Advertisement

- United States

- /

- Building

- /

- NYSE:SSD

Simpson Manufacturing Co., Inc. Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

A week ago, Simpson Manufacturing Co., Inc. (NYSE:SSD) came out with a strong set of second-quarter numbers that could potentially lead to a re-rate of the stock. Statutory earnings performance was extremely strong, with revenue of US$326m beating expectations by 29% and earnings per share (EPS) of US$1.22, an impressive 138%ahead of expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Simpson Manufacturing after the latest results.

Check out our latest analysis for Simpson Manufacturing

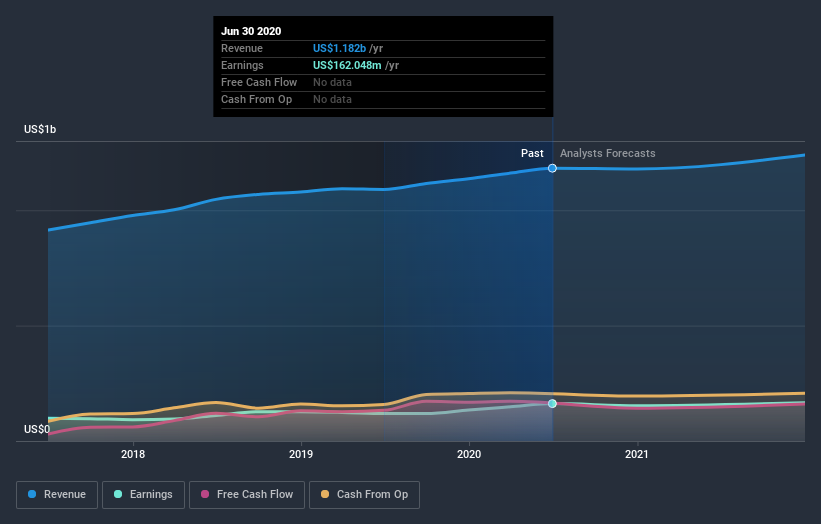

Taking into account the latest results, Simpson Manufacturing's four analysts currently expect revenues in 2020 to be US$1.18b, approximately in line with the last 12 months. Statutory earnings per share are forecast to shrink 4.9% to US$3.48 in the same period. Before this earnings report, the analysts had been forecasting revenues of US$1.05b and earnings per share (EPS) of US$2.47 in 2020. So we can see there's been a pretty clear increase in sentiment following the latest results, with both revenues and earnings per share receiving a decent lift in the latest estimates.

With these upgrades, we're not surprised to see that the analysts have lifted their price target 25% to US$93.75per share. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Simpson Manufacturing analyst has a price target of US$106 per share, while the most pessimistic values it at US$82.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with the forecast 0.3% revenue decline a notable change from historical growth of 9.1% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.2% annually for the foreseeable future. It's pretty clear that Simpson Manufacturing's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Simpson Manufacturing following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Simpson Manufacturing going out to 2021, and you can see them free on our platform here..

Before you take the next step you should know about the 1 warning sign for Simpson Manufacturing that we have uncovered.

When trading Simpson Manufacturing or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:SSD

Simpson Manufacturing

Through its subsidiaries, designs, engineers, manufactures, and sells structural solutions for wood, concrete, and steel connections in North America, Europe, and the Asia Pacific.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor