Advertisement

These 4 Measures Indicate That High Liner Foods (TSE:HLF) Is Using Debt Extensively

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that High Liner Foods Incorporated (TSE:HLF) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for High Liner Foods

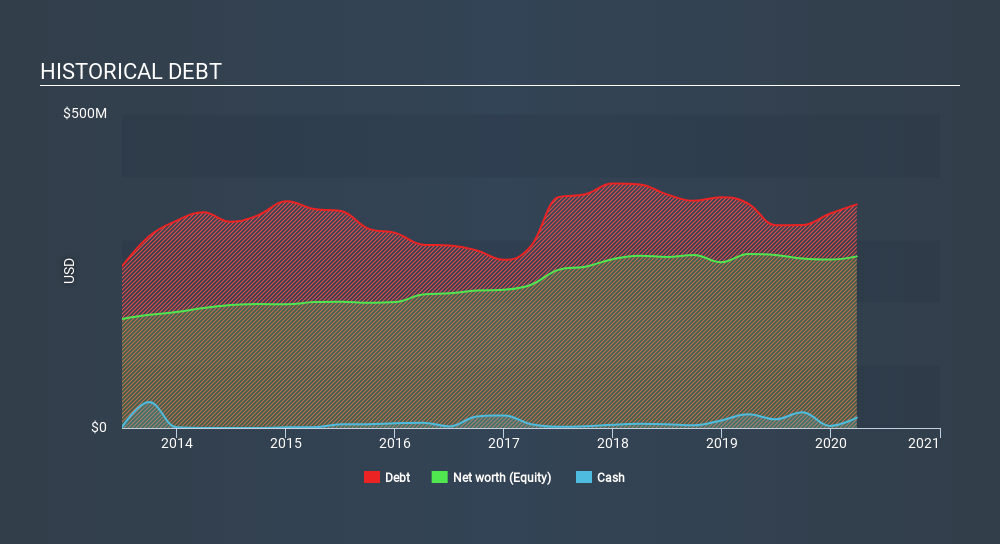

What Is High Liner Foods's Net Debt?

As you can see below, High Liner Foods had US$356.0m of debt, at March 2020, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has US$16.6m in cash leading to net debt of about US$339.5m.

How Strong Is High Liner Foods's Balance Sheet?

We can see from the most recent balance sheet that High Liner Foods had liabilities of US$170.6m falling due within a year, and liabilities of US$348.0m due beyond that. On the other hand, it had cash of US$16.6m and US$104.8m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$397.2m.

This deficit casts a shadow over the US$159.7m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, High Liner Foods would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

High Liner Foods has a debt to EBITDA ratio of 4.6 and its EBIT covered its interest expense 2.6 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Looking on the bright side, High Liner Foods boosted its EBIT by a silky 33% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if High Liner Foods can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, High Liner Foods's free cash flow amounted to 42% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

We'd go so far as to say High Liner Foods's level of total liabilities was disappointing. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Overall, we think it's fair to say that High Liner Foods has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for High Liner Foods you should be aware of, and 1 of them is a bit concerning.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About TSX:HLF

High Liner Foods

Processes and markets prepared and packaged frozen seafood products in North America.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This Gold Stock Could Triple if Its Gold Resource Grows

Fair Value:CA$466.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9720.3% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$23.861.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Hektar Real Estate Investment Trust ·

Hektar REIT: Deep Value, Attractive Yield, and a Portfolio Transformation Story in the Making

Fair Value:RM 156.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on CSG ·

CSG represents a high-quality industrial compounder operating in a structurally growing and geopolitically reinforced market,

Fair Value:€3037.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

artoflosing on BlackBerry ·

Accidental transformation from Phones to Physical AI.

Fair Value:CA$16.2228.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.1% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6120.0% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

35 likesusers have liked this narrative