Advertisement

- United Arab Emirates

- /

- Consumer Services

- /

- ADX:DRIVE

Emirates Driving Company P.J.S.C. (ADX:DRIVE) On An Uptrend: Could Fundamentals Be Driving The Stock?

Emirates Driving Company P.J.S.C's (ADX:DRIVE) stock up by 7.9% over the past three months. As most would know, long-term fundamentals have a strong correlation with market price movements, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. In this article, we decided to focus on Emirates Driving Company P.J.S.C's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Emirates Driving Company P.J.S.C

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Emirates Driving Company P.J.S.C is:

18% = د.إ116m ÷ د.إ664m (Based on the trailing twelve months to June 2020).

The 'return' is the income the business earned over the last year. That means that for every AED1 worth of shareholders' equity, the company generated AED0.18 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Emirates Driving Company P.J.S.C's Earnings Growth And 18% ROE

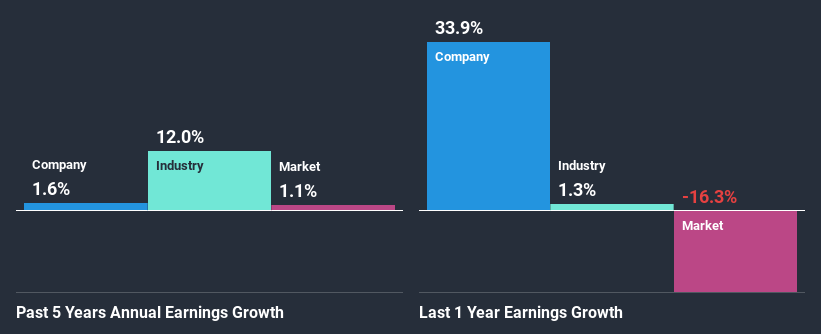

At first glance, Emirates Driving Company P.J.S.C seems to have a decent ROE. On comparing with the average industry ROE of 10% the company's ROE looks pretty remarkable. Given the circumstances, we can't help but wonder why Emirates Driving Company P.J.S.C saw little to no growth in the past five years. We reckon that there could be some other factors at play here that's limiting the company's growth. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for instance.

As a next step, we compared Emirates Driving Company P.J.S.C's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 13% in the same period.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is Emirates Driving Company P.J.S.C fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Emirates Driving Company P.J.S.C Using Its Retained Earnings Effectively?

Emirates Driving Company P.J.S.C has a high three-year median payout ratio of 55% (or a retention ratio of 45%), meaning that the company is paying most of its profits as dividends to its shareholders. This does go some way in explaining why there's been no growth in its earnings.

Additionally, Emirates Driving Company P.J.S.C has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth.

Conclusion

Overall, we feel that Emirates Driving Company P.J.S.C certainly does have some positive factors to consider. However, while the company does have a high ROE, its earnings growth number is quite disappointing. This can be blamed on the fact that it reinvests only a small portion of its profits and pays out the rest as dividends. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. To gain further insights into Emirates Driving Company P.J.S.C's past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you decide to trade Emirates Driving Company P.J.S.C, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emirates Driving Company P.J.S.C might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ADX:DRIVE

Emirates Driving Company P.J.S.C

Manages and develops motor vehicles driving training in the United Arab Emirates.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor