Advertisement

- United Arab Emirates

- /

- Insurance

- /

- DFM:TAKAFUL-EM

Why We're Not Concerned Yet About Takaful Emarat - Insurance (PSC)'s (DFM:TAKAFUL-EM) 28% Share Price Plunge

To the annoyance of some shareholders, Takaful Emarat - Insurance (PSC) (DFM:TAKAFUL-EM) shares are down a considerable 28% in the last month, which continues a horrid run for the company. For any long-term shareholders, the last month ends a year to forget by locking in a 50% share price decline.

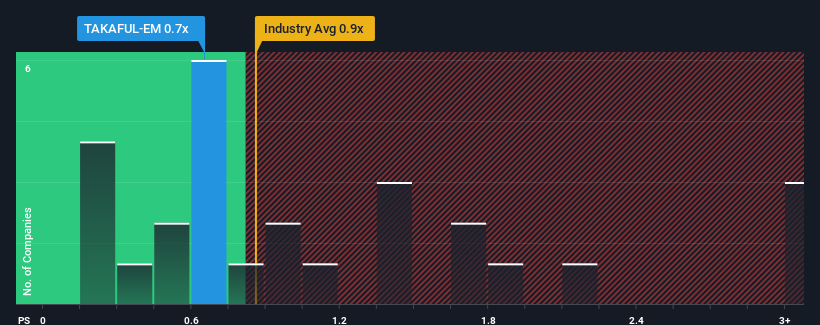

Even after such a large drop in price, you could still be forgiven for feeling indifferent about Takaful Emarat - Insurance (PSC)'s P/S ratio of 0.7x, since the median price-to-sales (or "P/S") ratio for the Insurance industry in the United Arab Emirates is also close to 0.9x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Takaful Emarat - Insurance (PSC)

How Has Takaful Emarat - Insurance (PSC) Performed Recently?

Recent times have been quite advantageous for Takaful Emarat - Insurance (PSC) as its revenue has been rising very briskly. The P/S is probably moderate because investors think this strong revenue growth might not be enough to outperform the broader industry in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Takaful Emarat - Insurance (PSC) will help you shine a light on its historical performance.Is There Some Revenue Growth Forecasted For Takaful Emarat - Insurance (PSC)?

Takaful Emarat - Insurance (PSC)'s P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, we see that the company grew revenue by an impressive 163% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 24% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

It's interesting to note that the rest of the industry is similarly expected to decline by 9.1% over the next year, which is just as bad as the company's recent medium-term revenue decline.

With this in mind, it's no surprise that Takaful Emarat - Insurance (PSC)'s P/S is similar to its industry peers. However, shrinking revenues are unlikely to lead to a stable P/S long-term, which could set up shareholders for future disappointment regardless. There is potential for the P/S to fall to lower levels if the company doesn't improve its top-line growth, which would be difficult to do with the current industry outlook.

What We Can Learn From Takaful Emarat - Insurance (PSC)'s P/S?

Following Takaful Emarat - Insurance (PSC)'s share price tumble, its P/S is just clinging on to the industry median P/S. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Takaful Emarat - Insurance (PSC) revealed its three-year contraction in revenue is resulting in a P/S that matches the industry, given the industry is also set to shrink at a similar rate. It would appear as though shareholders are comfortable with the current P/S ratio, as they seem to have confidence that future revenue will not result in any unfavourable surprises. Although, we are concerned whether the company's performance will worsen relative to other industry players under these tough industry conditions. If the company's performance remains relatively stable, it's likely that the current share price will continue to find support.

Before you take the next step, you should know about the 5 warning signs for Takaful Emarat - Insurance (PSC) (4 are a bit unpleasant!) that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Takaful Emarat - Insurance (PSC) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:TAKAFUL-EM

Takaful Emarat - Insurance (PSC)

Engages in the takaful insurance activities in the United Arab Emirates.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor