Advertisement

- Netherlands

- /

- Metals and Mining

- /

- ENXTAM:MT

What Are Analysts Expecting From ArcelorMittal (AMS:MT) In The Years Ahead?

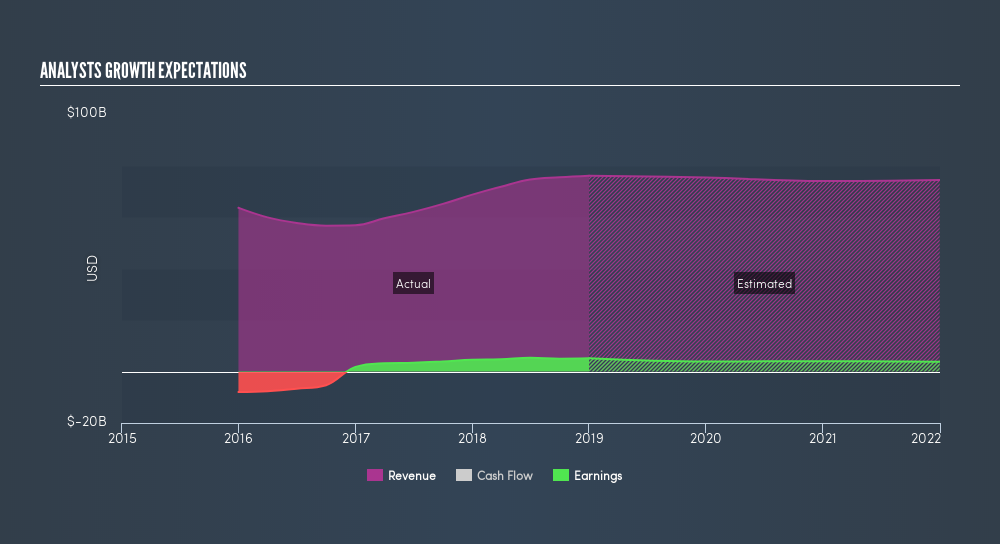

ArcelorMittal's (AMS:MT) latest earnings announcement in December 2018 suggested that the company benefited from a strong tailwind, leading to a double-digit earnings growth of 13%. Below is a brief commentary on my key takeaways on how market analysts view ArcelorMittal's earnings growth outlook over the next few years and whether the future looks even brighter than the past. I will be using net income excluding extraordinary items in order to exclude one-off volatility which I am not interested in.

Check out our latest analysis for ArcelorMittal

Analysts' outlook for the upcoming year seems pessimistic, with earnings decreasing by a double-digit -25%. Over the medium term, earnings are predicted to continue to be below today's level, with a decline of -23% in 2021, eventually reaching US$4.0b in 2022.

Although it’s helpful to be aware of the rate of growth each year relative to today’s level, it may be more valuable analyzing the rate at which the earnings are growing on average every year. The advantage of this method is that it removes the impact of near term flucuations and accounts for the overarching direction of ArcelorMittal's earnings trajectory over time, fluctuate up and down. To calculate this rate, I put a line of best fit through analyst consensus of forecasted earnings. The slope of this line is the rate of earnings growth, which in this case is -11%. This means that, we can anticipate ArcelorMittal will chip away at a rate of -11% every year for the next few years.

Next Steps:

For ArcelorMittal, there are three essential factors you should further examine:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is MT worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MT is currently mispriced by the market.

- Other High-Growth Alternatives: Are there other high-growth stocks you could be holding instead of MT? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTAM:MT

ArcelorMittal

Operates as integrated steel and mining companies in the Americas, Europe, Asia, and Africa.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

EP

Epstein_Research on Blackrock Silver ·

Are Blackrock Silver shares oversold?

Fair Value:CA$370.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Ares Strategic Mining ·

Ares Strategic Mining: $250M Pentagon Contract vs C$76M Market Cap

Fair Value:CA$0.9371.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DS

DS2invest on PayPal Holdings ·

PayPal: Undervalued Cash Flow Machine or Value Trap?

Fair Value:US$69.0318.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

60 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0