David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Retech Technology Co., Limited (ASX:RTE) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Retech Technology

How Much Debt Does Retech Technology Carry?

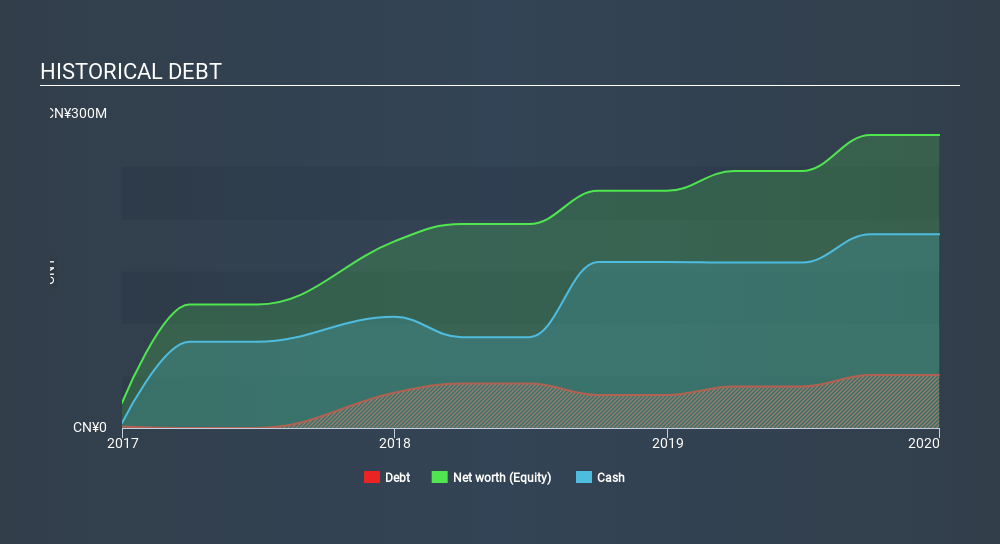

You can click the graphic below for the historical numbers, but it shows that as of December 2019 Retech Technology had CN¥50.7m of debt, an increase on CN¥31.5m, over one year. But on the other hand it also has CN¥185.1m in cash, leading to a CN¥134.4m net cash position.

How Strong Is Retech Technology's Balance Sheet?

We can see from the most recent balance sheet that Retech Technology had liabilities of CN¥85.2m falling due within a year, and liabilities of CN¥72.3m due beyond that. Offsetting these obligations, it had cash of CN¥185.1m as well as receivables valued at CN¥114.0m due within 12 months. So it can boast CN¥141.6m more liquid assets than total liabilities.

This surplus strongly suggests that Retech Technology has a rock-solid balance sheet (and the debt is of no concern whatsoever). On this basis we think its balance sheet is strong like a sleek panther or even a proud lion. Simply put, the fact that Retech Technology has more cash than debt is arguably a good indication that it can manage its debt safely.

And we also note warmly that Retech Technology grew its EBIT by 19% last year, making its debt load easier to handle. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Retech Technology will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Retech Technology may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Retech Technology recorded free cash flow worth 57% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Retech Technology has net cash of CN¥134.4m, as well as more liquid assets than liabilities. And we liked the look of last year's 19% year-on-year EBIT growth. So we don't think Retech Technology's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Retech Technology you should be aware of, and 1 of them makes us a bit uncomfortable.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ASX:RTE

Retech Technology

Retech Technology Co., Limited, an investment holding company, provides technology solutions to corporate customers, vocational schools, ESG related companies, and students in the People’s Republic of China, Hong Kong, and Australia.

Mediocre balance sheet with poor track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion