Advertisement

- Australia

- /

- Hospitality

- /

- ASX:FLT

We Think The Compensation For Flight Centre Travel Group Limited's (ASX:FLT) CEO Looks About Right

Key Insights

- Flight Centre Travel Group will host its Annual General Meeting on 12th of November

- Total pay for CEO Skroo Turner includes AU$1.01m salary

- The total compensation is 46% less than the average for the industry

- Over the past three years, Flight Centre Travel Group's EPS grew by 95% and over the past three years, the total loss to shareholders 22%

The performance at Flight Centre Travel Group Limited (ASX:FLT) has been rather lacklustre of late and shareholders may be wondering what CEO Skroo Turner is planning to do about this. At the next AGM coming up on 12th of November, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We think CEO compensation looks appropriate given the data we have put together.

View our latest analysis for Flight Centre Travel Group

How Does Total Compensation For Skroo Turner Compare With Other Companies In The Industry?

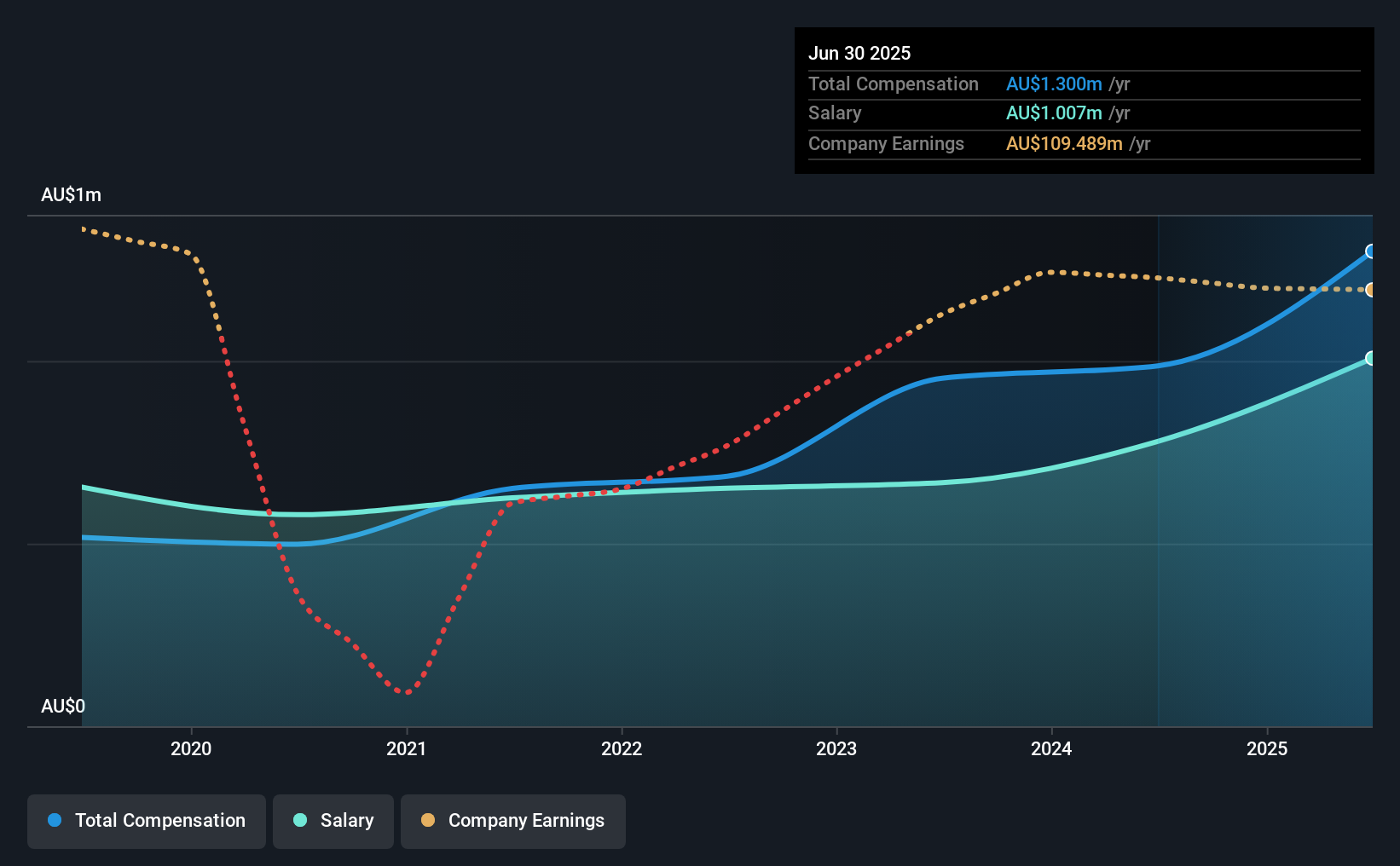

Our data indicates that Flight Centre Travel Group Limited has a market capitalization of AU$2.6b, and total annual CEO compensation was reported as AU$1.3m for the year to June 2025. That's a notable increase of 32% on last year. We note that the salary portion, which stands at AU$1.01m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Australian Hospitality industry with market capitalizations ranging from AU$1.5b to AU$4.9b, the reported median CEO total compensation was AU$2.4m. In other words, Flight Centre Travel Group pays its CEO lower than the industry median. Moreover, Skroo Turner also holds AU$599k worth of Flight Centre Travel Group stock directly under their own name.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | AU$1.0m | AU$780k | 77% |

| Other | AU$293k | AU$207k | 23% |

| Total Compensation | AU$1.3m | AU$987k | 100% |

On an industry level, roughly 57% of total compensation represents salary and 43% is other remuneration. Flight Centre Travel Group is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Flight Centre Travel Group Limited's Growth Numbers

Flight Centre Travel Group Limited has seen its earnings per share (EPS) increase by 95% a year over the past three years. It achieved revenue growth of 2.7% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Flight Centre Travel Group Limited Been A Good Investment?

Given the total shareholder loss of 22% over three years, many shareholders in Flight Centre Travel Group Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The fact that shareholders are sitting on a loss is certainly disheartening. This diverges with the robust growth in EPS, suggesting that there is a large discrepancy between share price and fundamentals. There needs to be more focus by management and the board to examine why the share price has diverged from fundamentals. In the upcoming AGM, shareholders should take this opportunity to raise these concerns with the board and revisit their investment thesis with regards to the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Flight Centre Travel Group that you should be aware of before investing.

Switching gears from Flight Centre Travel Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor