Advertisement

- United States

- /

- Machinery

- /

- NYSE:SXI

Three Things You Should Check Before Buying Standex International Corporation (NYSE:SXI) For Its Dividend

Could Standex International Corporation (NYSE:SXI) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. Yet sometimes, investors buy a stock for its dividend and lose money because the share price falls by more than they earned in dividend payments.

A slim 1.1% yield is hard to get excited about, but the long payment history is respectable. At the right price, or with strong growth opportunities, Standex International could have potential. The company also bought back stock equivalent to around 3.2% of market capitalisation this year. Some simple research can reduce the risk of buying Standex International for its dividend - read on to learn more.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Looking at the data, we can see that 22% of Standex International's profits were paid out as dividends in the last 12 months. Given the low payout ratio, it is hard to envision the dividend coming under threat, barring a catastrophe.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Standex International's cash payout ratio last year was 21%, which is quite low and suggests that the dividend was thoroughly covered by cash flow. It's positive to see that Standex International's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Remember, you can always get a snapshot of Standex International's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

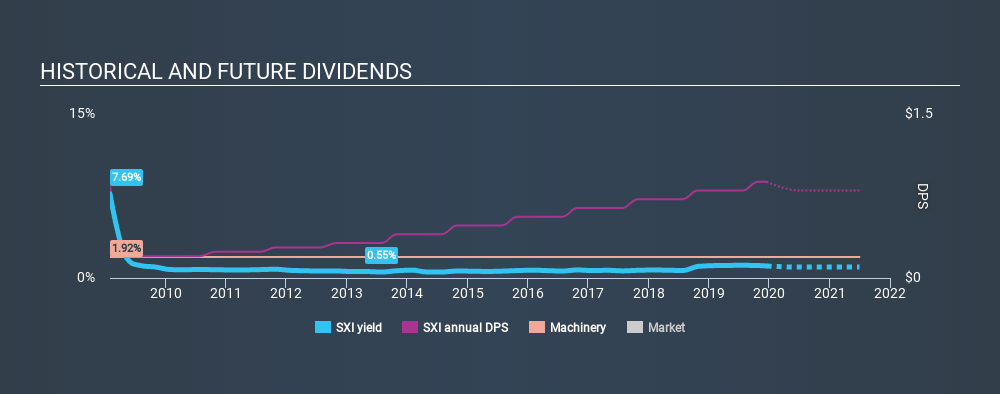

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of Standex International's dividend payments. Its dividend payments have fallen by 20% or more on at least one occasion over the past ten years. During the past ten-year period, the first annual payment was US$0.84 in 2009, compared to US$0.88 last year. Its dividends have grown at less than 1% per annum over this time frame.

It's good to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth, anyway. We're not that enthused by this.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? While there may be fluctuations in the past , Standex International's earnings per share have basically not grown from where they were five years ago. Flat earnings per share are acceptable for a time, but over the long term, the purchasing power of the company's dividends could be eroded by inflation.

Conclusion

To summarise, shareholders should always check that Standex International's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. It's great to see that Standex International is paying out a low percentage of its earnings and cash flow. Earnings per share have been falling, and the company has cut its dividend at least once in the past. From a dividend perspective, this is a cause for concern. In sum, we find it hard to get excited about Standex International from a dividend perspective. It's not that we think it's a bad business; just that there are other companies that perform better on these criteria.

Given that earnings are not growing, the dividend does not look nearly so attractive. Very few businesses see earnings consistently shrink year after year in perpetuity though, and so it might be worth seeing what the 4 analysts we track are forecasting for the future.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:SXI

Standex International

Together with subsidiaries, engages in the manufacture and sale of various products and services for commercial and industrial markets in the United States and internationally.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor