Computershare (ASX:CPU) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a notable 31.2% increase in dividend payouts and innovative product launches, juxtaposed against a 16.7% drop in Q2 net sales and inflationary pressures. In the discussion that follows, we will delve into Computershare's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

Strengths: Core Advantages Driving Sustained Success For Computershare

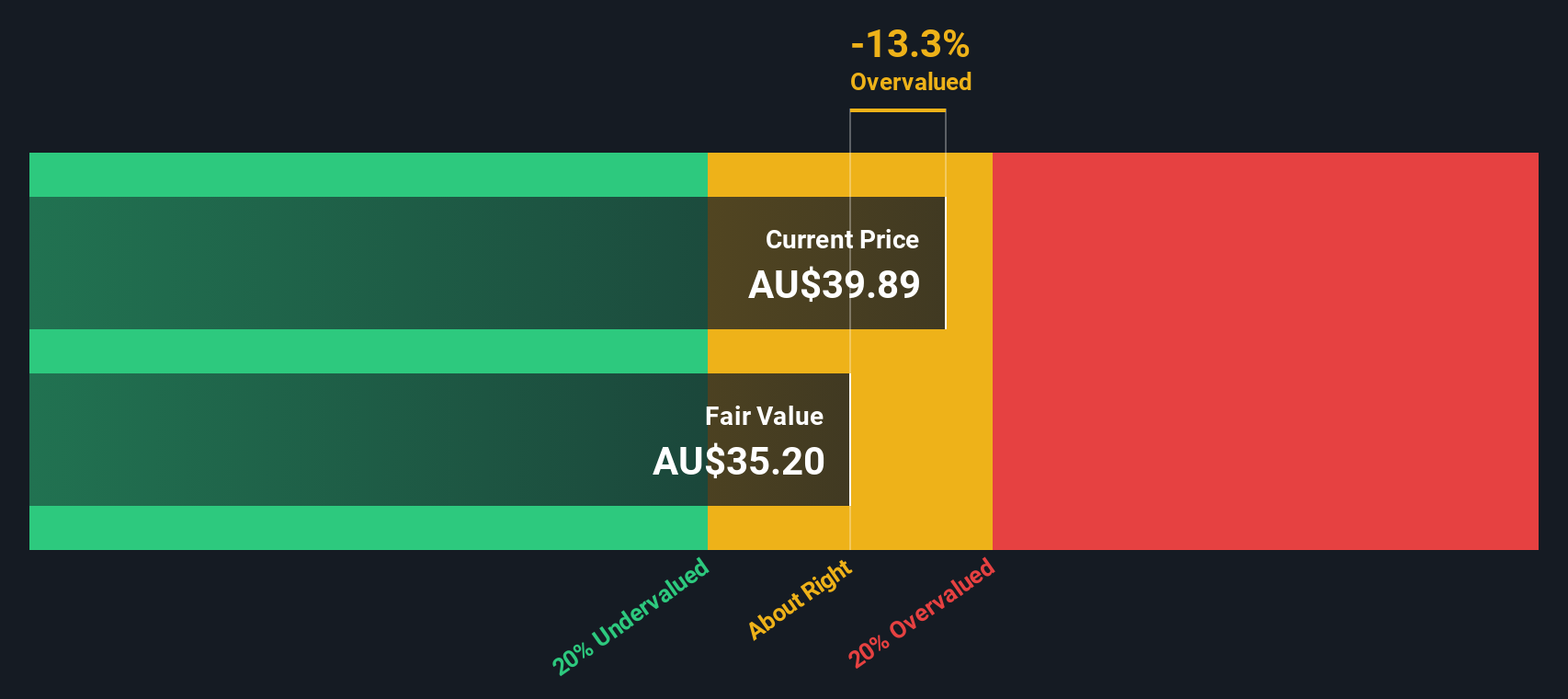

Computershare has demonstrated strong financial health, with management EPS increasing by over 8%, slightly ahead of guidance, and EBIT ex MI up by 21%, as highlighted by CEO Stuart Irving. The company also reported a robust return on invested capital (ROIC) at 30%. Issuer Services revenues rose by 11%, and Corporate Actions revenues surged by over 23%, reflecting the company's effective integrated model. Transaction fees increased by over 35% due to strong vesting activity across a diverse client book. Additionally, the company has significantly strengthened its balance sheet, with net debt-to-EBITDA leverage at 0.36x and net debt more than halved. The company is considered good value with a Price-To-Earnings Ratio of 20.7x, which is below both the industry average of 21.2x and the peer average of 38.7x, indicating it is trading at a significant discount to its estimated fair value of A$52.48.

Weaknesses: Critical Issues Affecting Computershare's Performance and Areas For Growth

Despite its strengths, Computershare faces several challenges. Corporate Trust headline revenues modestly declined, and the exit from the Ginnie Mae REMIC business resulted in a loss of approximately $28 million in annual trust fee revenues. Market conditions have been challenging, with higher interest rates impacting new deal volumes and mix. Statutory NPAT decreased by 21% to $352.6 million, as reported by CFO Nick Oldfield. Additionally, the sale of KCC cost the company $0.013 per share in earnings. The company's revenue growth forecast of 1.1% per year is significantly slower than the Australian market's 5.4% per year, indicating potential areas for improvement.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Computershare is actively investing in its core businesses and making selective and disciplined acquisitions to strengthen its market position. CEO Stuart Irving mentioned multiple technology projects running across the group, which could drive future growth. The recovery in structured product securitization is expected to improve trust fees, client balances, and yields. The company is also focusing on cost-out programs to reduce stranded costs from recent disposals. With an active pipeline for potential acquisitions, Computershare is well-positioned to capitalize on emerging opportunities and enhance its competitive advantage. The company's earnings are forecast to grow at 8.39% per year, which, while slower than the market average, still represents a positive growth trajectory.

Threats: Key Risks and Challenges That Could Impact Computershare's Success

Computershare faces several external threats that could impact its success. Global market volatility elevates forecasting risk, and new clients from IPOs are at all-time lows, potentially affecting future revenue streams. The average cost of debt is almost 7%, which could strain financial resources. The Corporate Trust clients tend to be more sophisticated and challenging regarding the rates they demand, adding to the complexity of maintaining profitability in this segment. Additionally, significant insider selling over the past three months raises concerns about internal confidence in the company's future performance. The company's unstable dividend track record and high level of debt further add to the risks that Computershare must navigate to sustain its growth and market position.

Conclusion

Computershare's strong financial health, evidenced by a 21% increase in EBIT ex MI and a 30% return on invested capital, highlights its effective integrated model and prudent financial management. However, challenges such as declining Corporate Trust revenues and a slower revenue growth forecast compared to the Australian market indicate areas needing strategic focus. The company's active investment in technology projects and disciplined acquisitions positions it well for future growth, despite external threats like market volatility and high debt costs. With a Price-To-Earnings Ratio of 20.7x, significantly below the industry and peer averages, Computershare is trading at a notable discount to its estimated fair value of A$52.48, suggesting potential upside for investors as it navigates these complexities.

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ASX:CPU

Computershare

Provides issuer, corporate trust, employee share plans and voucher, communication and utilities, technology and operations, and mortgage and property rental services.