Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:PEY

Why You Should Leave Peyto Exploration & Development Corp. (TSE:PEY)'s Upcoming Dividend On The Shelf

Peyto Exploration & Development Corp. (TSE:PEY) is about to trade ex-dividend in the next 4 days. Investors can purchase shares before the 30th of January in order to be eligible for this dividend, which will be paid on the 14th of February.

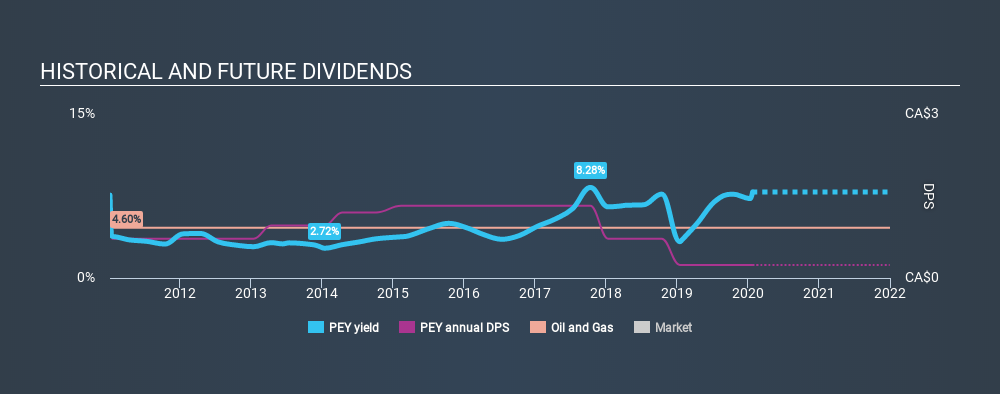

Peyto Exploration & Development's next dividend payment will be CA$0.02 per share, on the back of last year when the company paid a total of CA$0.24 to shareholders. Calculating the last year's worth of payments shows that Peyto Exploration & Development has a trailing yield of 7.9% on the current share price of CA$3.05. If you buy this business for its dividend, you should have an idea of whether Peyto Exploration & Development's dividend is reliable and sustainable. So we need to investigate whether Peyto Exploration & Development can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Peyto Exploration & Development

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. That's why it's good to see Peyto Exploration & Development paying out a modest 39% of its earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 67% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If earnings fall far enough, the company could be forced to cut its dividend. That explains why we're not overly excited about Peyto Exploration & Development's flat earnings over the past five years. Better than seeing them fall off a cliff, for sure, but the best dividend stocks grow their earnings meaningfully over the long run.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Peyto Exploration & Development's dividend payments per share have declined at 18% per year on average over the past nine years, which is uninspiring.

The Bottom Line

Should investors buy Peyto Exploration & Development for the upcoming dividend? Earnings per share are down very slightly in recent times, and Peyto Exploration & Development paid out less half its profit and more than half its cash flow as dividends, which is not the worst combination but could be better. Overall we're not hugely bearish on the stock, but there are likely better dividend investments out there.

Wondering what the future holds for Peyto Exploration & Development? See what the two analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:PEY

Peyto Exploration & Development

Engages in the exploration, development, and production of natural gas, oil, and natural gas liquids in Alberta’s deep basin.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor