- United States

- /

- Electrical

- /

- NYSE:THR

Thermon Group Holdings, Inc. Just Missed EPS By 28%: Here's What Analysts Think Will Happen Next

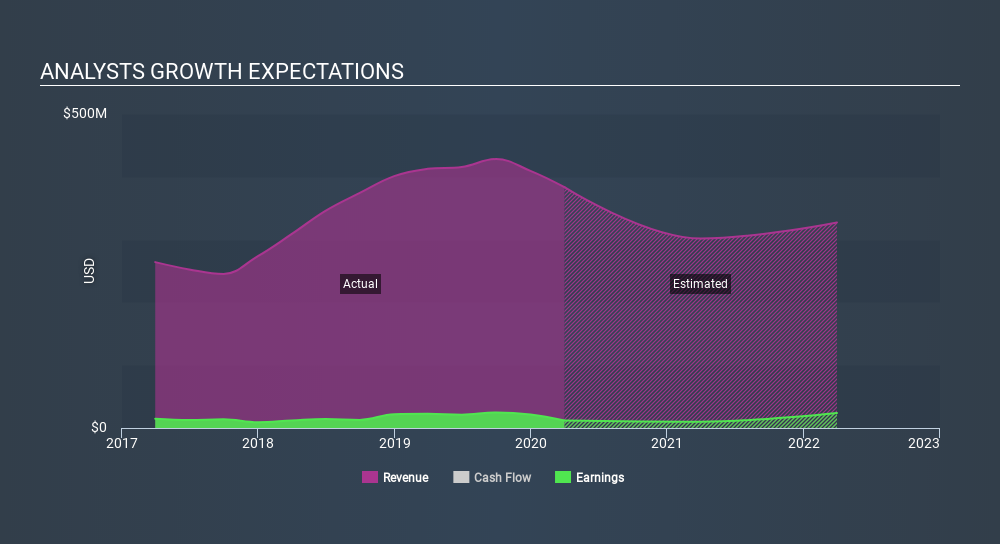

Thermon Group Holdings, Inc. (NYSE:THR) shareholders are probably feeling a little disappointed, since its shares fell 4.3% to US$15.63 in the week after its latest yearly results. Statutory earnings per share fell badly short of expectations, coming in at US$0.36, some 28% below analyst forecasts, although revenues were okay, approximately in line with analyst estimates at US$383m. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for Thermon Group Holdings

Taking into account the latest results, the two analysts covering Thermon Group Holdings provided consensus estimates of US$301.8m revenue in 2021, which would reflect a stressful 21% decline on its sales over the past 12 months. Statutory earnings per share are forecast to fall 18% to US$0.30 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$351.9m and earnings per share (EPS) of US$0.50 in 2021. It looks like sentiment has declined substantially in the aftermath of these results, with a real cut to revenue estimates and a pretty serious reduction to earnings per share numbers as well.

It'll come as no surprise then, to learn that the analysts have cut their price target 7.5% to US$18.50.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast revenue decline of 21%, a significant reduction from annual growth of 9.2% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.7% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Thermon Group Holdings is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Thermon Group Holdings' future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Thermon Group Holdings going out as far as 2022, and you can see them free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Thermon Group Holdings (including 1 which is significant) .

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NYSE:THR

Thermon Group Holdings

Provides engineered industrial process heating solutions for process industries in the United States and Latin America, Canada, Europe, the Middle East, Africa, and the Asia-Pacific.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion