Advertisement

- Taiwan

- /

- Real Estate

- /

- TWSE:5525

Sweeten Real Estate DevelopmentLtd (TPE:5525) Seems To Be Using An Awful Lot Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Sweeten Real Estate Development Co.,Ltd. (TPE:5525) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Sweeten Real Estate DevelopmentLtd

What Is Sweeten Real Estate DevelopmentLtd's Debt?

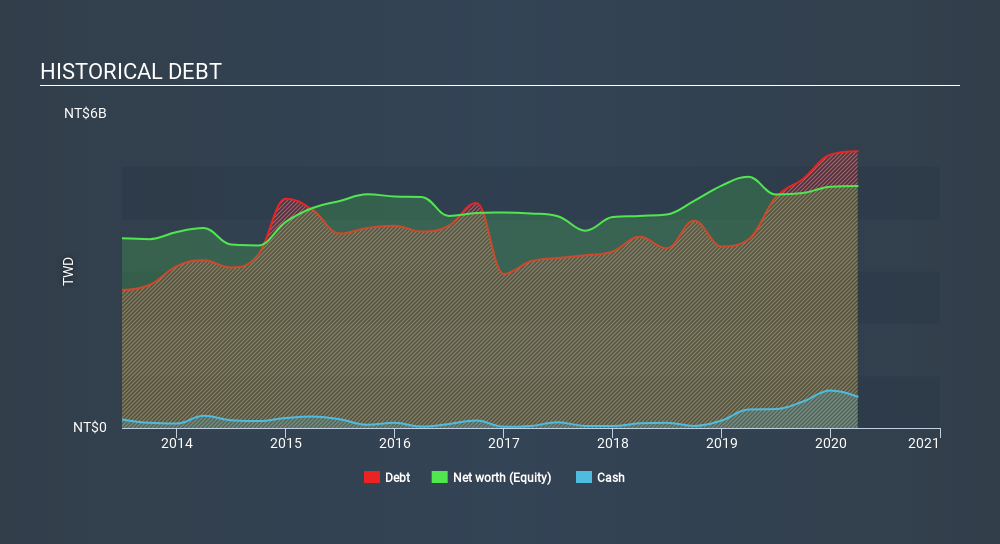

The image below, which you can click on for greater detail, shows that at March 2020 Sweeten Real Estate DevelopmentLtd had debt of NT$5.29b, up from NT$3.60b in one year. However, because it has a cash reserve of NT$597.1m, its net debt is less, at about NT$4.69b.

How Healthy Is Sweeten Real Estate DevelopmentLtd's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Sweeten Real Estate DevelopmentLtd had liabilities of NT$7.14b due within 12 months and liabilities of NT$508.4m due beyond that. Offsetting this, it had NT$597.1m in cash and NT$361.6m in receivables that were due within 12 months. So it has liabilities totalling NT$6.69b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of NT$5.02b, we think shareholders really should watch Sweeten Real Estate DevelopmentLtd's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Sweeten Real Estate DevelopmentLtd's net debt to EBITDA ratio is 14.9 which suggests rather high debt levels, but its interest cover of 8.6 times suggests the debt is easily serviced. Overall we'd say it seems likely the company is carrying a fairly heavy swag of debt. Shareholders should be aware that Sweeten Real Estate DevelopmentLtd's EBIT was down 74% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But it is Sweeten Real Estate DevelopmentLtd's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, Sweeten Real Estate DevelopmentLtd actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

On the face of it, Sweeten Real Estate DevelopmentLtd's net debt to EBITDA left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its interest cover is a good sign, and makes us more optimistic. After considering the datapoints discussed, we think Sweeten Real Estate DevelopmentLtd has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 3 warning signs for Sweeten Real Estate DevelopmentLtd (1 is potentially serious) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About TWSE:5525

Sweeten Real Estate DevelopmentLtd

Sweeten Real Estate Development Co.,Ltd. constructs, develops, leases, and sells residential, commercial, and industrial area.

Mediocre balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor