Advertisement

- United Arab Emirates

- /

- Food and Staples Retail

- /

- DFM:UNIONCOOP

Union Coop's (DFM:UNIONCOOP) Dismal Stock Performance Reflects Weak Fundamentals

It is hard to get excited after looking at Union Coop's (DFM:UNIONCOOP) recent performance, when its stock has declined 12% over the past three months. To decide if this trend could continue, we decided to look at its weak fundamentals as they shape the long-term market trends. Particularly, we will be paying attention to Union Coop's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Union Coop is:

13% = د.إ317m ÷ د.إ2.4b (Based on the trailing twelve months to March 2025).

The 'return' is the yearly profit. Another way to think of that is that for every AED1 worth of equity, the company was able to earn AED0.13 in profit.

Check out our latest analysis for Union Coop

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Union Coop's Earnings Growth And 13% ROE

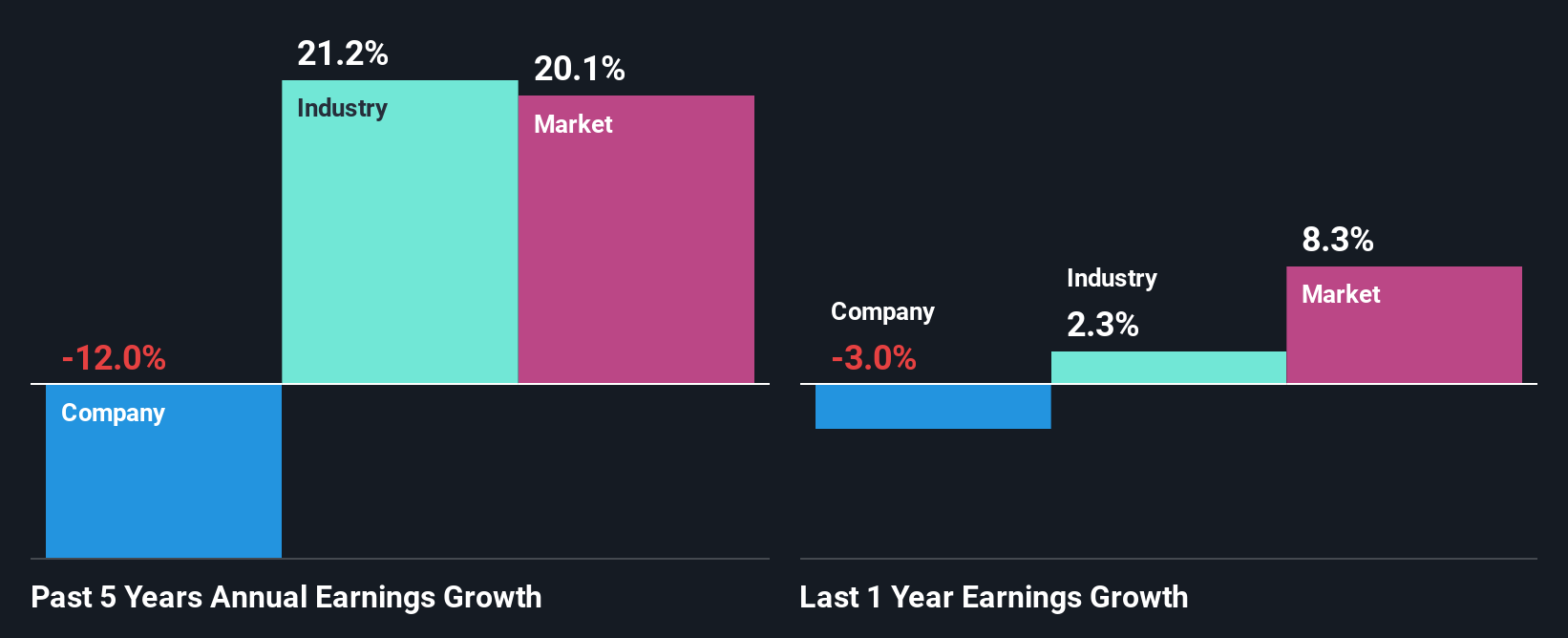

It is quite clear that Union Coop's ROE is rather low. An industry comparison shows that the company's ROE is not much different from the industry average of 14% either. Given the circumstances, the significant decline in net income by 12% seen by Union Coop over the last five years is not surprising.

So, as a next step, we compared Union Coop's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 21% over the last few years.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Union Coop fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Union Coop Efficiently Re-investing Its Profits?

Union Coop's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 86% (or a retention ratio of 14%). With only very little left to reinvest into the business, growth in earnings is far from likely. You can see the 2 risks we have identified for Union Coop by visiting our risks dashboard for free on our platform here.

Only recently, Union Coop stated paying a dividend. This likely means that the management might have concluded that its shareholders have a strong preference for dividends.

Conclusion

Overall, we would be extremely cautious before making any decision on Union Coop. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. So far, we've only made a quick discussion around the company's earnings growth. So it may be worth checking this free detailed graph of Union Coop's past earnings, as well as revenue and cash flows to get a deeper insight into the company's performance.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DFM:UNIONCOOP

Union Coop

Union Coop establishes and manages hypermarkets and consumer cooperatives in the United Arab Emirates.

Average dividend payer with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor