a market capitalization of approximately A$3.42 billion.

Operations: Magellan Financial Group generates revenue primarily from Investment Management Services, contributing A$279.83 million, with additional income from Fund Investments and Corporate activities. Over recent periods, the company has experienced fluctuations in its gross profit margin, reaching 80.78% in the latest quarter ending October 2024. Operating expenses are a significant part of its cost structure, including general and administrative expenses which were A$29.15 million recently.

PE: 8.4x

Magellan Financial Group, a smaller Australian firm, showcases high-quality earnings despite relying solely on external borrowing for funding. Recent financials reveal net income rising to A$238.76 million from A$182.66 million year-on-year, even as revenue dipped to A$378.63 million from A$431.65 million. The company repurchased 4,969,671 shares for A$52.47 million by June 2024 under its buyback plan extended till April 2025, reflecting strategic capital management amidst forecasted earnings declines over the next three years by an average of 9.2% annually.

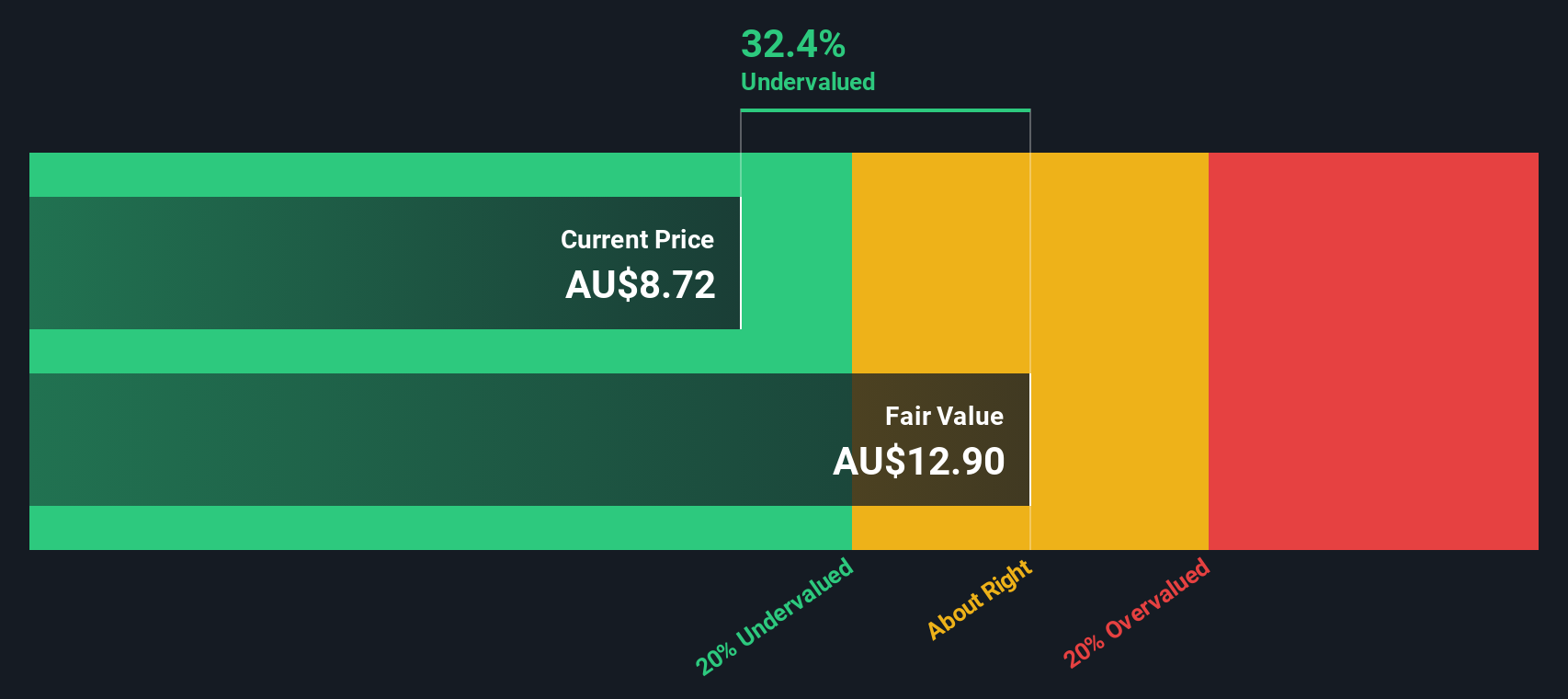

Tabcorp Holdings (ASX:TAH)

Simply Wall St Value Rating: ★★★★★☆

Overview: Tabcorp Holdings operates in the gaming services and wagering and media sectors, with a market capitalization of A$4.90 billion.

Operations: Tabcorp Holdings generates revenue primarily from its Wagering and Media segment, contributing significantly to the total revenue of A$2.36 billion as of the latest period. The company has experienced a consistent gross profit margin of 100% over several periods, indicating that all reported revenues translate directly into gross profit. Despite this high gross profit margin, net income margins have shown volatility with recent figures reflecting substantial losses due to high operating and non-operating expenses.

PE: -0.8x

Tabcorp Holdings, a small player in Australia's investment landscape, recently reported a challenging financial year with sales of A$2.3 billion, down from A$2.4 billion the previous year, and a net loss of A$1.36 billion compared to last year's profit. Despite this setback, insider confidence is evident as an executive purchased 250,000 shares for approximately A$215,000 in September 2024. While facing high-risk external borrowing and past shareholder dilution, earnings are projected to grow significantly by 112% annually.

- Take a closer look at Tabcorp Holdings' potential here in our valuation report.

Evaluate Tabcorp Holdings' historical performance by accessing our past performance report.

Key Takeaways

- Unlock more gems! Our Undervalued ASX Small Caps With Insider Buying screener has unearthed 19 more companies for you to explore.Click here to unveil our expertly curated list of 22 Undervalued ASX Small Caps With Insider Buying.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:MFG

Flawless balance sheet and undervalued.