Advertisement

- Spain

- /

- Electric Utilities

- /

- BME:RED

We Think Red Eléctrica Corporación (BME:REE) Can Stay On Top Of Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Red Eléctrica Corporación, S.A. (BME:REE) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Red Eléctrica Corporación

What Is Red Eléctrica Corporación's Net Debt?

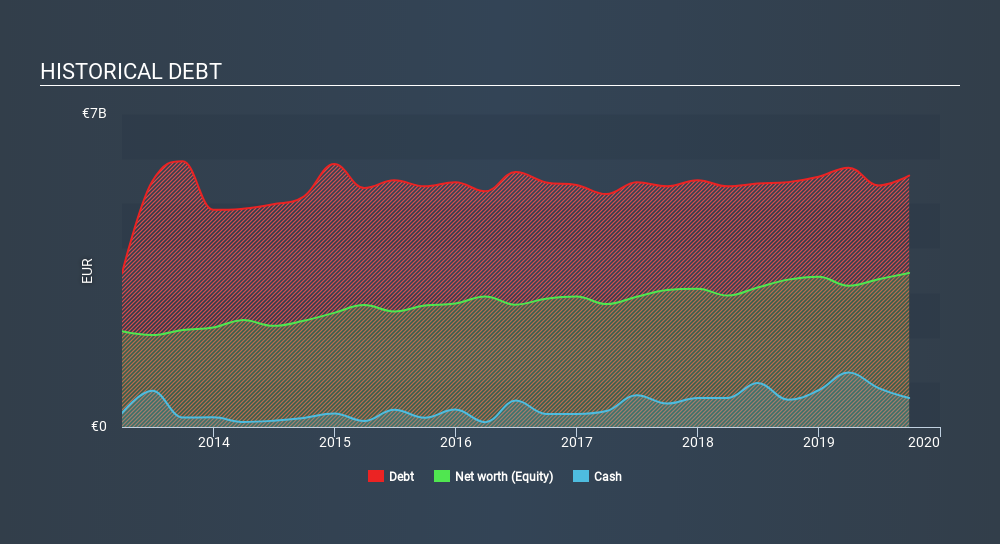

You can click the graphic below for the historical numbers, but it shows that as of September 2019 Red Eléctrica Corporación had €5.61b of debt, an increase on €5.5k, over one year. On the flip side, it has €648.5m in cash leading to net debt of about €4.96b.

How Healthy Is Red Eléctrica Corporación's Balance Sheet?

We can see from the most recent balance sheet that Red Eléctrica Corporación had liabilities of €2.03b falling due within a year, and liabilities of €5.99b due beyond that. Offsetting this, it had €648.5m in cash and €1.37b in receivables that were due within 12 months. So its liabilities total €6.00b more than the combination of its cash and short-term receivables.

This is a mountain of leverage even relative to its gargantuan market capitalization of €9.83b. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt to EBITDA of 3.2 Red Eléctrica Corporación has a fairly noticeable amount of debt. On the plus side, its EBIT was 8.1 times its interest expense, and its net debt to EBITDA, was quite high, at 3.2. We saw Red Eléctrica Corporación grow its EBIT by 3.8% in the last twelve months. Whilst that hardly knocks our socks off it is a positive when it comes to debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Red Eléctrica Corporación can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Red Eléctrica Corporación recorded free cash flow worth 64% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Red Eléctrica Corporación's conversion of EBIT to free cash flow was a real positive on this analysis, as was its interest cover. On the other hand, its net debt to EBITDA makes us a little less comfortable about its debt. We would also note that Electric Utilities industry companies like Red Eléctrica Corporación commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Red Eléctrica Corporación's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Red Eléctrica Corporación you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BME:RED

Redeia Corporación

Engages in the electricity transmission, and system operation and management of the transmission network for the electricity system in Spain and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor