Advertisement

These Metrics Don't Make Lokesh Machines (NSE:LOKESHMACH) Look Too Strong

If we're looking to avoid a business that is in decline, what are the trends that can warn us ahead of time? Businesses in decline often have two underlying trends, firstly, a declining return on capital employed (ROCE) and a declining base of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. So after glancing at the trends within Lokesh Machines (NSE:LOKESHMACH), we weren't too hopeful.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Lokesh Machines, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.007 = ₹11m ÷ (₹2.8b - ₹1.2b) (Based on the trailing twelve months to June 2020).

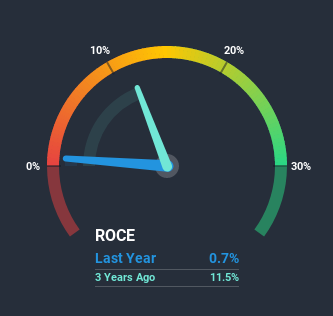

Thus, Lokesh Machines has an ROCE of 0.7%. Ultimately, that's a low return and it under-performs the Machinery industry average of 9.9%.

See our latest analysis for Lokesh Machines

Historical performance is a great place to start when researching a stock so above you can see the gauge for Lokesh Machines' ROCE against it's prior returns. If you're interested in investigating Lokesh Machines' past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Lokesh Machines' ROCE Trending?

There is reason to be cautious about Lokesh Machines, given the returns are trending downwards. About five years ago, returns on capital were 11%, however they're now substantially lower than that as we saw above. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Since returns are falling and the business has the same amount of assets employed, this can suggest it's a mature business that hasn't had much growth in the last five years. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Lokesh Machines becoming one if things continue as they have.

Another thing to note, Lokesh Machines has a high ratio of current liabilities to total assets of 42%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.In Conclusion...

In summary, it's unfortunate that Lokesh Machines is generating lower returns from the same amount of capital. Long term shareholders who've owned the stock over the last five years have experienced a 69% depreciation in their investment, so it appears the market might not like these trends either. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

One more thing: We've identified 3 warning signs with Lokesh Machines (at least 2 which are potentially serious) , and understanding them would certainly be useful.

While Lokesh Machines isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading Lokesh Machines or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:LOKESHMACH

Low and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.8% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|20.2% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|26.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|6.9% overvalued

TO

Community Contributor