Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Experience Co Limited (ASX:EXP) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Experience Co

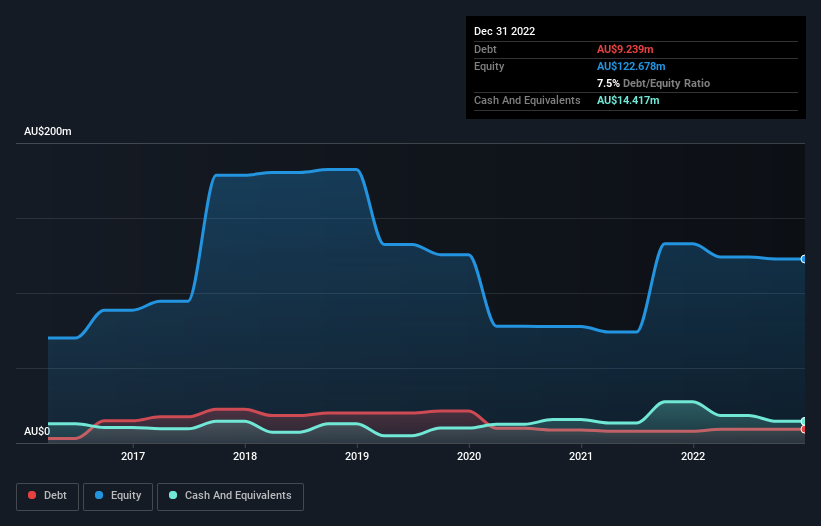

What Is Experience Co's Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2022 Experience Co had AU$9.24m of debt, an increase on AU$7.84m, over one year. However, it does have AU$14.4m in cash offsetting this, leading to net cash of AU$5.18m.

How Healthy Is Experience Co's Balance Sheet?

The latest balance sheet data shows that Experience Co had liabilities of AU$34.4m due within a year, and liabilities of AU$30.1m falling due after that. On the other hand, it had cash of AU$14.4m and AU$4.00m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by AU$46.1m.

Experience Co has a market capitalization of AU$196.0m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Experience Co boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Experience Co can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Experience Co wasn't profitable at an EBIT level, but managed to grow its revenue by 102%, to AU$88m. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Experience Co?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Experience Co lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of AU$5.4m and booked a AU$11m accounting loss. With only AU$5.18m on the balance sheet, it would appear that its going to need to raise capital again soon. Importantly, Experience Co's revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Experience Co insider transactions.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Experience Co might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:EXP

Experience Co

Engages in the adventure tourism and leisure business in Australia and New Zealand.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor