Advertisement

We Think 8K Miles Software Services (NSE:8KMILES) Can Stay On Top Of Its Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that 8K Miles Software Services Limited (NSE:8KMILES) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View 4 warning signs we detected for 8K Miles Software Services

What Is 8K Miles Software Services's Net Debt?

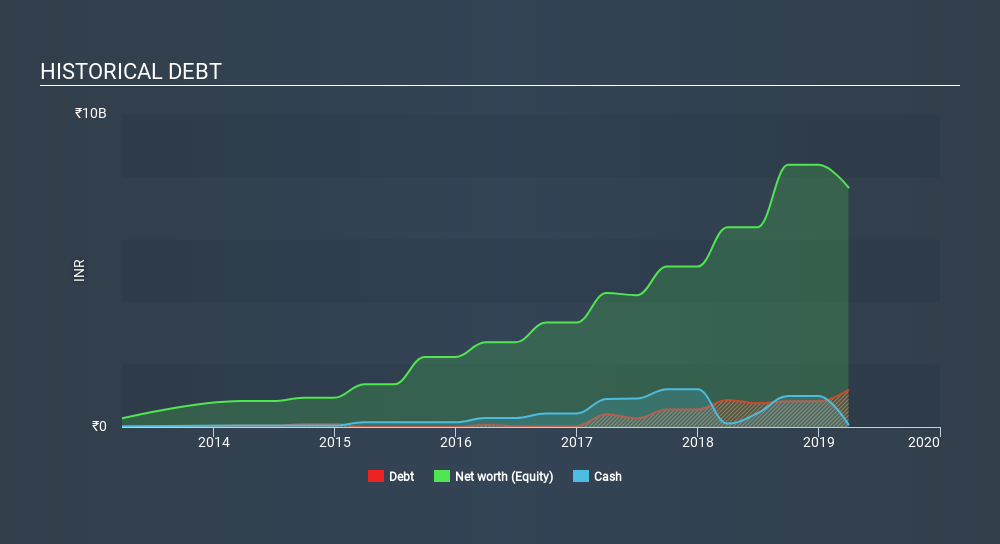

You can click the graphic below for the historical numbers, but it shows that as of March 2019 8K Miles Software Services had ₹1.18b of debt, an increase on ₹865, over one year. On the flip side, it has ₹81.5m in cash leading to net debt of about ₹1.10b.

A Look At 8K Miles Software Services's Liabilities

Zooming in on the latest balance sheet data, we can see that 8K Miles Software Services had liabilities of ₹1.70b due within 12 months and liabilities of ₹621.7m due beyond that. On the other hand, it had cash of ₹81.5m and ₹2.86b worth of receivables due within a year. So it actually has ₹619.8m more liquid assets than total liabilities.

This luscious liquidity implies that 8K Miles Software Services's balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

8K Miles Software Services has a low net debt to EBITDA ratio of only 1.00. And its EBIT easily covers its interest expense, being 12.9 times the size. So we're pretty relaxed about its super-conservative use of debt. It is just as well that 8K Miles Software Services's load is not too heavy, because its EBIT was down 63% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But it is 8K Miles Software Services's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Considering the last three years, 8K Miles Software Services actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

We weren't impressed with 8K Miles Software Services's conversion of EBIT to free cash flow, and its EBIT growth rate made us cautious. But like a ballerina ending on a perfect pirouette, it has not trouble covering its interest expense with its EBIT. When we consider all the elements mentioned above, it seems to us that 8K Miles Software Services is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for 8K Miles Software Services (of which 2 are major) which any shareholder or potential investor should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:SECURKLOUD

SecureKloud Technologies

Provides information and technology services in India, the United States, Canada, Ireland, and Australia.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor