Stock Analysis

- Australia

- /

- Hospitality

- /

- ASX:FLT

Unveiling Three ASX Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

The Australian stock market is currently experiencing a downturn, with the ASX200 down by 0.45% and most sectors showing declines. Notably, IT and healthcare sectors have faced significant losses, while real estate has shown some resilience amidst recent economic turbulence highlighted by a surprising inflation report. In such a market context, companies with high insider ownership can be particularly compelling as they often indicate that those closest to the business are confident in its long-term potential and are deeply invested in its success.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Botanix Pharmaceuticals (ASX:BOT) | 10% | 120.9% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Change Financial (ASX:CCA) | 26.6% | 76.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Biome Australia (ASX:BIO) | 34.5% | 114.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 52.2% |

| Argosy Minerals (ASX:AGY) | 14.5% | 129.6% |

Underneath we present a selection of stocks filtered out by our screen.

Botanix Pharmaceuticals (ASX:BOT)

Simply Wall St Growth Rating: ★★★★★★

Overview: Botanix Pharmaceuticals Limited, based in Australia, focuses on the research and development of dermatology and antimicrobial products with a market capitalization of approximately A$624.46 million.

Operations: The company generates revenue primarily through its research and development activities in dermatology and antimicrobial products, totaling A$0.44 million.

Insider Ownership: 10%

Return On Equity Forecast: 44% (2026 estimate)

Botanix Pharmaceuticals, despite its small revenue base of A$437K, is poised for significant growth with expected annual profit and revenue increases substantially above the Australian market average. The company's earnings have expanded by 12.5% annually over the past five years and are projected to surge by 120.89% per year moving forward. Recently, Botanix completed a follow-on equity offering raising A$70 million, which may dilute current shareholders but also funds expansion as it approaches new product launches.

- Click to explore a detailed breakdown of our findings in Botanix Pharmaceuticals' earnings growth report.

- In light of our recent valuation report, it seems possible that Botanix Pharmaceuticals is trading beyond its estimated value.

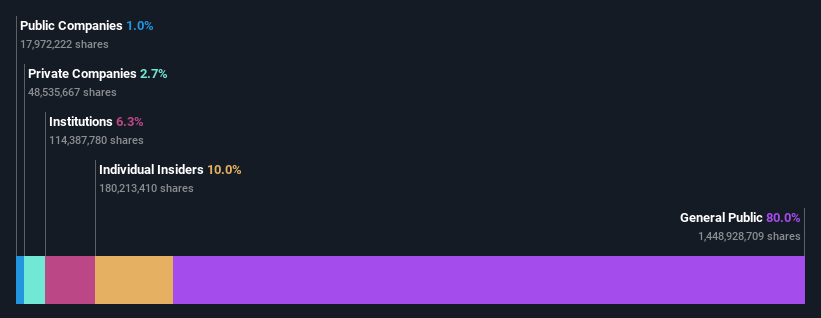

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across various regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of A$4.44 billion.

Operations: The company generates revenue primarily through its leisure and corporate travel segments, with A$1.28 billion from leisure and A$1.06 billion from corporate services.

Insider Ownership: 13.3%

Return On Equity Forecast: 22% (2026 estimate)

Flight Centre Travel Group, now profitable, trades at 18.5% below its estimated fair value, highlighting potential undervaluation. With insider ownership aligning interests with shareholders, the company's earnings are set to outpace the Australian market with an 18.8% annual growth rate. Although revenue growth is more modest at 9.7% annually, it still exceeds the national average of 5.4%. The forecasted high Return on Equity of 21.8% in three years underscores strong management efficacy and financial health.

- Unlock comprehensive insights into our analysis of Flight Centre Travel Group stock in this growth report.

- The valuation report we've compiled suggests that Flight Centre Travel Group's current price could be inflated.

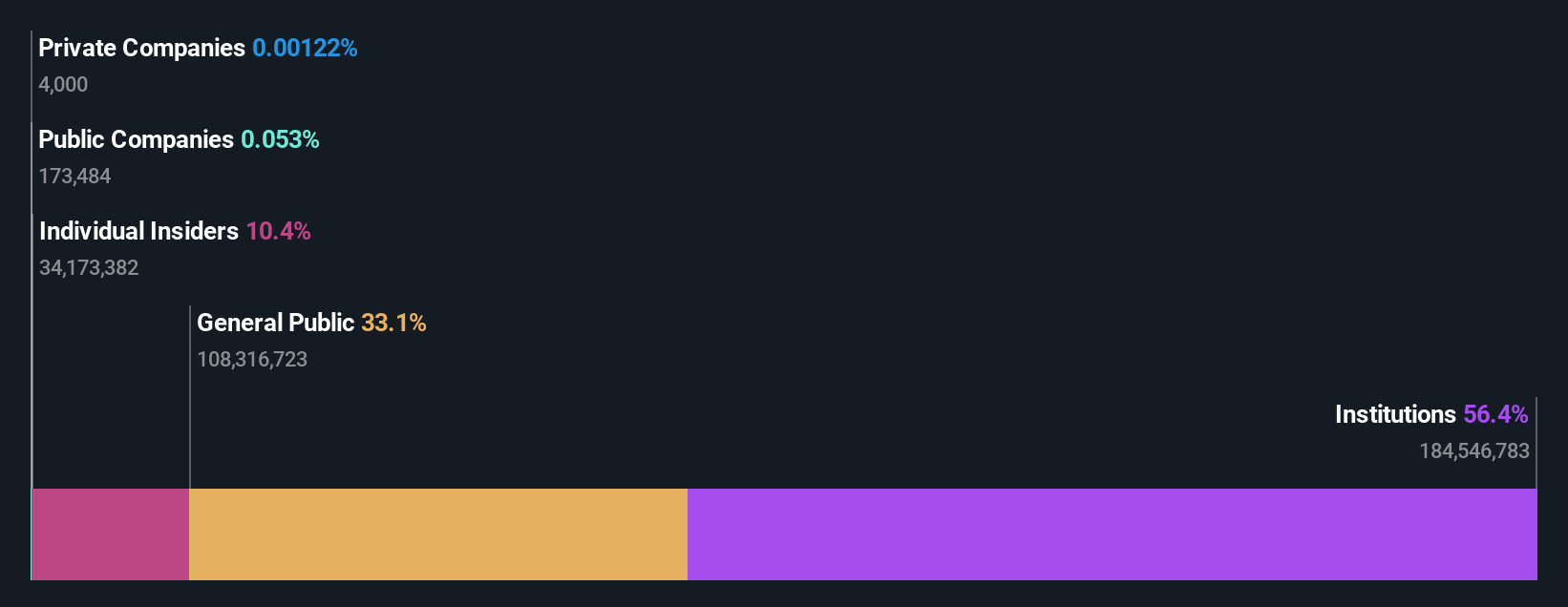

Technology One (ASX:TNE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Technology One Limited is a company that develops, markets, sells, implements, and supports integrated enterprise business software solutions both in Australia and internationally, with a market capitalization of A$6.06 billion.

Operations: The company generates revenue through three primary segments: software sales contributing A$317.24 million, corporate services at A$83.83 million, and consulting services totaling A$68.13 million.

Insider Ownership: 12.3%

Return On Equity Forecast: 33% (2027 estimate)

Technology One, a growth-oriented firm with high insider ownership, exhibits promising financial health with earnings expected to grow by 14.3% annually, outpacing the Australian market average of 13.8%. While its revenue growth at 11.1% yearly is below the significant threshold of 20%, it still surpasses the national market's 5.4%. The company's price-to-earnings ratio stands at an attractive A$55.3x compared to the industry average of A$61.6x, suggesting potential undervaluation relative to its peers. Recent results show a robust year-on-year revenue increase from A$201 million to A$240.83 million and a net income rise from A$41.28 million to A$48 million, reflecting strong operational performance and profitability.

- Get an in-depth perspective on Technology One's performance by reading our analyst estimates report here.

- The analysis detailed in our Technology One valuation report hints at an inflated share price compared to its estimated value.

Next Steps

- Discover the full array of 89 Fast Growing ASX Companies With High Insider Ownership right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Flight Centre Travel Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Excellent balance sheet with reasonable growth potential.