Advertisement

- Australia

- /

- Professional Services

- /

- ASX:QIP

Why It Might Not Make Sense To Buy QANTM Intellectual Property Limited (ASX:QIP) For Its Upcoming Dividend

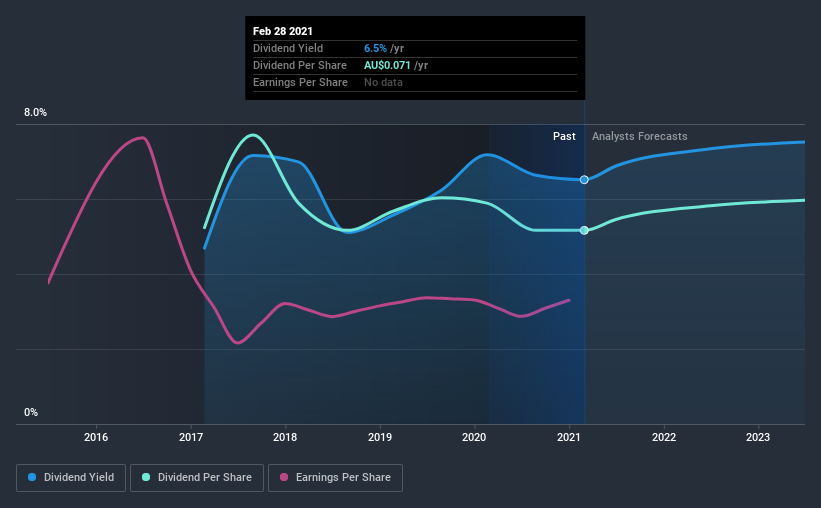

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see QANTM Intellectual Property Limited (ASX:QIP) is about to trade ex-dividend in the next 2 days. Investors can purchase shares before the 3rd of March in order to be eligible for this dividend, which will be paid on the 31st of March.

QANTM Intellectual Property's next dividend payment will be AU$0.04 per share. Last year, in total, the company distributed AU$0.071 to shareholders. Based on the last year's worth of payments, QANTM Intellectual Property has a trailing yield of 6.5% on the current stock price of A$1.09. If you buy this business for its dividend, you should have an idea of whether QANTM Intellectual Property's dividend is reliable and sustainable. So we need to investigate whether QANTM Intellectual Property can afford its dividend, and if the dividend could grow.

View our latest analysis for QANTM Intellectual Property

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Its dividend payout ratio is 86% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be worried about the risk of a drop in earnings. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out more than half (65%) of its free cash flow in the past year, which is within an average range for most companies.

It's positive to see that QANTM Intellectual Property's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit QANTM Intellectual Property paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. That's why it's not ideal to see QANTM Intellectual Property's earnings per share have been shrinking at 2.6% a year over the previous five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. It looks like the QANTM Intellectual Property dividends are largely the same as they were four years ago. If a company's dividend stays flat while earnings are in decline, this is typically a sign that it is paying out a larger percentage of its earnings. This can become unsustainable if earnings fall far enough.

Final Takeaway

Should investors buy QANTM Intellectual Property for the upcoming dividend? It's never good to see earnings per share shrinking, but at least the dividend payout ratios appear reasonable. We're aware though that if earnings continue to decline, the dividend could be at risk. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Although, if you're still interested in QANTM Intellectual Property and want to know more, you'll find it very useful to know what risks this stock faces. Every company has risks, and we've spotted 1 warning sign for QANTM Intellectual Property you should know about.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade QANTM Intellectual Property, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if QANTM Intellectual Property might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:QIP

QANTM Intellectual Property

Provides intellectual property services for start-up technology businesses, SMEs, multinationals, public sector research institutions, and universities in Australia, New Zealand, the United Kingdom, Singapore, Malaysia, and Hongkong.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor