Advertisement

- Australia

- /

- Electrical

- /

- ASX:FOS

FOS Capital Limited's (ASX:FOS) 26% Price Boost Is Out Of Tune With Earnings

Despite an already strong run, FOS Capital Limited (ASX:FOS) shares have been powering on, with a gain of 26% in the last thirty days. The annual gain comes to 113% following the latest surge, making investors sit up and take notice.

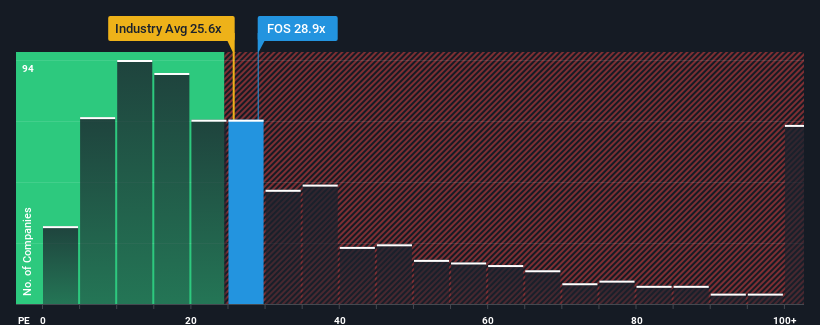

After such a large jump in price, given around half the companies in Australia have price-to-earnings ratios (or "P/E's") below 19x, you may consider FOS Capital as a stock to potentially avoid with its 28.9x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Earnings have risen at a steady rate over the last year for FOS Capital, which is generally not a bad outcome. One possibility is that the P/E is high because investors think this good earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for FOS Capital

How Is FOS Capital's Growth Trending?

In order to justify its P/E ratio, FOS Capital would need to produce impressive growth in excess of the market.

If we review the last year of earnings growth, the company posted a worthy increase of 2.9%. Still, lamentably EPS has fallen 48% in aggregate from three years ago, which is disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 27% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that FOS Capital is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

What We Can Learn From FOS Capital's P/E?

FOS Capital's P/E is getting right up there since its shares have risen strongly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that FOS Capital currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with FOS Capital, and understanding them should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:FOS

FOS Capital

Through its subsidiaries, manufactures and distributes commercial luminaires, outdoor fittings, linear extruded lighting, and architectural lighting solutions in Australia and New Zealand.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor