Advertisement

- United States

- /

- Building

- /

- NasdaqGS:APOG

These 4 Measures Indicate That Apogee Enterprises (NASDAQ:APOG) Is Using Debt Extensively

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Apogee Enterprises, Inc. (NASDAQ:APOG) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Apogee Enterprises

What Is Apogee Enterprises's Debt?

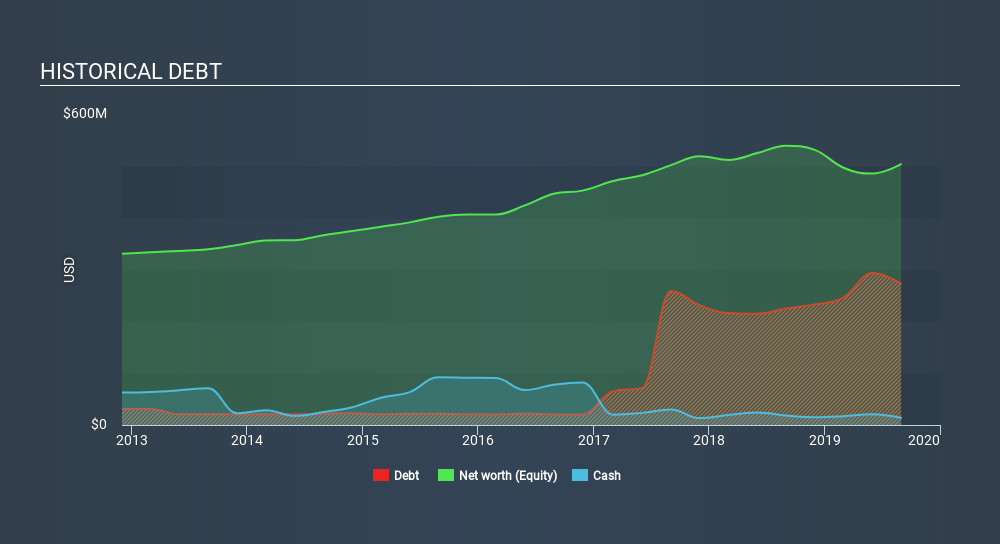

The image below, which you can click on for greater detail, shows that at August 2019 Apogee Enterprises had debt of US$272.8m, up from US$224.9m in one year. However, because it has a cash reserve of US$13.8m, its net debt is less, at about US$259.0m.

How Healthy Is Apogee Enterprises's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Apogee Enterprises had liabilities of US$371.3m due within 12 months and liabilities of US$264.5m due beyond that. Offsetting this, it had US$13.8m in cash and US$276.9m in receivables that were due within 12 months. So its liabilities total US$345.0m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Apogee Enterprises has a market capitalization of US$1.02b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Apogee Enterprises's net debt of 2.3 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 7.1 times interest expense) certainly does not do anything to dispel this impression. Shareholders should be aware that Apogee Enterprises's EBIT was down 39% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Apogee Enterprises can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Apogee Enterprises recorded free cash flow worth 51% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Apogee Enterprises's struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. But on the bright side, its ability to to cover its interest expense with its EBIT isn't too shabby at all. When we consider all the factors discussed, it seems to us that Apogee Enterprises is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. Given our hesitation about the stock, it would be good to know if Apogee Enterprises insiders have sold any shares recently. You click here to find out if insiders have sold recently.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:APOG

Apogee Enterprises

Provides architectural products and services for enclosing buildings, and glass and acrylic products used for preservation, protection, and enhanced viewing in the United States, Canada, and Brazil.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor