Advertisement

- United States

- /

- Energy Services

- /

- NasdaqCM:MIND

We're Not Worried About Mitcham Industries's (NASDAQ:MIND) Cash Burn

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

Given this risk, we thought we'd take a look at whether Mitcham Industries (NASDAQ:MIND) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business's cash, relative to its cash burn.

View our latest analysis for Mitcham Industries

Does Mitcham Industries Have A Long Cash Runway?

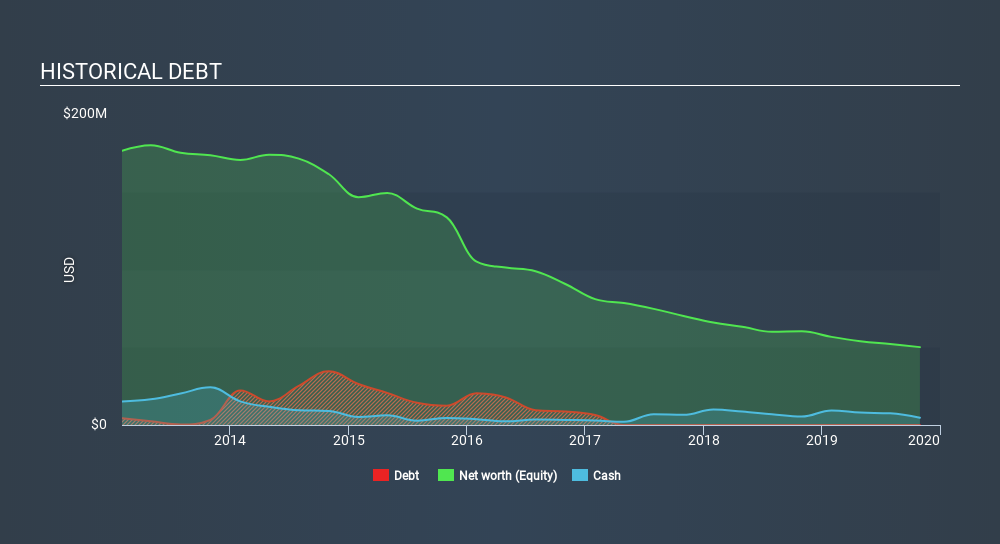

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. As at October 2019, Mitcham Industries had cash of US$4.7m and no debt. In the last year, its cash burn was US$2.0m. Therefore, from October 2019 it had 2.3 years of cash runway. Importantly, though, the one analyst we see covering the stock thinks that Mitcham Industries will reach cashflow breakeven before then. In that case, it may never reach the end of its cash runway. The image below shows how its cash balance has been changing over the last few years.

How Well Is Mitcham Industries Growing?

Happily, Mitcham Industries is travelling in the right direction when it comes to its cash burn, which is down 73% over the last year. However, operating revenue growth was flat over the period. It seems to be growing nicely. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Mitcham Industries Raise Cash?

While Mitcham Industries seems to be in a decent position, we reckon it is still worth thinking about how easily it could raise more cash, if that proved desirable. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash to fund growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Mitcham Industries's cash burn of US$2.0m is about 5.8% of its US$35m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

How Risky Is Mitcham Industries's Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way Mitcham Industries is burning through its cash. In particular, we think its cash burn reduction stands out as evidence that the company is well on top of its spending. Its weak point is its revenue growth, but even that wasn't too bad! There's no doubt that shareholders can take a lot of heart from the fact that at least one analyst is forecasting it will reach breakeven before too long. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Notably, our data indicates that Mitcham Industries insiders have been trading the shares. You can discover if they are buyers or sellers by clicking on this link.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqCM:MIND

MIND Technology

Provides technology to the oceanographic, hydrographic, defense, seismic, and maritime security industries in the United States, China, Norway, Turkey, Singapore, Canada, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|12.0% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|5.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|57.3% overvalued

UN

Community Contributor