Advertisement

- Australia

- /

- Aerospace & Defense

- /

- ASX:DRO

DroneShield Limited (ASX:DRO) Stocks Shoot Up 33% But Its P/S Still Looks Reasonable

DroneShield Limited (ASX:DRO) shares have continued their recent momentum with a 33% gain in the last month alone. The annual gain comes to 222% following the latest surge, making investors sit up and take notice.

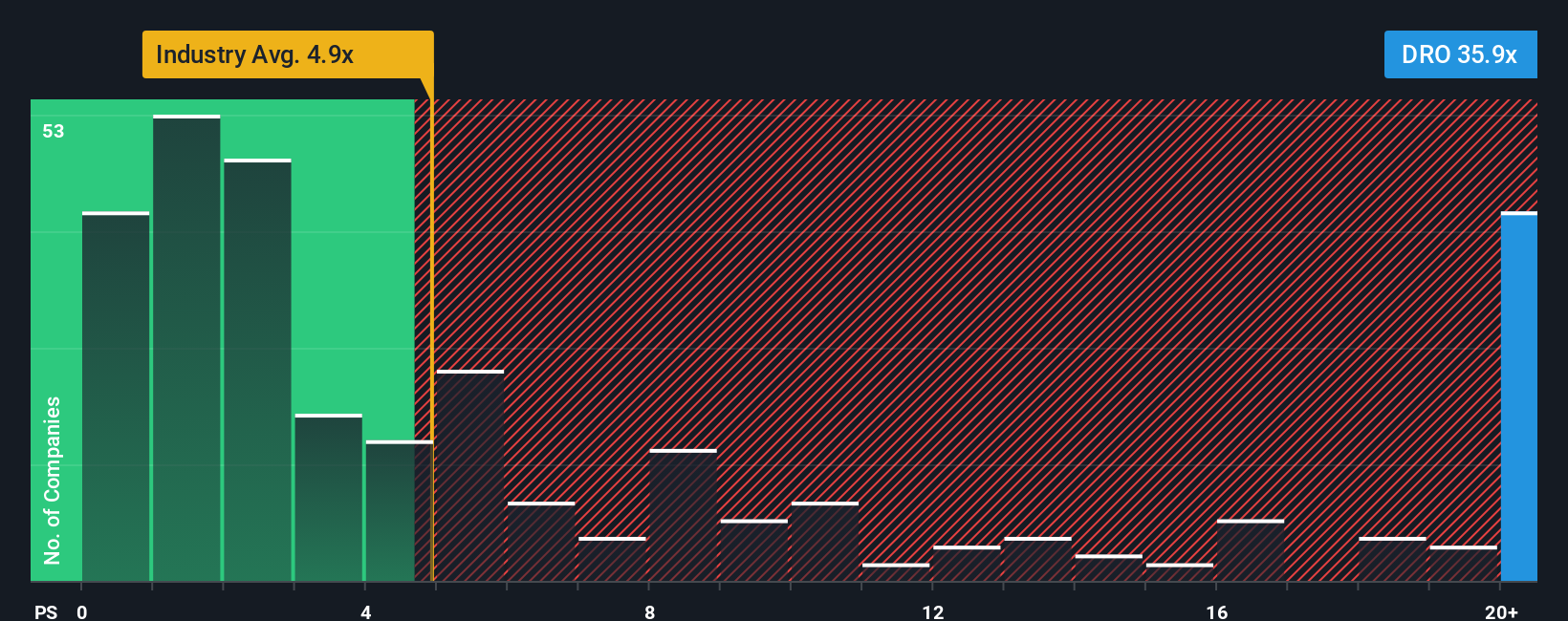

Following the firm bounce in price, DroneShield's price-to-sales (or "P/S") ratio of 35.9x might make it look like a strong sell right now compared to other companies in the Aerospace & Defense industry in Australia, where around half of the companies have P/S ratios below 4.8x and even P/S below 1.7x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for DroneShield

What Does DroneShield's Recent Performance Look Like?

DroneShield certainly has been doing a good job lately as it's been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on DroneShield will help you uncover what's on the horizon.How Is DroneShield's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as DroneShield's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 62% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 110% as estimated by the dual analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 17%, which is noticeably less attractive.

With this in mind, it's not hard to understand why DroneShield's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On DroneShield's P/S

Shares in DroneShield have seen a strong upwards swing lately, which has really helped boost its P/S figure. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that DroneShield maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Aerospace & Defense industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It is also worth noting that we have found 3 warning signs for DroneShield (1 is concerning!) that you need to take into consideration.

If you're unsure about the strength of DroneShield's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:DRO

DroneShield

Engages in the development, commercialization, and sale of hardware and software technology for drone detection and security in Australia and the United States.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor