Advertisement

Elmo Software Limited's (ASX:ELO): Elmo Software Limited provides software-as-a-service, cloud-based human resource (HR) and payroll solutions for organizations in Australia, New Zealand, and Singapore. The AU$617m market-cap posted a loss in its most recent financial year of -AU$13.2m and a latest trailing-twelve-month loss of -AU$14.5m leading to an even wider gap between loss and breakeven. As path to profitability is the topic on ELO’s investors mind, I’ve decided to gauge market sentiment. In this article, I will touch on the expectations for ELO’s growth and when analysts expect the company to become profitable.

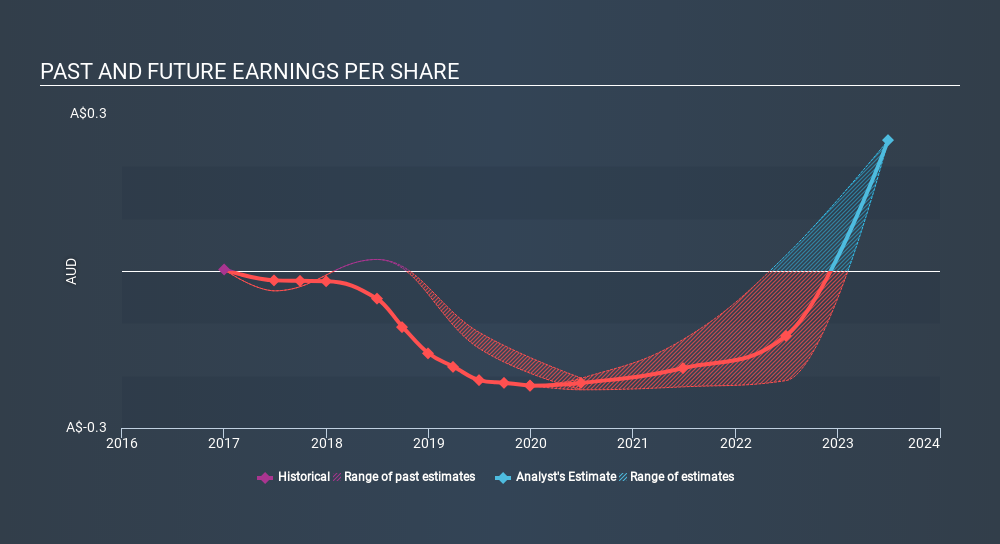

Check out our latest analysis for Elmo Software

Consensus from the 6 Software analysts is ELO is on the verge of breakeven. They expect the company to post a final loss in 2022, before turning a profit of AU$16m in 2023. ELO is therefore projected to breakeven around 3 years from today. In order to meet this breakeven date, I calculated the rate at which ELO must grow year-on-year. It turns out an average annual growth rate of 39% is expected, which signals high confidence from analysts. If this rate turns out to be too aggressive, ELO may become profitable much later than analysts predict.

I’m not going to go through company-specific developments for ELO given that this is a high-level summary, though, bear in mind that typically a high forecast growth rate is not unusual for a company that is currently undergoing an investment period.

One thing I’d like to point out is that ELO has no debt on its balance sheet, which is rare for a loss-making loss-making, growth company, which usually has a high level of debt relative to its equity. This means that ELO has been operating purely on its equity investment and has no debt burden. This aspect reduces the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on ELO, so if you are interested in understanding the company at a deeper level, take a look at ELO’s company page on Simply Wall St. I’ve also compiled a list of relevant aspects you should further examine:

- Valuation: What is ELO worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether ELO is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Elmo Software’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ASX:ELO

ELMO Software

ELMO Software Limited provides software-as-a-service, cloud-based human resource (HR), payroll, and expense management solutions in Australia, New Zealand, the United Kingdom, and internationally.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor