Advertisement

- India

- /

- Renewable Energy

- /

- NSEI:RPOWER

We Like These Underlying Trends At Reliance Power (NSE:RPOWER)

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings back into the business at ever-higher rates of return. With that in mind, we've noticed some promising trends at Reliance Power (NSE:RPOWER) so let's look a bit deeper.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Reliance Power is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

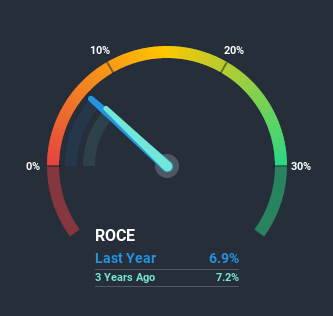

0.069 = ₹26b ÷ (₹533b - ₹160b) (Based on the trailing twelve months to March 2020).

Thus, Reliance Power has an ROCE of 6.9%. Even though it's in line with the industry average of 7.1%, it's still a low return by itself.

View our latest analysis for Reliance Power

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Reliance Power's past further, check out this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Reliance Power Tell Us?

Reliance Power has not disappointed in regards to ROCE growth. The data shows that returns on capital have increased by 73% over the trailing five years. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. In regards to capital employed, Reliance Power appears to been achieving more with less, since the business is using 28% less capital to run its operation. If this trend continues, the business might be getting more efficient but it's shrinking in terms of total assets.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 30% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.In Conclusion...

From what we've seen above, Reliance Power has managed to increase it's returns on capital all the while reducing it's capital base. However the stock is down a substantial 91% in the last five years so there could be other areas of the business hurting its prospects. Regardless, we think the underlying fundamentals warrant this stock for further investigation.

On a final note, we found 3 warning signs for Reliance Power (2 don't sit too well with us) you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you decide to trade Reliance Power, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account.Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:RPOWER

Reliance Power

Engages in the development, construction, and operation of power projects in India and internationally.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

163 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Korea Electric Power ·

Korea Electric Power Corp (KEP): The Grid’s Tug-of-War – AI Demand vs. The Strait of Hormuz

Fair Value:US$32.5150.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Coherent ·

Coherent Corp. (COHR): The Optical AI Engine – Scaling the Photon-Silicon Frontier

Fair Value:US$2501.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GL

GlennUrban on High Tide ·

High Tide's Future Potential Will Surge with 15% Revenue Growth

Fair Value:US$1281.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0