Advertisement

- United Arab Emirates

- /

- Basic Materials

- /

- ADX:RAKWCT

Ras Al Khaimah Co. for White Cement & Construction Materials P.S.C. (ADX:RAKWCT) Investors Should Think About This Before Buying It For Its Dividend

Today we'll take a closer look at Ras Al Khaimah Co. for White Cement & Construction Materials P.S.C. (ADX:RAKWCT) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

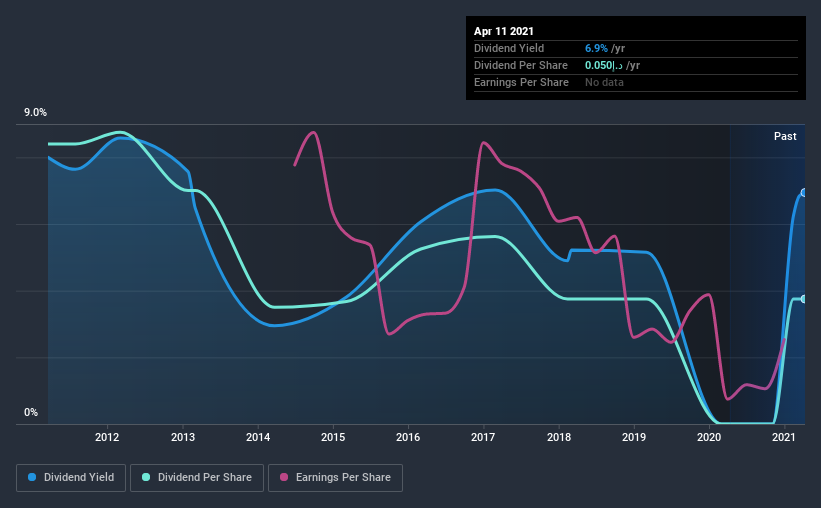

In this case, Ras Al Khaimah for White Cement & Construction Materials P.S.C likely looks attractive to investors, given its 6.9% dividend yield and a payment history of over ten years. It would not be a surprise to discover that many investors buy it for the dividends. Some simple analysis can reduce the risk of holding Ras Al Khaimah for White Cement & Construction Materials P.S.C for its dividend, and we'll focus on the most important aspects below.

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Ras Al Khaimah for White Cement & Construction Materials P.S.C paid out 197% of its profit as dividends, over the trailing twelve month period. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Ras Al Khaimah for White Cement & Construction Materials P.S.C paid out 2.7% of its free cash flow as dividends last year, which is conservative and suggests the dividend is sustainable. It's good to see that while Ras Al Khaimah for White Cement & Construction Materials P.S.C's dividends were not covered by profits, at least they are affordable from a cash perspective. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Very few companies are able to sustainably pay dividends larger than their reported earnings.

We update our data on Ras Al Khaimah for White Cement & Construction Materials P.S.C every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

One of the major risks of relying on dividend income, is the potential for a company to struggle financially and cut its dividend. Not only is your income cut, but the value of your investment declines as well - nasty. For the purpose of this article, we only scrutinise the last decade of Ras Al Khaimah for White Cement & Construction Materials P.S.C's dividend payments. The dividend has been cut on at least one occasion historically. During the past 10-year period, the first annual payment was د.إ0.1 in 2011, compared to د.إ0.05 last year. The dividend has shrunk at around 7.7% a year during that period. Ras Al Khaimah for White Cement & Construction Materials P.S.C's dividend hasn't shrunk linearly at 7.7% per annum, but the CAGR is a useful estimate of the historical rate of change.

We struggle to make a case for buying Ras Al Khaimah for White Cement & Construction Materials P.S.C for its dividend, given that payments have shrunk over the past 10 years.

Dividend Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Over the past five years, it looks as though Ras Al Khaimah for White Cement & Construction Materials P.S.C's EPS have declined at around 4.0% a year. If earnings continue to decline, the dividend may come under pressure. Every investor should make an assessment of whether the company is taking steps to stabilise the situation.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. We're not keen on the fact that Ras Al Khaimah for White Cement & Construction Materials P.S.C paid out such a high percentage of its income, although its cashflow is in better shape. Earnings per share are down, and Ras Al Khaimah for White Cement & Construction Materials P.S.C's dividend has been cut at least once in the past, which is disappointing. Overall, Ras Al Khaimah for White Cement & Construction Materials P.S.C falls short in several key areas here. Unless the investor has strong grounds for an alternative conclusion, we find it hard to get interested in a dividend stock with these characteristics.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 3 warning signs for Ras Al Khaimah for White Cement & Construction Materials P.S.C (of which 1 is significant!) you should know about.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

If you decide to trade Ras Al Khaimah for White Cement & Construction Materials P.S.C, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ADX:RAKWCT

Ras Al Khaimah for White Cement & Construction Materials P.S.C

Manufactures and supplies lime and cement products in the United Arab Emirates and internationally.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

88 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative